Markets Today - June 22, 2026

Jun 22•4 min read

-3.png)

Daily analysis of crypto markets and the forces shaping them, from the Nexo research desk.

Bitcoin holds ground as risk sentiment cautiously recovers

Bitcoin is holding the mid-$60,000s in early Monday trading as weekend diplomacy between Washington and Tehran produced better-than-feared outcomes. U.S. Vice President Vance met Iranian Foreign Minister Araghchi in Switzerland over the weekend, with Iran reporting major progress toward a formal agreement. Oil is easing, Asian equities closed largely positive led by tech and semiconductors. The week's primary variables are Fedspeak, Thursday's PCE print, and any further developments out of the Strait of Hormuz, where shipping levels remain far below pre-conflict norms despite the ceasefire.

Bitcoin

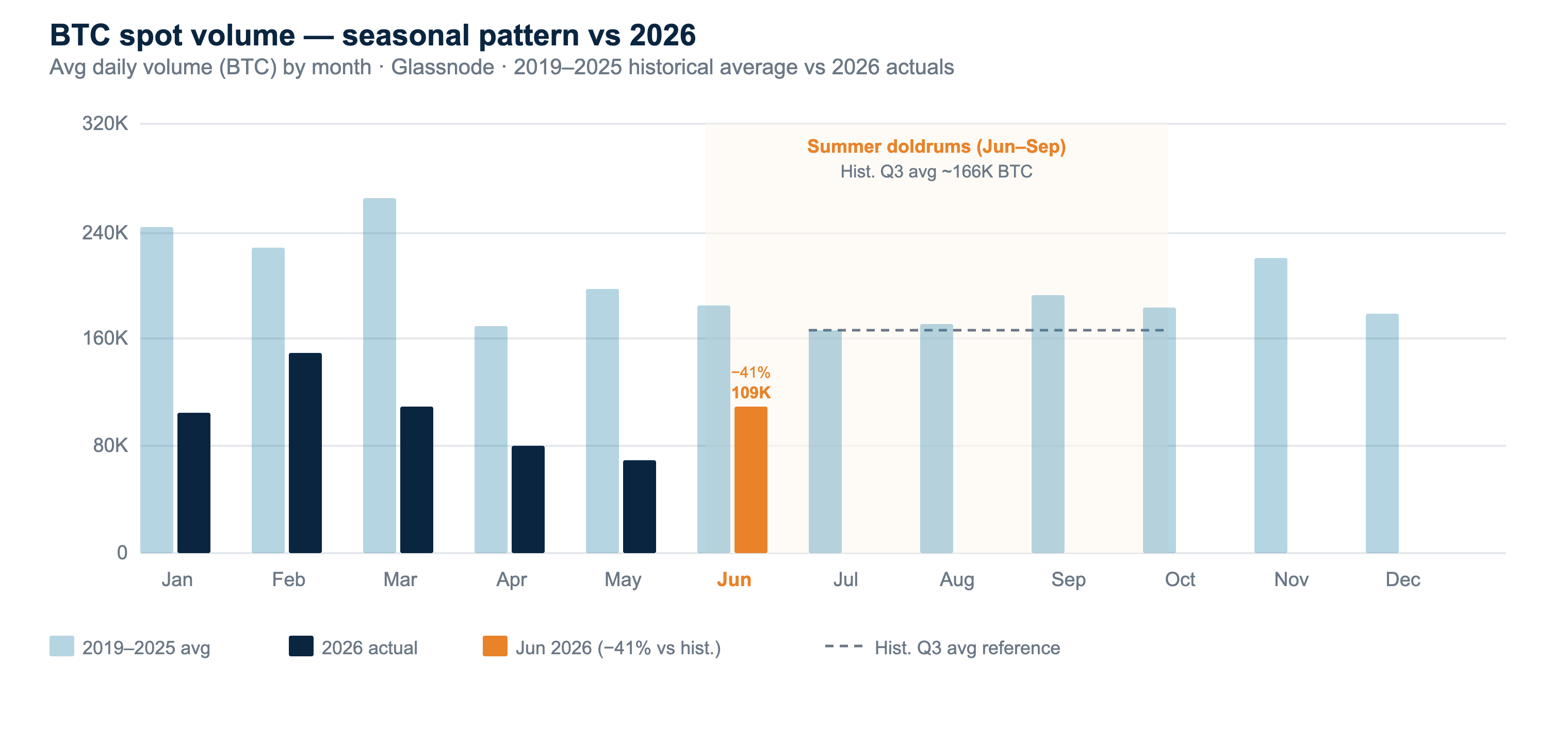

Bitcoin is trading above $64,000, holding a $62,000–$67,000 range for the past seven days, with the 50-day moving average falling above spot as resistance.

