Markets Today - May 13, 2026

May 13•4 min read

Daily analysis of crypto markets and the forces shaping them, from the Nexo research desk.

Bitcoin keeps its gains despite hot U.S. inflation

Bitcoin is holding above $80,000 and the total crypto market cap is edging back toward $2.7 trillion, despite U.S. inflation accelerating in April. Yesterday's CPI printed at 3.8% y/y, with energy contributing 40% of the increase and pushing December rate-hike odds to nearly 30%, up from 15% a week ago. The cross-asset response is mixed: U.S. equity futures are lower alongside Asian and European indices, while Brent crude holds steady near $106 a barrel. Gold has stabilized around $4,700 but is down 3% over the past month and nearly 11% below its February record. The main question for markets now is how central banks respond to firmer inflation.

Bitcoin

Bitcoin is trading near $81,000, down 0.3% on the day, with the 7-day range compressed to roughly $79,500–$82,500. Per Glassnode, BTC perpetual open interest has fallen 7% from a week ago to $36.8 billion, consistent with deleveraging on the move below $80,000. Funding sits at 3.4% annualized after averaging slightly negative over the past 30 days, indicating balanced positioning rather than crowded long.

Options markets line up the same way. Implied volatility has compressed, with the term structure in normal contango: one-week ATM IV at 35.4%, one-month at 36.2%, three-month at 38.7%, and six-month at 41.8%. The volatility setup reflects pricing for a contained near-term move. A clean break above $82,500 or below $79,500 would likely reset both volatility and positioning. The catalyst is more likely to come from rates pricing than from crypto-native flows.

