MiCA and the EU crypto market

Jul 02•6 min read

In this patch of your weekly Dispatch:

- Will BTC buyers return?

- Support in the charts

- The week’s key numbers

Market cast

BTC: Another test of support

Bitcoin's weekly chart is showing genuine technical strain. Price has broken below the 200-period SMA — a key long-term trend indicator, and is now hovering near the lower Bollinger Band, a volatility indicator, signaling the move lower has stretched further than usual. The RSI, a momentum oscillator, is approaching the 30 threshold, while the Stochastic, another momentum oscillator, is already in oversold territory – both flagging that selling pressure is becoming extended. The MACD histogram, a trend and momentum indicator, sits just below the zero line, keeping the broader trend tilted bearish for now.

The daily chart echoes that tone. Price is trading below most key moving averages and sitting close to the lower Bollinger Band, with the RSI and Stochastic oscillators both edging toward oversold readings. The one steadier note is the MACD histogram, which is holding just above the zero line — a small sign that near-term momentum hasn't fully broken down even as the broader structure stays cautious.

Key levels to watch: On the downside, immediate support sits around $59,000, with the next significant level near $55,000. To the upside, the first resistance comes in around $61,000, followed by $64,000.

The big idea

The new MiCA era

On July 1, 2026, MiCA came into force across the European Economic Area. It established a regulatory perimeter for digital asset custody, capital adequacy, and consumer protection. Within 24 hours, the market absorbed what this meant: the EEA would optimize for institutional accountability and consumer protection in digital asset services. Capital routes accordingly.

But MiCA is not unique in making this choice. Every major regulatory framework makes one. Basel prices bank capital adequacy. GDPR prices personal data protection. MiCA prices consumer protection and institutional accountability in custody. Singapore's MAS prices institutional sophistication and wealth management integration. Dubai's VARA prices operational speed and market sovereignty. Hong Kong's SFC prices settlement infrastructure and cross-border integration. Each framework is a different answer to the question: what should this market optimize for? The distinction matters because it determines which capital stays and which leaves.

The priorities

Consider what each framework requires platforms to absorb: MiCA mandates qualified custody, segregated client assets, minimum capital reserves, and enforceable grievance procedures. These are non-negotiable and costly. A platform in the EEA cannot operate without them. The cost is built into the business model. In exchange, the framework guarantees that institutional capital – pension funds, family offices, wealth managers—can be allocated to authorized platforms with the same due diligence they apply in traditional finance. Retail clients have enforceable rights. The regulator is accessible.

This pricing structure attracts specific capital: generational wealth transfers, institutional allocations, and long-term holders who value custody certainty.

What frameworks price

The capital split post-July 1 is not a flaw in MiCA. EEA retail and institutional capital that prioritizes custody certainty, regulatory accessibility, and enforceable rights concentrates under authorized MiCA platforms. This is not capital disappearing from crypto. It is capital being sorted by market design.

In traditional finance, this happened post-2008. Prime brokerage consolidated among a smaller number of highly-regulated, well-capitalized players. Higher-risk strategies, proprietary trading, and marginal capital routed to shadow banking and offshore structures. Systemic risk did not disappear—it relocated. The system became two-tiered: a regulated core and an unregulated periphery, each with its own capital sources and risk profiles.

MiCA creates the same structure.

What this reveals about market structure

The architecture is revealing because it answers a question the industry has avoided for over a decade: what does a mature digital asset market actually need? Digital assets began as a rejection of institutional gatekeeping. The original premise was that decentralized networks could replace custodians, that users could be their own banks, that regulation was unnecessary friction. A decade later, the market's answer is more complicated.

Institutional capital entering digital assets does not want to be its own bank. Pension funds do not want custody risk on their balance sheet. Family offices do not want to operate their own cold storage. Sovereign wealth funds do not want regulatory ambiguity. These institutions have options. If digital assets cannot deliver the same custody certainty, capital protection, and regulatory transparency they get in traditional finance, they do not allocate.

MiCA's pricing structure acknowledges this. It says: if you want institutional capital, you absorb the cost of custody infrastructure, capital adequacy, and regulatory compliance. The next 18 months will show which hypotheses the market validates.

The EEA consolidation effect

For the EEA specifically, July 1 forces a choice. Platforms either pay the cost of MiCA compliance or exit the market. There is no middle ground.

This creates consolidation. Smaller platforms cannot absorb the compliance cost. Marginal operators disappear. Capital concentrates under players with the scale and capital to meet minimum requirements and still compete on execution, fees, and product quality.

This is not a problem for the regulated core. Consolidation is stability. Fewer, larger, better-capitalized platforms means lower systemic failure risk and clearer customer protection. The cost is reduced competition and potentially higher fees.

The question is not whether MiCA is "good" regulation. It is whether the cost of compliance is worth the benefit of accessing EEA institutional capital. For platforms whose business model depends on that capital, the answer is yes.

The real question

MiCA reveals that regulatory frameworks do not price trust. They price market design.

Capital will route according to which optimization matches its needs. Institutional capital will split between frameworks that can deliver custody certainty, and frameworks that can deliver operational speed. Retail capital will split between regulated certainty and speculative access. Speculative capital will concentrate in non-custodial spaces where regulatory overhead is zero.

None of these flows disappears. They sort. And the next competitive cycle will be determined not by which framework is "best," but by which markets built the infrastructure to actually deliver on the priorities they priced.

