How much of your portfolio should actually be in crypto?

Apr 26•6 min read

TL;DR: The 5–10% rule is a starting point, not an answer. The right crypto allocation depends on three variables: your liquidity position outside crypto, your existing asset mix, and your time horizon. Work through those three questions before comparing any numbers. If you hold crypto on a platform like Nexo that allows borrowing against your position, the effective liquidity of a larger allocation changes too.

Start with the question behind the question

Before sizing a crypto allocation, get clear on what you're trying to do with it.

Most holders buy for one of four reasons: long-term appreciation, inflation protection, active use (borrowing against holdings, earning yield), or speculation. The right allocation is different for each. A long-term appreciation thesis supports a larger, patient position. A speculative thesis supports a smaller one you're genuinely prepared to lose. If you're using crypto actively, borrowing against it through a credit line or earning daily interest, the asset is doing more work than if it's sitting in a wallet. That changes how you value holding more of it.

Getting clear on your reason is the first decision. Everything else follows.

The three-question framework

Question 1: What is your liquidity position outside crypto?

This is the variable most allocation guides skip entirely.

If you have 12 months of living expenses in a bank account and a stable income, you can hold a volatile asset through a significant drawdown without being forced to sell at the worst time. That cushion supports a larger allocation.

If your emergency fund is thin or your income is variable, a large crypto position creates a specific risk: you may need to sell during a downturn to cover something else. Selling under pressure rather than by choice is how most retail holders lock in losses they didn't need to take.

A practical threshold: crypto should not represent more of your portfolio than you could afford to see fall 70% without changing anything else about your financial life. Bitcoin fell 77% from its November 2021 peak of $69,000 to its November 2022 low of $15,500. Ethereum fell 81% over the same period. Those are not edge cases. They are the historical norm for major crypto assets in bear markets. If that scenario would mean you can't cover essentials, the allocation is too large.

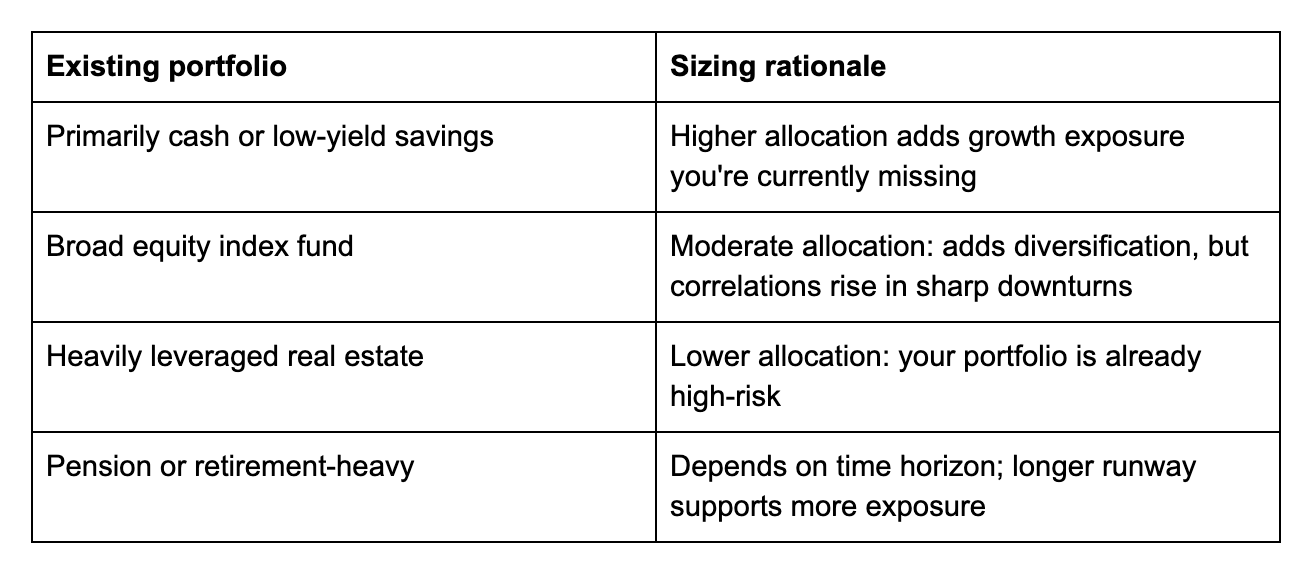

Question 2: What does your existing asset mix look like?

