Markets Today - June 26, 2026

Jun 26•4 min read

.png)

Daily analysis of crypto markets and the forces shaping them, from the Nexo research desk.

Bitcoin steadies near $60,000 as a three-year-high inflation print resets the rate path

The crypto market is closing a challenging week. Bitcoin has steadied near $60,000 after yesterday's pullback to $58,479, triggered by a three-year-high U.S. PCE inflation reading that pushed Fed rate cuts further out of reach. Ethereum and the broader altcoin complex are also lower, leaving the total crypto market cap around $2.1 trillion. Equities offer no cover: the S&P 500 is down 1.73% on the week and the Nasdaq more, as the AI trade wobbles on stretched valuations and concerns that rising component costs will squeeze hardware margins. Brent crude sits near $76 and the dollar holds close to a seven-month high. Today's calendar is light, but the week ahead turns on the June payrolls report, the most consequential print for the rate outlook and crypto's near-term direction.

Bitcoin

Bitcoin trades near $60,000, down 2.4% on the day after Thursday's correction to $58,479 on a hotter-than-expected PCE print and softer consumer spending. The move was macro driven, not crypto-specific. The breakdown from this week's $65,505 high leaves $62,000 as first resistance and $58,500 as support.

Liquidity is the bigger story. Glassnode data show order-book depth has thinned sharply through the selloff, and the damage is mostly on the bid side: market makers pulled buy orders rather than catch a falling tape, while offers held. The thinning is on the demand side of the book, not from added selling, and it leaves the path forward asymmetric — thin bids mean each sell can more easily move price further down. Until bids rebuild, the path of least resistance stays lower unless Bitcoin reclaims $62,000.