Eleonor Genova, Head of Communications, Nexo

The week's most interesting data story

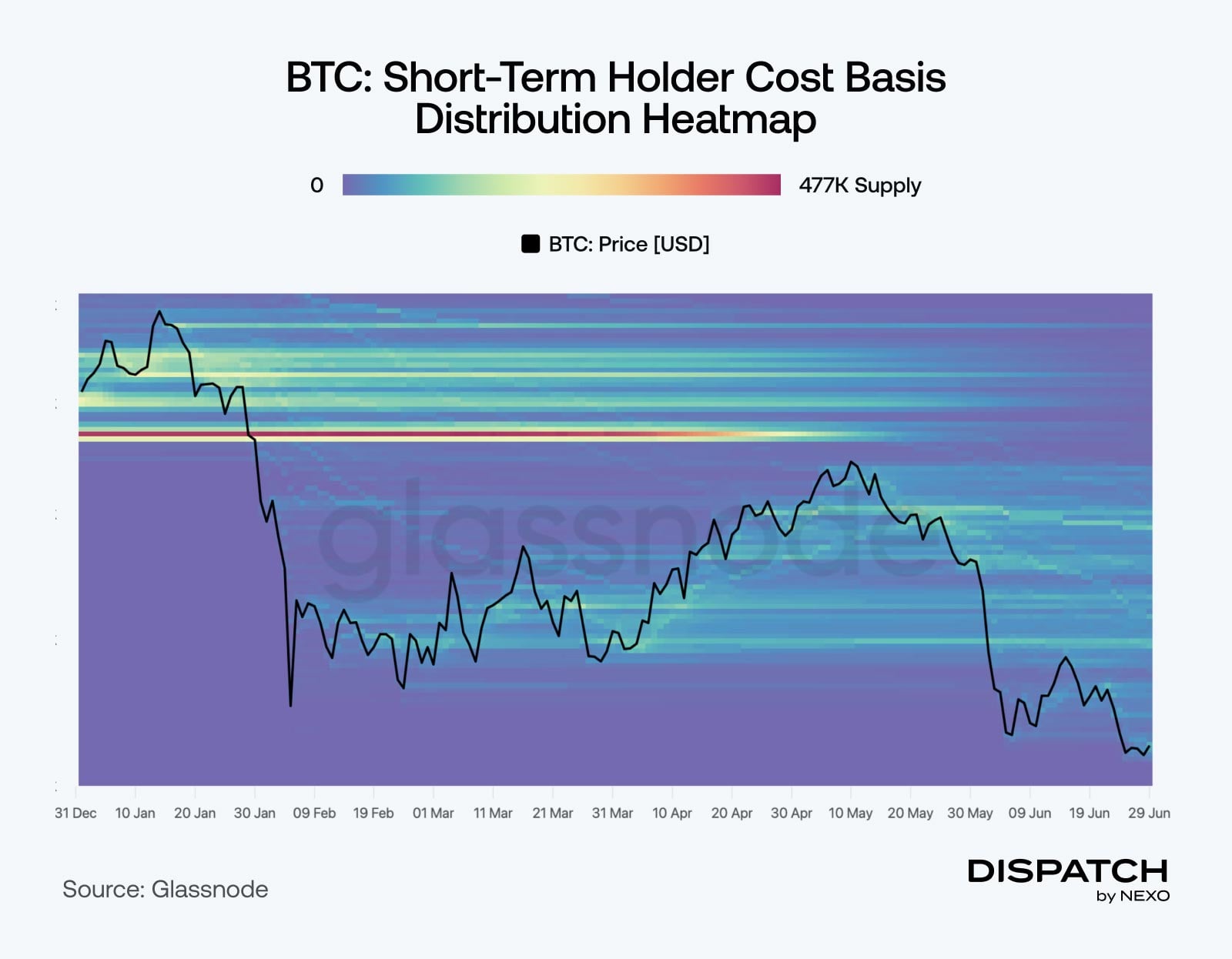

Time for BTC buyers to step in?

This week's chart shows where recent buyers got in, and why that's capping Bitcoin's upside for now. The heatmap maps short-term holder supply density across price levels — brighter bands mark where more coins were acquired. The densest cluster sits between $66,800 and $70,700, a pocket of recently bought coins now underwater. Holders near breakeven tend to sell into any bounce just to exit even, making that zone the likely ceiling for a near-term recovery. It's not permanent, though: a sustained reclaim above $66,800 would ease that pressure and open the path toward the broader Short-Term Holder Cost Basis at $71,400, the next level to watch.

The numbers

The week’s most interesting numbers

¥162/$ — The yen hit its weakest level since 1986, even as Bitcoin's correlation with it hit -0.90, the tightest since 2022 — a setup that could now favor Bitcoin if the yen rebounds.

$570 — Benchmark reiterated its $570 price target on Strategy after the company unveiled a framework to buy back shares and sell up to $1.25 billion of its 847,363 BTC if needed.

5.70 million ETH — Bitmine added 27,084 ETH last week, reaching 94% of its target of owning 5% of Ethereum's supply, and joined the Russell 1000 index.

72% — XRP's daily active addresses jumped to nearly 39,500 in two weeks, while open interest hit its lowest since July 2025 — a cleaner setup for the next move.

Hot topic

What the community is discussing

Is this the great Bitcoin consolidation?

Last week’s market correction explained.

Is an altcoin summer coming?

Dispatch is a weekly publication by Nexo, designed to help you navigate and take action in the evolving world of digital assets. To share your Dispatch suggestions and comments, email us at [email protected].