Markets Today - July 6, 2026

Jul 06•4 min read

-1.png)

Daily analysis of crypto markets and the forces shaping them, from the Nexo research desk.

Bitcoin holds gains as Fed tightening fears ease

Bitcoin is holding most of last week's gains, with Fed tightening fears easing after Thursday's weaker-than-expected jobs report. The total crypto market cap is steady near $2.17 trillion, up 0.4% over the past 24 hours. U.S. equities opened higher on Monday, while oil eased after OPEC+ agreed to add a further 188,000 barrels per day from August. Gold slipped as the dollar firmed off two-week lows.The week's main event is Wednesday's June FOMC minutes, the first under Kevin Warsh. The tone is expected to be hawkish, but with forward guidance stripped from the statement, markets will scrutinize the minutes for any read on the path ahead.

Bitcoin

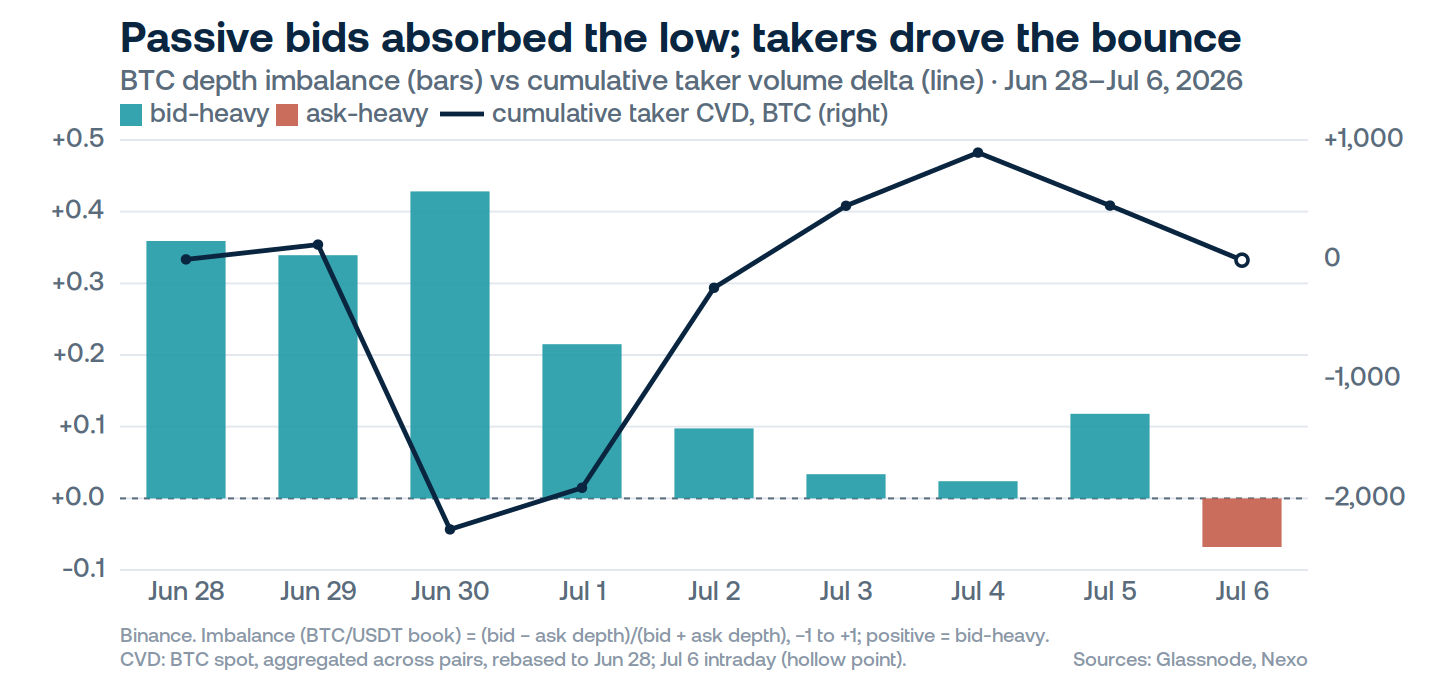

Bitcoin is hovering near $63,000, softening during Monday's session after a six-day rally that lifted prices from late-June lows around $58,500. Despite last week's recovery, the asset remains pinned beneath its 50-day and 200-day moving averages, marking the move as a relief bounce within a broader downtrend.

Order-book data adds colour. Liquidity improved during the climb: bid-ask spreads tightened and slippage fell, so the market can now digest larger orders with less price impact. The book's skew also evened out. Glassnode data shows Bitcoin's order book was heavily tilted to the bid at the June 30 trough, where resting bids absorbed a peak in taker selling that marked the bottom, but has since eased back to balance. A balanced book is a constructive signal: it points to two-way flow rather than one-sided pressure, a healthier and more normally functioning market with active market makers quoting both sides. Taken with the tighter spreads, that suggests liquidity providers are re-engaging rather than stepping back.

While spot Bitcoin ETFs faced an eighth week of outflows, with June seeing roughly $4.5 billion in exits, last week recorded the first net inflow since mid-month, signaling sell-side pressure may be tapering. Following last week's jobs data, markets are now centering on Wednesday's FOMC minutes for the next directional signal.

Ethereum & Altcoins

Ethereum is trading around $1,770, up roughly 12% over the past week but stalling just below $1,800 after tagging that level and easing back. The move has been broad. Solana has added about 11% over the same stretch, XRP around 9%, and Dogecoin close to 6%, while Hyperliquid's HYPE has led at roughly 13%. On the day, most majors are little changed as the market consolidates last week's advance rather than extending it. HYPE is the exception, up about 3.6% over 24 hours. Derivatives positioning looks constructive but not stretched. As per Glassnode data Ethereum's perpetual futures open interest in native units has rebuilt but remains around 11% below its early-June record, and funding rates have held modestly positive, consistent with longs rebuilding without excess leverage.

Macro & Institutional

Movements across asset classes are being driven primarily by shifting rate expectations. Last week's soft payrolls trimmed bets on near-term Fed tightening but did not reverse them. Markets still lean toward a hike this year, not a cut. That bias is setting the cross-asset tone. The dollar has firmed off two-week lows, pulling gold back from its recent rebound. Oil has drifted lower after OPEC+ agreed on July 5 to add another 188,000 barrels per day from August. That extends the June and July increases into a market already well supplied, with Strait of Hormuz flows recovering and Chinese demand soft. Cheaper crude is the one disinflationary crosscurrent to the tightening story, though it has shifted it little. Equity futures held higher after the long weekend, led by the Nasdaq 100. The through-line is rate uncertainty. A firmer dollar and higher-for-longer expectations raise the opportunity cost of non-yielding assets. That weighs on gold and leaves crypto trading off the same dollar-and-yields signal.

Looking Ahead

Light on data, the week hands the Fed the wheel. Wednesday's June FOMC minutes are the main driver, the first under Kevin Warsh, and the expected read is hawkish. Monday's ISM Services release is the one print worth watching, for whether prices paid ease from a multi-year high, with Fed and ECB speakers filling the session. For crypto, absent idiosyncratic digital-asset catalysts, the dollar and yields hold control. A hawkish minutes read is the main risk to appetite.

Author: Dessislava Ianeva, Analyst at Nexo’s Dispatch

This material is produced by Nexo for informational purposes only and does not constitute financial, investment, legal, or tax advice, or a recommendation to transact in any digital asset. Views are the author's as of the date of publication and may change without notice. Information is from sources believed reliable, but Nexo makes no warranty as to its accuracy and accepts no liability for any loss arising from reliance on this material.