Markets Today - May 18, 2026

May 18•4 min read

.png)

Daily analysis of crypto markets and the forces shaping them, from the Nexo research desk.

Oil-driven yield repricing keeps crypto in consolidation

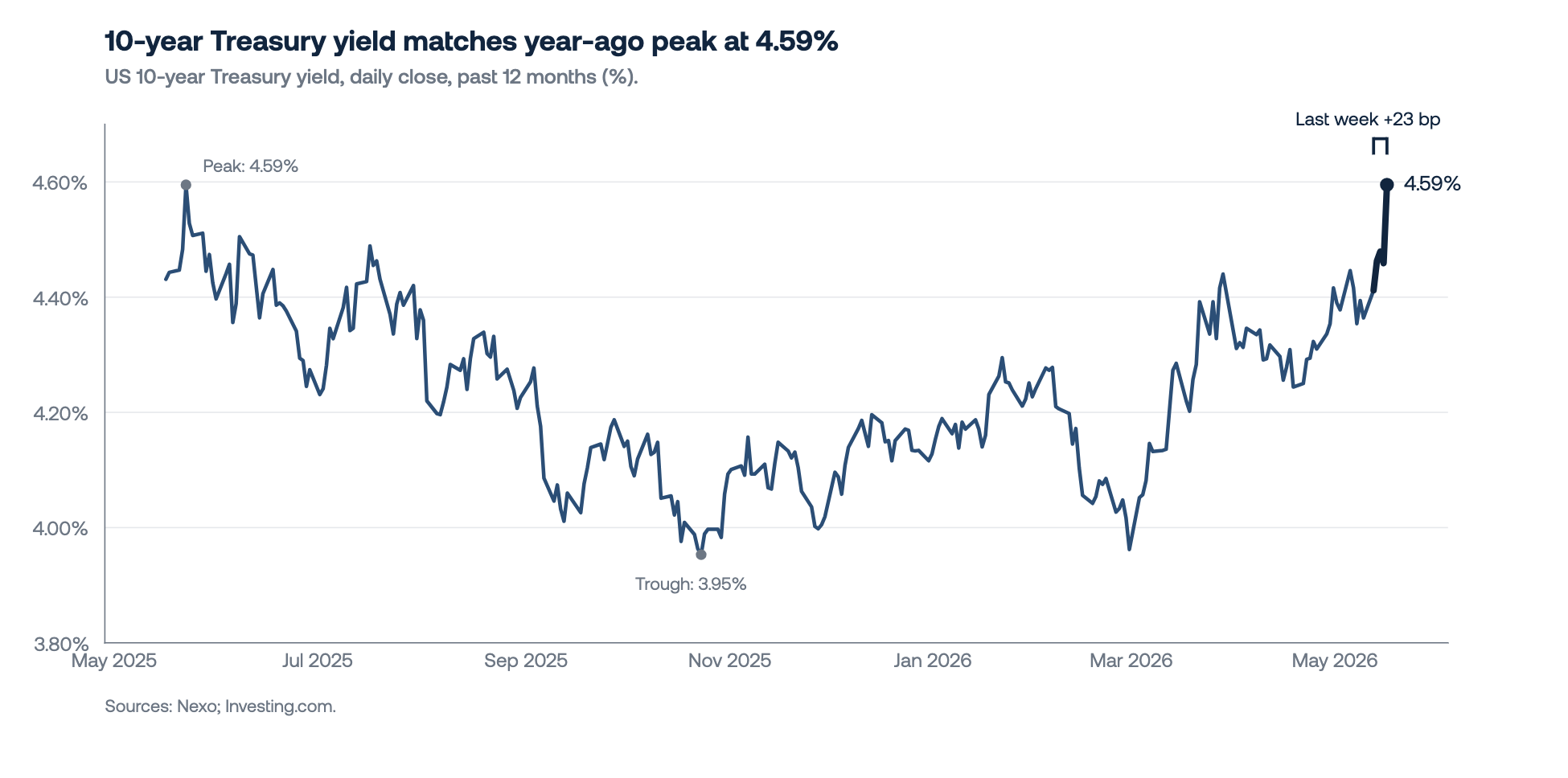

Crypto markets are consolidating as the broader macro backdrop turns more hawkish. Bitcoin traded around $77,000 on Monday morning, down 4.7% on the week and at the lower end of its 24h $76,800–$78,400 range. The U.S. 10-year yield has reached a 15-month high on the back of a multi-week oil rally tied to the effective closure of the Strait of Hormuz, with Brent above $110 a barrel. Rate-hike odds for the remainder of the year have re-priced to roughly even, and risk assets are absorbing the shift. The April FOMC meeting minutes are due Wednesday at 18:00 UTC and will be parsed for how persistently above-target inflation is being weighted against growth risks.

Bitcoin

Bitcoin has rolled over from $82,200 to near $77,000 in the week since the CLARITY Act vote, as the regulatory catalyst gave way to macro tightening as the dominant driver. Reports that Strategy may sell part of its Bitcoin holdings, its first such signal since the 2020 treasury pivot, have added a supply-side overhang.

Derivatives positioning points to orderly de-leveraging, not a flush. Daily liquidations sit near baseline at around $47 million, but longs account for 74% of the total versus roughly 50% over the prior 90 days. Leveraged longs are being unwound, not cascaded. Perpetual futures open interest fell roughly $5 billion from the May peak, per Glassnode, confirming leverage has come out cleanly. Funding rates averaged marginally positive, with about a quarter of hourly prints negative; conviction is fading but has not flipped to outright short-positioning that would set up a contrarian bid.

ETF flows turned net negative last week, with around $1 billion in outflows — the discretionary institutional channel stepped back too, not just leveraged retail. With macro headwinds intact, the path of least resistance is sideways-to-lower toward $73,800. A directional reset higher would require a reclaim of $82,000 alongside a supportive macro impulse.

Ethereum & Altcoins

