Markets Today - July 3, 2026

Jul 03•4 min read

.png)

Daily analysis of crypto markets and the forces shaping them, from the Nexo research desk.

Bitcoin steadies near $62,000 as soft payrolls ease the Fed's hand and sentiment shifts

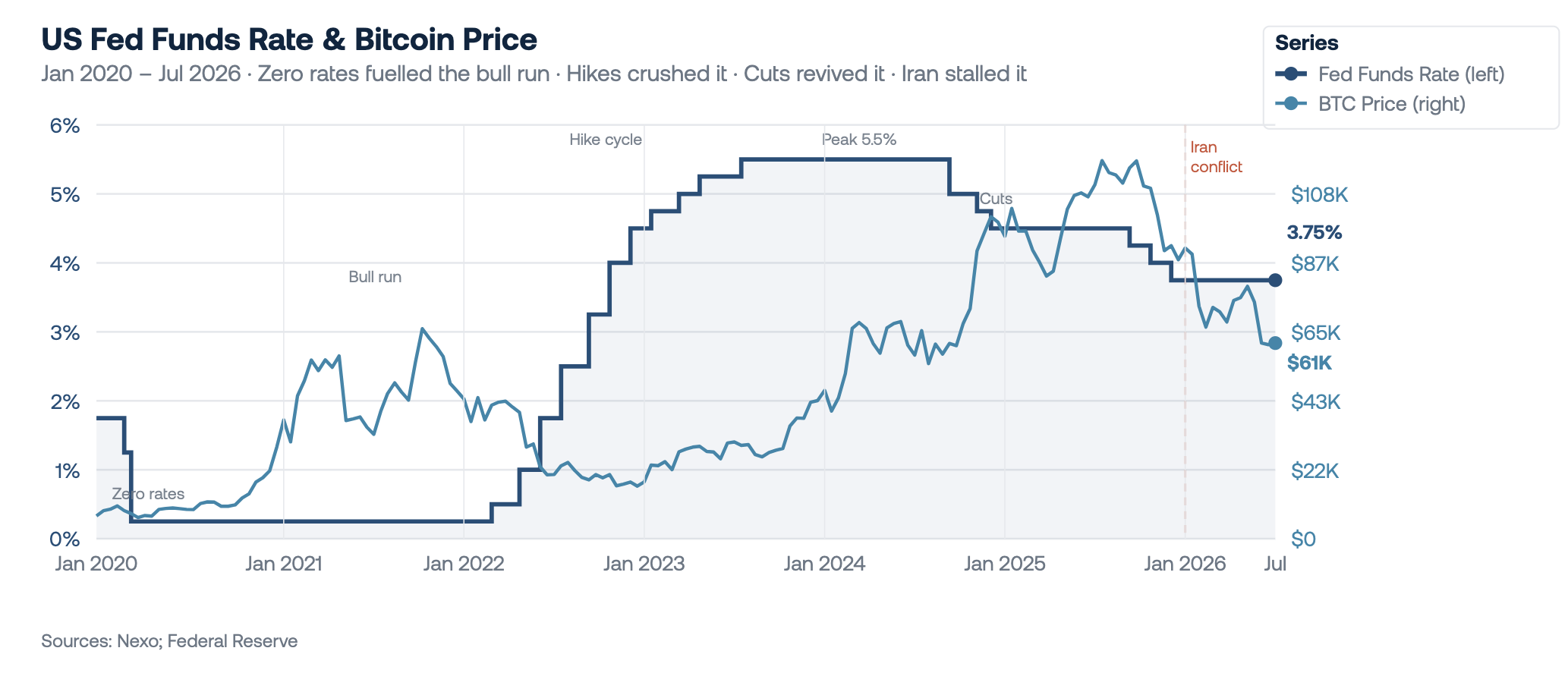

A weaker-than-expected June jobs report has done in one session what weeks of diplomatic progress could not — meaningfully repriced the Fed's rate trajectory and given risk assets room to breathe. Bitcoin is trading around $61,600, up on the week for the first time since mid-June, as U.S. markets prepare to close for the Independence Day holiday. Equity futures are pointing higher, with the Nasdaq up 0.9% and the S&P 500 up 0.4%, as semiconductor stocks attempt a recovery following this week's pullback. Brent crude is near $72, the USD is on track for its first weekly loss in two weeks, and gold is heading for its first weekly gain in five. The total crypto market cap is recovering as the combination of softer rate expectations and a squeeze on short positions has pushed the broader complex meaningfully higher.