Ethereum & Altcoins

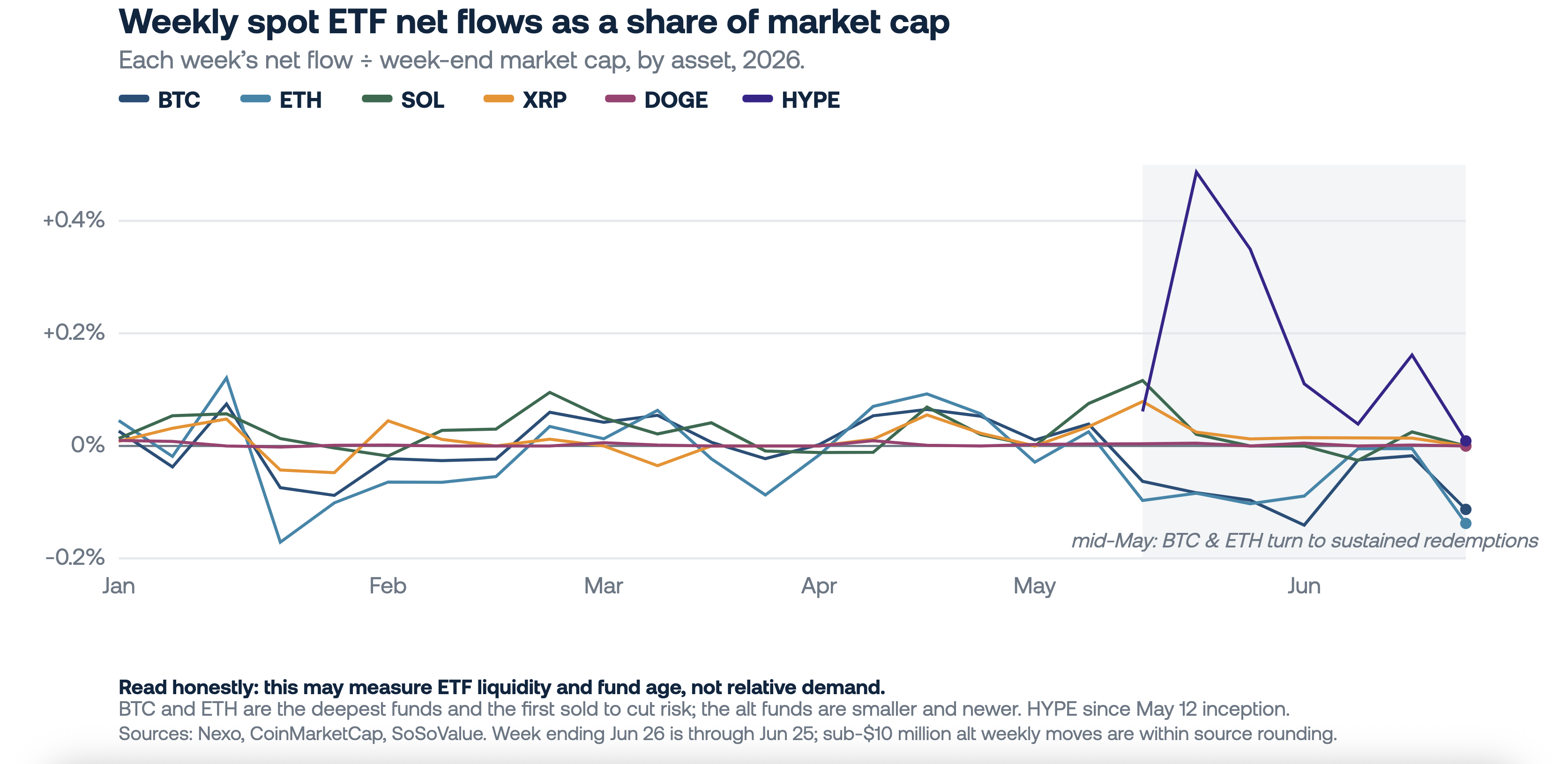

Ethereum trades around $1,560, down 5.2% over 24 hours and underperforming Bitcoin's 2.4% decline. The complex is stabilizing rather than recovering. Both bounced close to 3% off the overnight low after yesterday's PCE-driven retraction, but most majors remain red, with XRP down 4.0% and Dogecoin 3.4%. Solana and Hyperliquid were the exceptions, each up around 1.3%. The macro setting has turned hostile, and Bitcoin and Ethereum have acted as the liquid de-risking vehicles. Their spot ETFs flipped to net redeemers in May and June, shedding roughly 0.3% and 0.2% of market cap, while the smaller alt funds held positive flows. Rather than relative demand, this divergence likely reflects what institutions sell to cut risk, and is consistent with Bitcoin dominance holding near 58.4%.

Macro & Institutional

Technology stocks set the tone again, and crypto followed them down. The S&P 500 fell 1.73% on the week and the Nasdaq more, as investors soured on stretched AI valuations. A report that OpenAI may delay its IPO to 2027 and Apple's price hikes on higher memory costs were the triggers. Korean chip giants SK Hynix and Samsung led the selling even as both prepare record AI spending. The message is a more selective market that wants earnings and reasonable prices, not just the AI story.

The macro picture is an uncomfortable squeeze. Core inflation ticked up to 3.4%, which keeps the Fed sidelined and even revives talk of a hike. Treasury yields did fall, but for the wrong reason — softer consumer spending and a hint of demand weakness, not cooling prices. So the market is caught between inflation too high to let the Fed ease and growth soft enough to worry about. That is not a clean signal in either direction, and risk assets cannot find footing in it.

Looking Ahead

Today's data calendar is quiet. The final University of Michigan survey for June is the only U.S. release of note, with one-year inflation expectations seen easing to 4.6% from 4.8%. The week ahead is shortened and jobs-dominated. U.S. markets close Friday, July 3 for the observed Independence Day holiday. That pulls the June employment report forward to Thursday, July 2. Consensus looks for nonfarm payrolls of 172,000, unemployment at 4.3%, and earnings up 0.3% on the month. The print is the week's main risk event because it shapes the Fed's path. A soft number revives easing expectations and supports risk assets. Firm payrolls reinforce the hawkish read that pushed Bitcoin below $58,000 this week. The major crypto-specific catalyst next week sits in Washington. Senator Lummis has flagged final CLARITY Act text around July 4. It would be the first read on whether the market-structure bill can clear the Senate before the August recess.

Author: Dessislava Ianeva, Analyst at Nexo’s Dispatch

This material is produced by Nexo for informational purposes only and does not constitute financial, investment, legal, or tax advice, or a recommendation to transact in any digital asset. Views are the author's as of the date of publication and may change without notice. Information is from sources believed reliable, but Nexo makes no warranty as to its accuracy and accepts no liability for any loss arising from reliance on this material.