Crypto doesn't exist in isolation. It interacts with everything else you own.

Question 3: What is your time horizon?

Crypto's volatility is most damaging over short time horizons. If you need the money in two years, a drawdown that takes three years to recover is a real problem. If your horizon is ten years, that same drawdown is noise. Every four-year rolling period in Bitcoin's history since 2013 has closed higher than it opened, a data point worth holding in mind when calibrating how much volatility you can afford to ignore.

A rough adjustment to your base allocation:

- Under 3 years: 5% or less, or stablecoins only

- 3–7 years: 5–15% depending on liquidity and asset mix

- 7+ years: up to 20–25% is defensible for investors with strong liquidity and a genuine long-term thesis

How borrowing changes the calculation

One factor most allocation frameworks ignore: if you hold crypto on a platform like Nexo, your position isn't just a passive bet. It's an asset you can borrow against.

If you need liquidity and don't want to sell, a crypto-backed credit line lets you access funds using your Bitcoin or Ethereum as collateral, from 1.9% annual interest for eligible clients. Your holdings stay in place. If the price recovers, your full position benefits. Strategy (formerly MicroStrategy), which held approximately 815,061 BTC as of April 2026, has used a version of this logic at an institutional scale, borrowing against Bitcoin reserves rather than liquidating them to fund operations.

This doesn't mean holding more than your financial situation supports. But it does mean that for long-term holders, the availability of borrowing increases the effective liquidity of the asset, which changes the practical risk of a larger allocation.

Similarly, if you're earning daily interest on your holdings, the position generates yield while you hold. That compounds the case for sizing the allocation deliberately rather than defaulting to the smallest comfortable number.

What most people get wrong

The most common mistake isn't holding too much crypto. It's holding more than their liquidity position can absorb without forcing a sale at the wrong time.

The second is treating 5–10% as a ceiling for everyone. For a 30-year-old with a stable income, a full emergency fund, and a 10-year horizon, that range may be conservative. For someone five years from retirement with modest savings, it may be too high.

The third is not revisiting the allocation as circumstances change. A 10% position that made sense at €50,000 represents a different number, and a different psychological reality, at €200,000.

Explore crypto savings and borrowing on Nexo

Once you've sized your allocation, putting it to work matters as much as how much you hold. Flexible Savings earns daily interest on crypto and stablecoins with no lock-up. Fixed-term Savings offers higher rates for committed periods. And if you ever need liquidity without selling, Nexo's crypto-backed credit line gives you access to funds from 1.9% annual interest.

Frequently asked questions

1. How much of my portfolio should be in crypto?

It depends on your liquidity position, existing asset mix, and time horizon. The 5–10% rule is a starting point, not a ceiling or a floor. Work through the three questions above to arrive at a number that fits your situation.

2. Is 10% crypto too much?

For some people, yes. For others, no. If 10% falling 70% would force you to sell or change your financial behaviour, it's too much. If it wouldn't, 10% may be conservative depending on your time horizon and circumstances.

3. Does borrowing against crypto change how much I should hold?

It can. If you hold crypto on a platform that allows borrowing against your position, the asset has higher effective liquidity than one you can only access by selling. That changes the practical risk of holding a larger allocation.

4. How often should I rebalance?

A practical trigger is when your crypto allocation has moved more than 5 percentage points from your target due to price movements. Rising prices that push crypto from 10% to 18% of your portfolio may warrant trimming back. Falling prices that push it to 5% may warrant topping up, if your thesis is unchanged.

These materials are accessible globally, and the availability of this information does not constitute access to the services described, which services may not be available in certain jurisdictions. Rates are subject to change and may vary by region, loyalty tier, and other applicable factors. These materials are for general information purposes only and not intended as financial, legal, tax or investment advice, offer, solicitation, recommendation, or endorsement to use any of the Nexo Services and are not personalized, or in any way tailored to reflect particular investment objectives, financial situation or needs. Digital assets are subject to a high degree of risk, including but not limited to volatile market price dynamics, regulatory changes, and technological advancements. The past performance of digital assets is not a reliable indicator of future results. Digital assets are not money or legal tender, are not backed by the government or by a central bank, and most do not have any underlying assets, revenue stream, or another source of value. Independent judgment based on personal circumstances should be exercised, and consultation with a qualified professional is recommended before making any decision.