Why serious crypto holders don't sell in a downturn

May 20•6 min read

The short version

Every market cycle, the same pattern plays out: prices drop, headlines turn grim, and a wave of retail holders panic-sells. Meanwhile, a quieter group of sophisticated investors does something entirely different. They borrow against their positions, earn yield on what they hold, and wait.

When the recovery arrives, the wealth gap between these two groups widens permanently. This isn't luck—it's a calculated financial playbook that serious wealth has utilized for decades, and it is now fully accessible to crypto holders.

The emotional instinct to sell during a market decline is completely understandable—and historically, it is almost always wrong.

When an asset drops 20%, 30%, or 40%, the logic of selling feels airtight in the moment. You tell yourself you are stopping the bleeding, preserving your remaining capital, and timing a cleaner re-entry when the market finally stabilizes.

However, this short-term emotional logic completely collapses under structural scrutiny.

The triple penalty of panic selling

Selling your digital assets during a downturn inflicts three distinct operational wounds on your portfolio simultaneously:

- Permanent capitulation: It converts a temporary paper drawdown into a permanent, irreversible financial loss.

- Forfeiting the rebound: It completely removes you from the subsequent recovery phase, which historically happens faster than most market participants anticipate.

- Tax liabilities: In most jurisdictions, selling triggers a taxable disposal event. You are forced to navigate tax compliance on a degraded asset.

Note: Tax treatment varies significantly by region—always consult a qualified tax professional regarding your specific situation.

The speed and scale of crypto recoveries are routinely underestimated. For instance, Bitcoin fell 77% between November 2021 and November 2022, only to rally and secure a major all-time high of $125,071 in October 2025.

Every major crypto asset that has survived its first five years has successfully recovered from its worst drawdowns. The investors who captured those massive recoveries were simply the ones who refused to liquidate at the bottom.

If your core investment thesis has fundamentally changed, exiting makes sense. But if the asset’s utility remains intact, the network is secure, and the only variable that changed is a temporary spot price, the case for selling might be incredibly weak.

What serious wealth has always done instead

There is a reason why ultra-high-net-worth families don't liquidate their prime assets when markets drop. It isn't stubbornness; it’s an institutional framework known colloquially as "Buy, Borrow, Die." This strategy has been a cornerstone of multi-generational wealth preservation for over a century.

The operational logic is straightforward:

- Accumulate: You buy high-conviction assets with long-term appreciation potential.

- Leverage: When you need real-world liquidity, you borrow against your assets instead of selling them.

- Preserve: The underlying asset remains in your portfolio, continuing to compound and appreciate, while you repay the line of credit over time.

Legacy institutions like JP Morgan, Fidelity, and Charles Schwab routinely offer securities-based lending to private banking clients for this exact purpose.

To put this in perspective, Bank of America's wealth management division alone held over $50 billion in structured and asset-backed loans at the end of 2022—right in the middle of one of the worst traditional market downturns in a decade. The wealthy weren't selling their equities at a discount; they were borrowing against them.

This strategy works because of a basic asymmetry: selling is irreversible. Once you forfeit your position at a depressed price, you are locked out. Borrowing preserves your optionality. You access immediate liquidity while keeping your long-term upside intact.

Applying the institutional playbook to crypto

The exact same lending mechanics previously reserved for elite private banking clients are now available natively within the crypto ecosystem—and they are significantly more accessible.

Through platforms like Nexo, you can open a crypto-backed credit line using BTC, ETH, SOL, XRP, and other major digital assets as collateral, with borrowing rates starting from 1.9% interest per year.

You receive instant funds with no repayment schedules or credit checks, and your holdings are unlocked the moment the line of credit is settled.