Bitcoin

Bitcoin is trading around $61,600, up approximately 3% on the week and recovering from the 21-month low of under $58,000 touched earlier this week. June nonfarm payrolls came in at just 57,000 — well below the 110,000 expected. snapping a three-month streak of upside surprises and compounded by downward revisions to April and May that removed a combined 74,000 jobs from prior estimates. The probability of a July rate hike fell from 34% on Tuesday to just 18% by Thursday's close. Warsh's Sintra acknowledgement that inflation risks had come down provided the framing; the jobs data provided the confirmation.

Spot Bitcoin ETFs recorded net inflows of $221.7 million on Thursday — the largest single-day figure in two months, ending a 10-day outflow streak. Year-to-date net outflows remain around $5.4 billion, and one session does not make a trend. But the direction matters: the first net inflow day in nearly two weeks, arriving alongside a soft jobs print and a recovering price, is the combination the market has been waiting for. For the recovery to develop into something durable, these inflows need to become consistent — historically, sustained ETF inflows have been a hallmark of Bitcoin's stronger periods.

Ethereum & Altcoins

Ethereum jumped approximately 5% to around $1,708, up nearly 10% on the week and the standout performer among large caps. Solana extended its run to $80, posting an 18.6% weekly gain — the strongest among the majors. XRP rose to $1.09, Cardano surged, and Hyperliquid's HYPE gained on the day. The altcoin complex is broadly recovering, though thin holiday-weekend liquidity amplifies moves in either direction and the pace of recovery should be read with that context in mind.

Macro & Institutional

The June payrolls print of 57,000 is the week's defining data release — the weakest reading since early 2025. The labour market picture is one of stabilisation rather than acceleration, not weak enough to signal recession but soft enough to remove the urgency of near-term Fed tightening. The rate outlook has shifted from one to two hikes toward zero to one in 2026. Wednesday's Fed meeting minutes are the next window into how Warsh's committee was thinking about inflation and the Iran deal's macro impact — and with forward guidance abandoned, these minutes carry more weight than they have in years.

Brent at $72 is essentially unchanged for the week, with the market structure having flipped from backwardation to contango — signalling near-term oversupply as Gulf production recovers. Bloomberg reported that some European leaders have begun to accept that Hormuz shipping fees may be inevitable — a development that, if formalised, would introduce a structural cost into the supply chain.

The week's semiconductor pullback — with key AI memory ETFs falling 12–25% from June highs, alongside Bitcoin's recovery is the first indication in months that investors may be beginning to rebalance risk back toward digital assets. It is too early to call this a sustained rotation, but a stabilising AI trade removes the most acute source of capital competition that defined H1. Samsung surging 6.8% on reports of an Anthropic chip partnership is a reminder that AI infrastructure spending has not stopped — the debate is over its pace, not its direction.

Looking Ahead

U.S. markets are closed today. Monday opens the week with the S&P Global Services PMI and ISM Non-Manufacturing PMI for June — an early read on whether the labour market softness is feeding through to broader activity. Wednesday is the week's defining day, with the Fed meeting minutes releasing alongside a 10-year Treasury note auction — the minutes being the first detailed window into how Warsh's committee weighed inflation, the Iran deal, and the rate path, and with forward guidance now abandoned, they carry more weight than they have in years. Thursday brings initial jobless claims, which will be closely watched for confirmation of whether June's soft payrolls print was a one-off or the start of a broader cooling trend. For Bitcoin, the question entering Q3 is whether Thursday's ETF inflow and the short squeeze mark the start of a more sustained recovery, or whether the market needs further macro confirmation before institutional demand returns in size.

Author: Iliya Kalchev, Analyst at Nexo’s Dispatch

This material is produced by Nexo for informational purposes only and does not constitute financial, investment, legal, or tax advice, or a recommendation to transact in any digital asset. Views are the author's as of the date of publication and may change without notice. Information is from sources believed reliable, but Nexo makes no warranty as to its accuracy and accepts no liability for any loss arising from reliance on this material.