Ethereum trades at $2,120 following the May 11 rejection at $2,340. Price sits above the $1,816 February cycle low but well below the $3,382 YTD high from January. ETF flows reinforce the softer tone. Ethereum spot ETFs posted five consecutive outflow days through May 15, totaling $255 million for the week. Cumulative net inflows now stand at $11.83 billion against assets of $12.93 billion.

Across the altcoins, the divergence between price and flow is sharp. Solana is the weakest of the majors, off about 2% to $84 in the past 24 hours, yet SOL spot ETFs absorbed $58 million in net inflows over the last five sessions and now hold cumulative inflows of $1.12 billion. The flows are not yet supporting the price. XRP shows the opposite pattern: down 2.2% to $1.38 over the past day but supported by $60.5 million in net ETF inflows over the week, with cumulative inflows at $1.39 billion.

Macro & Institutional

The selloff in global bonds is the dominant story in global financial markets. The U.S. 10-year yield rose more than 20 basis points last week to close at 4.59% on May 15, with the 2s10s curve widening as the long end led the move. The driver was the inflation data flow. CPI for April printed at the highest year-on-year reading in nearly three years, followed by a hotter-than-expected PPI release and import and export price prints above consensus. Pricing for Fed cuts in 2026 has been fully removed from the curve, with a small probability of a hike now showing in fed funds futures.

Crypto weakness reflects a long-end-led yield move that tightens financial conditions without Fed action. A sustained reversal would require a clean disinflation print or Middle East de-escalation that pulls oil and yields lower.

Looking Ahead

The April 28-29 FOMC minutes detail the 8-4 split — the most divided vote since October 1992 — and the reasoning behind dissents on the easing bias. Flash PMIs on Thursday give the first read on May activity. University of Michigan inflation expectations at week's end test whether April CPI and PPI have lifted the consumer's longer-run view.

Author: Dessislava Ianeva, Analyst at Nexo’s Dispatch

This material is produced by Nexo for informational purposes only and does not constitute financial, investment, legal, or tax advice, or a recommendation to transact in any digital asset. Views are the author's as of the date of publication and may change without notice. Information is from sources believed reliable, but Nexo makes no warranty as to its accuracy and accepts no liability for any loss arising from reliance on this material.