Markets Today - July 1, 2026

Jul 01•5 min read

.png)

Daily analysis of crypto markets and the forces shaping them, from the Nexo research desk.

Bitcoin steadies above $59,000 as Warsh takes the Sintra stage and payrolls loom

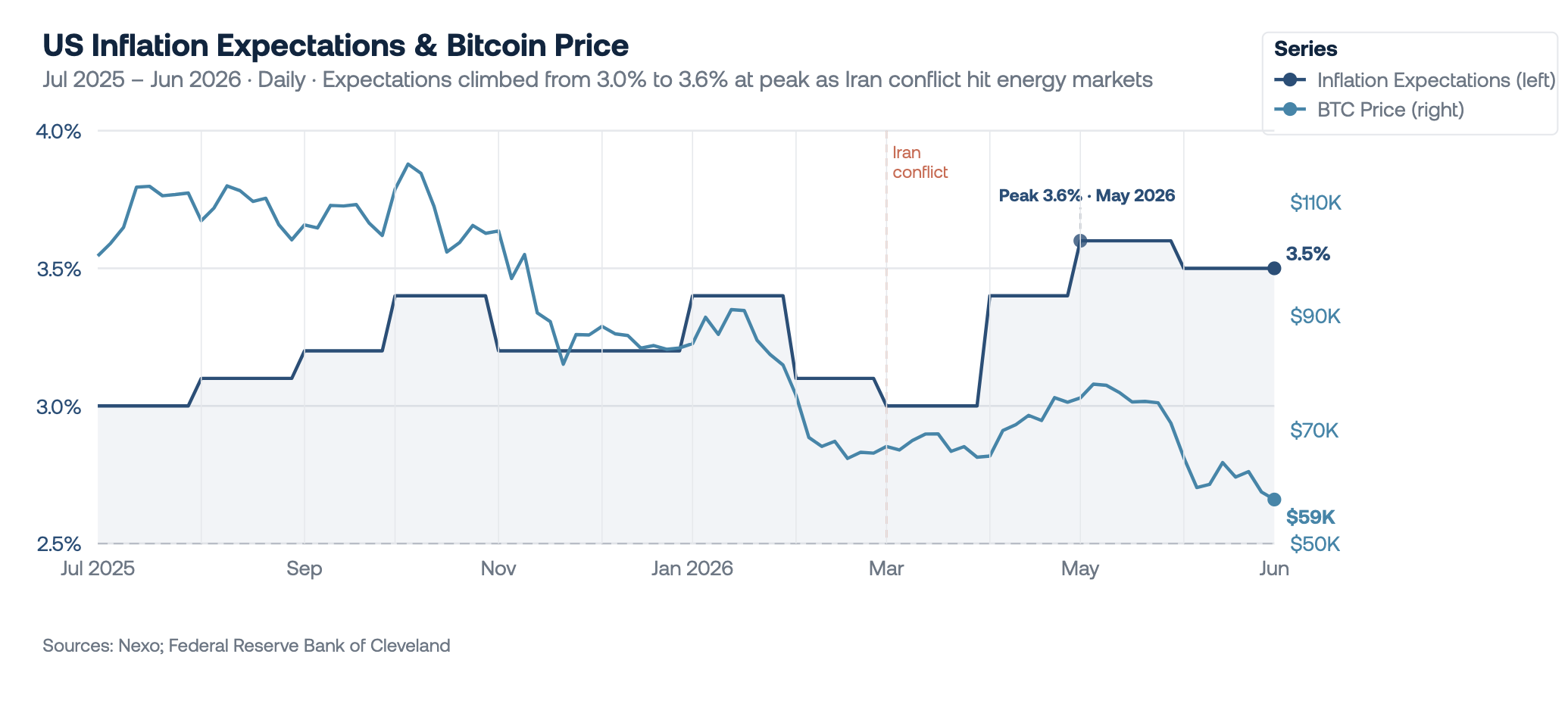

The new quarter opens with Bitcoin under modest pressure, trading above $59,000 after briefly touching a 22-month low of $57,803 earlier in the session. Equity futures are pointing slightly lower as markets await Fed Chair Warsh's first international speech at the ECB's Sintra forum — the most closely watched macro moment of the week. The total crypto market cap continues to drift near recent lows as institutional outflows show little sign of reversal. Brent crude is near $72, the dollar index is holding near 101.27, and the yen has weakened to a fresh 40-year low at 162.84 against the dollar, keeping intervention risk elevated. Eurozone CPI came in softer than expected at 2.8% in June, a constructive signal for inflation that has nudged the ECB toward a more measured stance heading into the Sintra panel.

Bitcoin

Bitcoin is trading around $59,000, having dipped to its lowest level since October 2024 earlier in the session before recovering. The quarter's defining forces — a hawkish Fed repricing and a rotation into AI-linked equities — kept Bitcoin rangebound below key levels, though the $57,000–$59,000 zone has now been tested multiple times without a decisive break lower, a sign that demand at these levels is not absent. With oil back near pre-war levels and the inflation picture gradually improving, the macro headwinds that drove the quarter's repositioning are showing early signs of easing — setting up a more constructive backdrop for Q3 if the rate narrative shifts.

