Markets Today - July 16, 2026

Jul 16•5 min read

.png)

Daily analysis of crypto markets and the forces shaping them, from the Nexo research desk.

Bitcoin steadies near $64,000 as cooling inflation offsets geopolitical risk

The crypto market is consolidating on Thursday after a constructive week, with Bitcoin steadying near $64,160 — easing slightly on the day after touching a monthly high of $65,500 on Wednesday, but still up around 1.6% on the week after recovering from its lows for the year. The macro backdrop has turned meaningfully more supportive: following Tuesday's soft CPI, Wednesday's producer price index (PPI) also came in below expectations, falling 0.3%, and the back-to-back prints have led markets to all but write off a July Fed hike, now priced at just 10%. Across other assets, the tone was steady: U.S. equity futures edged higher as record results from chipmaking giant TSMC reaffirmed robust AI demand, European shares were flat, the dollar languished near a one-month low, and gold eased to around $4,030 as a persistent geopolitical premium — renewed U.S.-Iran tensions holding oil near one-month highs, kept a floor under inflation concerns. The total crypto market cap is holding steady as the sector digests these competing forces.

Bitcoin

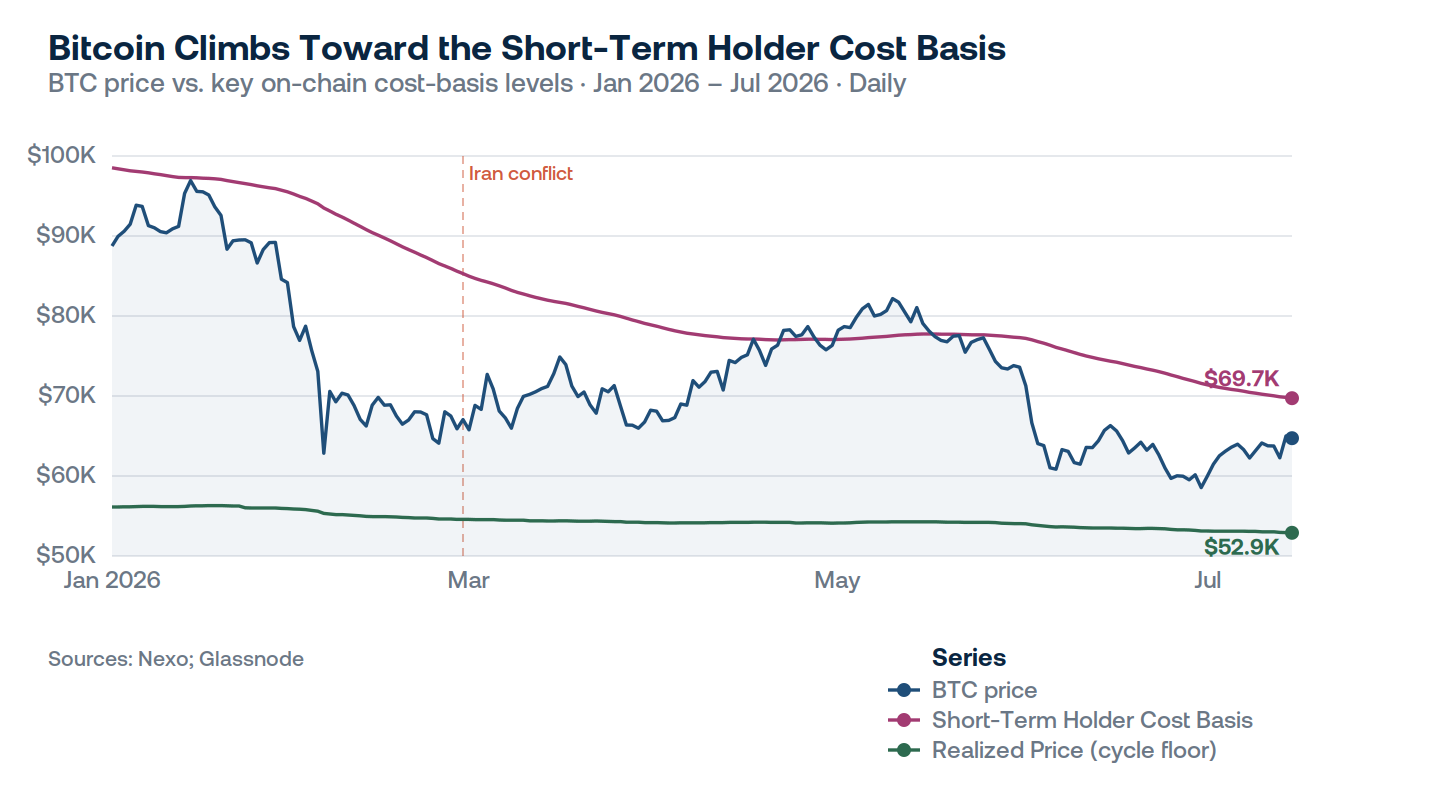

Bitcoin is trading around $64,160, slipping modestly after Wednesday's monthly high of $65,500 invited some profit-taking. The shallow pullback matters less than the behavior that preceded it: Bitcoin reacted to this week's soft inflation prints more forcefully than any major equity index, its sharpest response to good news in weeks. That eagerness to rally on a single data point is the tell of a market where sellers are largely spent and buyers are waiting for a reason — a constructive read even as spot follow-through remains the missing piece.