The current consolidation is also a liquidity story. June spot volume so far averaged ~109,000 BTC per day — 41% below the historical June average — and fell sharply within the month, from ~105,000 BTC on June 17 to ~52,000 BTC on June 21. As per Glassnode data, Net CVD shows selling is persistent but moderating. However, buyers are not stepping in. U.S. spot ETF net assets have fallen from $104 billion on May 15 to $78 billion on June 18. Outflows have slowed from -$733 million on May 27 to about ~-$82 million over the past three sessions.

In a thin book, this week's catalysts could hit harder. Thursday's PCE and any Hormuz development could generate a sharper move than the range implies. A hawkish PCE surprise reinforces the post-FOMC dollar bid — the most consistent headwind for Bitcoin since the June meeting.

Ethereum & Altcoins

Ethereum is trading slightly above ~$1,700, down on the day, at the lower end of its $1,700–$1,786 weekly range. ETF flows were negative into the weekend (-$29.4 million on June 17, -$12.8 million on June 18). Net assets stand at $9.3 billion. SOL is at ~$74, broadly flat. XRP ($1.13) and DOGE ($0.083) are soft with no specific catalyst.

ETH and SOL are moving in lockstep with Bitcoin — 7-day correlation of ~0.85 — offering no independent signal. XRP is slightly lower at 0.77. HYPE is the outlier. Its 7-day BTC correlation is just 0.24, driven by asset-specific flow rather than broad market beta. Glassnode CVD shows HYPE net buying picked up last week, the first positive weekly flow in three weeks , though Monday's session saw a modest reversal. The improvement is real but not yet sustained.

Macro & Institutional

The week opens with geopolitics as the dominant variable. The Vance–Araghchi talks in Switzerland produced cautiously positive signals: Iran reported major progress toward a formal agreement, including oil and petrochemical export waivers and a reconstruction initiative, as part of the June 17 memorandum of understanding. Brent crude is down ~1.6%, back toward the $78.50 200-day moving average. The Strait of Hormuz remains structurally unresolved, shipping levels are still far below pre-conflict norms and any reversal in the talks would reprice oil and risk assets simultaneously.

The dollar is moderately bid near May 2025 levels and U.S. Treasury yields are higher across the curve following Friday's Juneteenth closure. The post-FOMC setup remains the macro frame. Fed Chair Warsh held rates at 3.50–3.75% last week but penciled in further 2026 hikes and trimmed forward guidance, with markets now pricing more than 40 basis points of additional tightening by December. A stronger dollar and elevated yields are the most consistent headwinds for risk assets this week.

Looking Ahead

The data calendar is active. Canadian May CPI is the first test — markets are pricing 21 basis points of BoC tightening by year-end, and a miss on the trimmed and median measures would likely prompt a dovish repricing and weigh on CAD. Lagarde speaks today for the first time since the ECB's recent policy recalibration; Waller's remarks are also worth watching for any pushback against the 43 basis points of December tightening priced in. Flash PMIs for the eurozone and U.S. follow tomorrow. The week's centerpiece is Thursday: U.S. core PCE (consensus 0.3% month-on-month), Q1 GDP final, durable goods, and personal spending in one session — the most direct read on whether the post-FOMC hawkish repricing is justified.

Author: Dessislava Ianeva, Analyst at Nexo’s Dispatch

This material is produced by Nexo for informational purposes only and does not constitute financial, investment, legal, or tax advice, or a recommendation to transact in any digital asset. Views are the author's as of the date of publication and may change without notice. Information is from sources believed reliable, but Nexo makes no warranty as to its accuracy and accepts no liability for any loss arising from reliance on this material.