Spot Bitcoin ETF outflows recorded their largest monthly total since the products launched in January 2024 — $4.5 billion withdrawn in June alone, surpassing the previous monthly record by roughly 29%. Total net assets across U.S. spot Bitcoin ETFs have fallen to around $70.9 billion, down sharply from peaks above $110 billion earlier this year. The eighth consecutive week of outflows appears likely. The CLARITY Act — a potential structural catalyst, has continued to stall in Congress, with slow progress on digital asset regulation cited as a persistent headwind alongside concerns around potential Bitcoin selling by crypto treasury companies. Today's Warsh speech at Sintra and Thursday's nonfarm payrolls are the two variables most likely to move the needle on the rate outlook that has defined Bitcoin's trajectory through the quarter.

Ethereum & Altcoins

Ethereum is at around $1,570, with XRP flat and BNB modestly lower. Solana and Cardano were relative outperformers on the session. The altcoin complex is broadly subdued, with most major assets nursing deep Q2 losses and trading below their long-term moving averages.

On the institutional side, a publicly listed Ethereum treasury firm added 10,000 ETH for around $16 million last week — its first acquisition since October — bringing its total holdings to over 886,000 ETH worth around $1.38 billion. The move is a reminder that institutional accumulation at the asset level continues even as ETF flows remain negative.

Macro & Institutional

Warsh's Sintra appearance is the session's focal point — his first international speech since taking the Fed helm and the most closely watched central bank moment of the week. Having surprised markets with a hawkish pivot at his June meeting, where nine of nineteen officials projected at least one rate hike, markets will parse his remarks for any signal on how falling oil prices and easing inflation change the rate calculus. If he reinforces the hawkish framing, the dollar would likely strengthen further and extend the headwind for risk assets. Any acknowledgement that the inflation outlook has improved meaningfully with oil back at pre-war levels would be a more constructive signal — and the first indication that the September hike narrative may be getting ahead of the data.

Today also marks the end of MiCA's transition period across the European Economic Area — the point at which crypto platforms must hold authorization or exit the market. Industry estimates suggest around 83% of platforms serving the region will not be authorised in time, concentrating client assets and trading volume toward the compliant minority. The EEA is the world's third-largest crypto-to-fiat market and has lacked a unified rulebook until today. MiCA's deadline does not move price directly, but it determines who holds the client base and institutional trust by the time price does move again — making today's transition structurally significant for Europe's crypto market over the medium term.

The interaction with ECB President Lagarde adds another dimension. Eurozone CPI came in at 2.8% in June, below the 3.0% consensus and down from 3.2% in May, with core easing to 2.4% — driven largely by a deceleration in energy costs as Brent returned to pre-war levels. The data gives the ECB room to adopt a more measured stance, but a heavily hawkish Warsh could complicate that by strengthening the dollar and effectively importing inflation back into the Eurozone — a dynamic that would force Lagarde to maintain a more restrictive posture than the data alone would warrant.

Brent is near $72, approaching pre-conflict levels. U.S. and Iranian delegations are in Doha for separate technical talks with Qatari and Pakistani mediators — direct high-level negotiations remain on hold, with Hormuz governance and Iran's nuclear programme the two unresolved sticking points. The yen has fallen to its weakest level since 1986 at 162.84, with Friday's Independence Day closure seen as a potential window for Japanese intervention given thinner liquidity. Markets are currently pricing a 67% probability of a Fed rate hike in September, up from around 20% a month ago.

On the equity side, Q2 closed with the Philadelphia Semiconductor Index posting its best quarterly performance on record, surging 87.8%, as AI infrastructure spending drove the sector to historic gains. The S&P 500 rose 14.8% for the quarter, and the Nasdaq jumped 21.4% — their best quarterly gains since 2020. The divergence with crypto's 14% quarterly decline underscores the extent to which institutional capital has rotated toward AI-linked equities with clearer near-term fundamentals.

Looking Ahead

Warsh's Sintra remarks later today are the immediate catalyst — his framing of the inflation outlook in light of falling oil will set the tone for rate expectations heading into the summer. Wednesday also brings ADP private payrolls and the ISM manufacturing PMI, both precursors to Thursday's nonfarm payrolls report — the week's defining data point. Nonfarm payrolls, the unemployment rate, average hourly earnings, and initial jobless claims all land Thursday ahead of Friday's Independence Day closure. For Bitcoin, the combination of Warsh's tone and Thursday's labour data will determine whether the current level holds as a floor into the new quarter or gives way to a deeper test of support.

Author: Iliya Kalchev, Analyst at Nexo’s Dispatch

This material is produced by Nexo for informational purposes only and does not constitute financial, investment, legal, or tax advice, or a recommendation to transact in any digital asset. Views are the author's as of the date of publication and may change without notice. Information is from sources believed reliable, but Nexo makes no warranty as to its accuracy and accepts no liability for any loss arising from reliance on this material.