What is more telling is the shift in what drives the asset. Bitcoin's correlation with equities has been easing while its inverse link to the dollar deepens, so that it increasingly firms on dollar weakness and easing liquidity rather than pure risk sentiment. With the dollar pinned near a one-month low around 100.56 after two soft prints stripped away its rate support, that channel is now the more likely driver of the next move — and it points higher, provided the disinflation narrative holds.

The path from here is well mapped. Bitcoin's first real test sits at the cost basis of recent buyers near $69,000, a break-even level where the holders most inclined to sell are precisely those about to be made whole; a convincing reclaim opens room to run, while a rejection keeps the range intact. Derivatives traders have steadily unwound their downside bets, but until that repositioning is matched by genuine spot demand, the recovery remains promising rather than confirmed.

Ethereum & Altcoins

Ether outperformed on the week, edging higher to around $1,885 even as the broader market softened, while XRP eased to just under its recent range. Solana and Cardano both drifted lower, and BNB was marginally firmer. The moves reflect a market taking profit after recent strength rather than any fresh directional catalyst — a lack of liquidity in both directions has left tokens giving back some of their earlier gains.

The derivatives picture adds nuance. Ether's mild underperformance appears driven by bullish positions unwinding rather than aggressive new short selling, with open interest easing back from a five-week high — a healthier form of pullback than one led by fresh shorts. XRP saw open interest climb to a ten-day high even as its price slipped, a combination that would typically suggest growing bearish exposure, though its positive funding rates complicate that read. The broader takeaway is a market in a holding pattern, with leverage being trimmed rather than added as participants await a clearer signal.

Macro & Institutional

The week's defining story has been the decisive shift in the U.S. rate outlook. Wednesday's PPI unexpectedly fell 0.3%, following Tuesday's soft CPI, and the back-to-back readings — alongside a visibly cooling labor market, have effectively dismantled the narrative of an energy-driven inflation rebound. Markets now price the odds of a July hike at just 12%, a striking recalibration from only a week ago. For crypto, the transmission is direct: with higher rates the primary force behind the sector's recent weakness, the fading of that threat removes a significant overhang.

Equity markets steadied against that backdrop, with U.S. index futures modestly higher as record quarterly results from chipmaking giant TSMC — net profit up 77% to a record ~$22 billion, reaffirmed that AI-infrastructure demand remains exceptionally robust. The read was not uniformly positive: TSMC's shares slipped around 4% pre-market as a sharply raised capital-spending budget revived the perennial debate over whether the semiconductor cycle is secular or cyclical, dragging Nvidia and other chip names lower and capping broader risk appetite. Renewed U.S.-Iran hostilities have held Brent near one-month highs around $84.50, and the central question is whether policymakers read the oil move as a temporary supply shock or as something liable to spill into broader prices. The traditional-asset response captured the macro tension neatly: the same disinflation that has supported Bitcoin drove the dollar to a one-month low near 100.56, while gold slipped to around $4,030 as investors looked past the soft inflation data toward the inflationary risk embedded in higher oil.

Looking Ahead

With the inflation picture now clarified, attention turns to the real-economy data and earnings that will test the soft-landing narrative. Today brings U.S. June retail sales — the clearest read on consumer spending — alongside weekly jobless claims, a timely gauge of the cooling labor market, plus UK GDP and the Philadelphia Fed manufacturing index. Friday rounds out the week with Eurozone CPI. For Bitcoin, the setup is the most constructive in weeks — a fading rate threat, a weakening dollar, and spent sellers, but confirmation hinges on spot demand carrying the price through the overhead resistance near $69,000. Until that follow-through arrives, the recovery remains promising rather than proven, with the Middle East the most likely source of any renewed volatility.

Author: Iliya Kalchev, Analyst at Nexo’s Dispatch

This material is produced by Nexo for informational purposes only and does not constitute financial, investment, legal, or tax advice, or a recommendation to transact in any digital asset. Views are the author's as of the date of publication and may change without notice. Information is from sources believed reliable, but Nexo makes no warranty as to its accuracy and accepts no liability for any loss arising from reliance on this material.