Ethereum & Altcoins

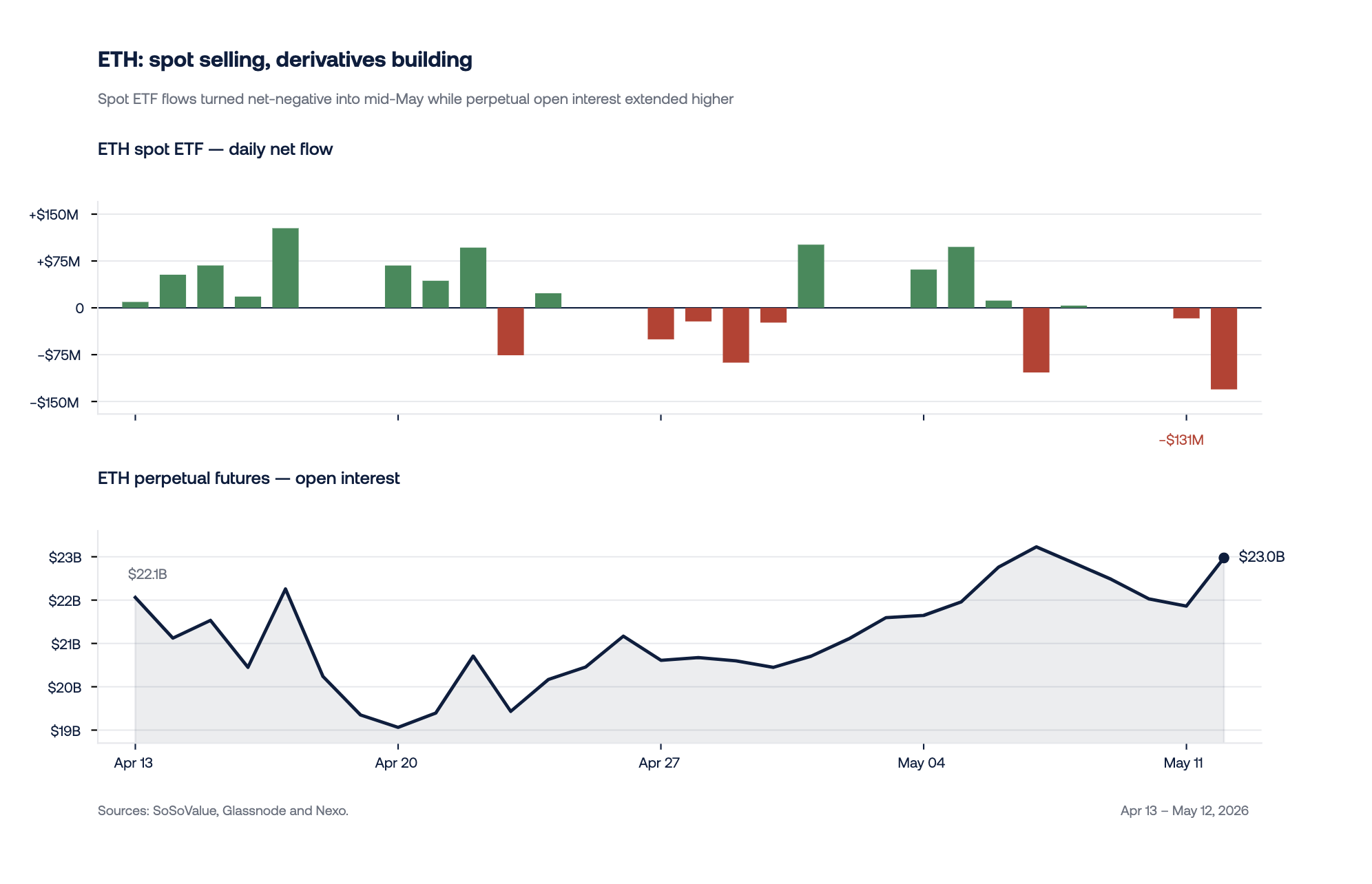

Ethereum is trading near $2,300, flat on the day and down 3% on the week. Spot has been a net seller all month and ETF outflows have accelerated this week. May 12 alone saw $131 million pulled, with the last two sessions netting roughly $148 million. Derivatives, however, are pulling the other way: perpetual futures open interest is building and funding has flipped positive, with leveraged traders adding bullish exposure even as cash markets distribute.

The picture in other large altcoins is cleaner. Solana and XRP are both higher on the week, with SOL futures open interest up 42% over 30 days and XRP up 22%. Funding on both is persistently positive, and spot ETFs are seeing consistent inflows in May. The institutional altcoin bid is selective: present in SOL and XRP, absent in ETH. In both cases real-money flows and leveraged positioning are pulling the same way, unlike ETH, where leveraged length is building into a cash market that's selling.

Macro & Institutional

December Brent futures are back above $90 a barrel after U.S. President Trump labeled Tehran's latest peace overture "garbage", the clearest signal yet that the Hormuz premium is sticking. A sustained move higher in oil would harden the pass-through CPI breadth confirmed yesterday. Two-year Treasury yields at 4% and rising odds of a December Fed rate hike tilt the implied policy path hawkish, narrowing the easing markets had priced through Q1.

China is potentially the offsetting force in the global risk picture. April exports rose 14% year-on-year against ~8% consensus, with technology leading despite chip restrictions. The CSI 300, China's blue-chip equity benchmark, sits above its prior Trump 1.0 peak; 10-year CGB yields trade below 2%. Resilient growth and accommodative monetary conditions stand in sharp contrast to US repricing. The Trump-Xi summit is the binary swing factor: with rare-earths leverage and AI deployment capacity, Beijing arrives in a materially stronger position than in 2017. A constructive summit keeps risk supported; escalation exposes it to one-sided Fed pressure.

On the institutional side, the Senate confirmed Kevin Warsh to the Federal Reserve Board and chair confirmation is widely expected. The Powell-to-Warsh transition completes against an inflation regime in which the room for a dovish pivot has narrowed materially.

Looking Ahead

Fed's Collins and Kashkari deliver the first Fed remarks since April CPI, followed later in the session by ECB's Lagarde — early signal on how central bank reaction functions are recalibrating to the print. The US 30-Year Treasury auction prints between the two Fed appearances, testing long-end demand after yesterday's soft 10-Year. Focus at the end of the week shifts to US Retail Sales, Import Prices, and Initial Jobless Claims, with the Atlanta Fed's next Q2 GDPNow update to follow. If Retail Sales and Import Prices reinforce CPI's broader inflation signal, the implied policy path tilts more hawkish; softer activity against firm prices reopens the stagflation frame.

Author: Dessislava Ianeva, Analyst at Nexo’s Dispatch

This material is produced by Nexo for informational purposes only and does not constitute financial, investment, legal, or tax advice, or a recommendation to transact in any digital asset. Views are the author's as of the date of publication and may change without notice. Information is from sources believed reliable, but Nexo makes no warranty as to its accuracy and accepts no liability for any loss arising from reliance on this material.