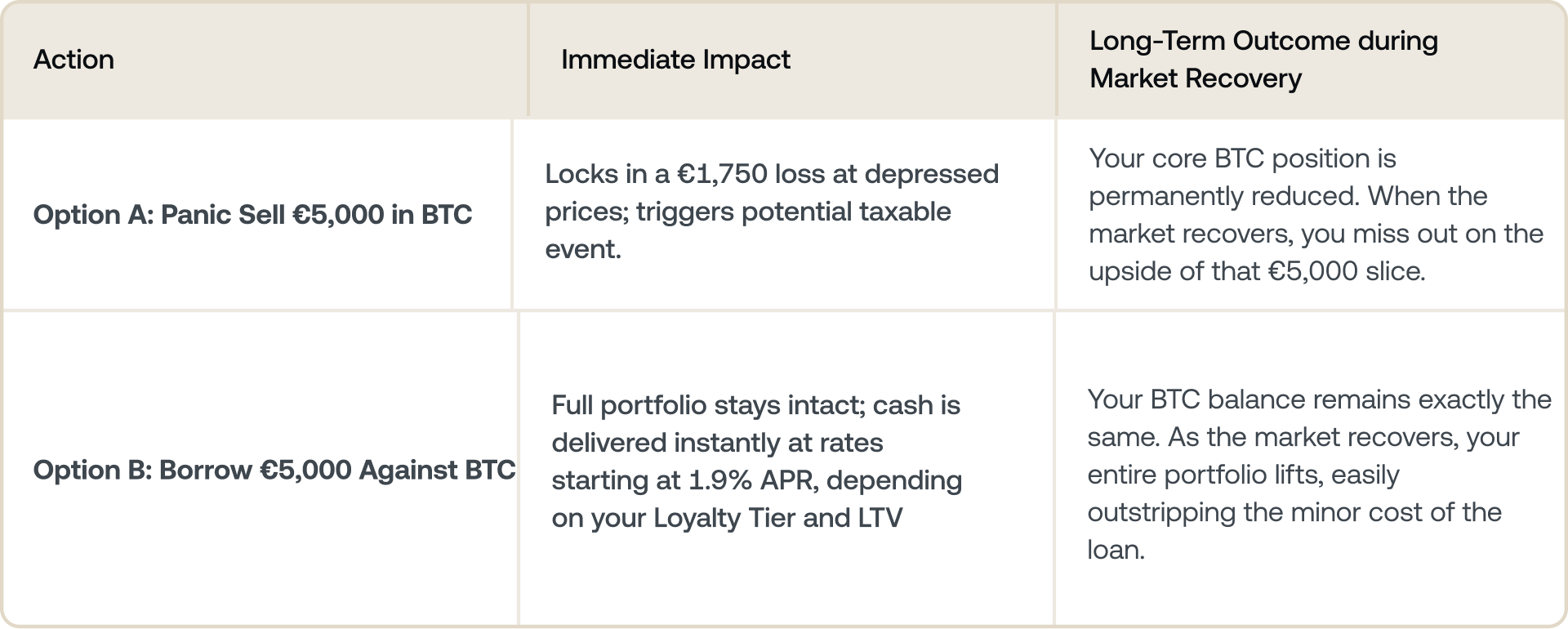

Real-world blueprint: Selling vs. borrowing

Imagine you hold €30,000 in BTC. The market experiences a standard crypto correction of 35%, temporarily compressing your portfolio value to €19,500. Suddenly, you hit an unexpected real-world expense—a €5,000 tax bill or business cost.

Here is how your choices look side-by-side:

The flip side: Managing your liquidation risk

While borrowing allows you to ride the market recovery, it is not without risk. Because crypto can be highly volatile, you must navigate the mechanics of leverage safely:

- Understanding LTV (Loan-to-Value): When you borrow €5,000 against your remaining €19,500 in BTC, your initial LTV sits at around 25.6%. The higher the LTV, the riskier the loan.

- The Threat of Margin Calls: If BTC prices continue to slide further down, your LTV ratio will rise. If it hits the platform's risk threshold, you will receive a margin call requiring you to either add more collateral or pay down a portion of the loan to stabilize your account.

- The Danger of Liquidation: If the market drops sharply and you fail to respond to a margin call, the system will automatically liquidate (sell) a portion of your BTC at depressed prices to cover the loan. This forces you into the exact scenario you were trying to avoid with Option A: locking in permanent losses.

Pro-Tip: Borrow Conservatively. The golden rule of crypto backing is to never borrow to your maximum limit. Maintain a low LTV buffer so your portfolio can comfortably weather sudden market dips without triggering a liquidation event.

Make your assets work

The borrow mechanic solves the liquidity puzzle. However, a comprehensive bear market playbook requires a secondary component: optimization. The strategic assets you are not spending should be actively generating yield while sitting out the storm.

Leaving BTC or ETH completely idle in a cold wallet during a prolonged market correction is a missed opportunity. Transitioning those holdings into a high-yield environment builds an automated cushion against falling prices.

On Nexo, utilizing Flexible Savings balances absolute liquidity with premium daily payouts:

- BTC: Up to 5.7% annual interest

- ETH: Up to 5.25% annual interest

- USDC: Up to 9.5% annual interest

For investors looking to temporarily de-risk without completely exiting into legacy bank accounts, allocating a portion of capital into dollar-pegged stablecoins like USDC or USDT is a highly coherent strategy.

Your capital remains stable, generating daily compounding yield while you wait for macro conditions to clear. When you detect a market turnaround, you can instantly swap back into BTC or ETH right inside the ecosystem.

Want your portfolio to outpace market corrections? Stop holding static assets and start earning daily compounding interest.

These materials are accessible globally, and the availability of this information does not constitute access to the services described, which services may not be available in certain jurisdictions. These materials are for general information purposes only and not intended as financial, legal, tax, or investment advice, offer, solicitation, recommendation, or endorsement to use any of the Nexo Services and are not personalized or in any way tailored to reflect particular investment objectives, financial situation, or needs. Digital assets are subject to a high degree of risk, including but not limited to volatile market price dynamics, regulatory changes, and technological advancements. The past performance of digital assets is not a reliable indicator of future results. Digital assets are not money or legal tender, are not backed by the government or by a central bank, and most do not have any underlying assets, revenue stream, or other source of value. Independent judgment based on personal circumstances should be exercised, and consultation with a qualified professional is recommended before making any decision.