APR vs APY: What the difference actually means for your crypto

Apr 01•5 min read

You see a rate. But which rate is it?

You open a crypto platform. It says 8%. Eight percent sounds clear enough.

But eight percent of what, calculated how, paid out when? The answer changes the actual money that lands in your account.

APR and APY are two different ways of expressing the same underlying interest rate — and the gap between them isn't just a technicality. In crypto, where yields compound daily, and borrowing costs stack up fast, the difference matters more than it does in a standard savings account.

Here's what each one means, and why you need to know which one you're looking at.

APR: the rate before compounding

APR stands for Annual Percentage Rate. It's the base interest rate for a year, with no compounding factored in.

If a product says 12% APR, that's 1% per month. Nothing more.

APR tells you the cost of borrowing. What it doesn't account for is what happens when interest earned is added back to your balance and starts earning interest itself.

That's where APY comes in.

APY: the rate after compounding

APY stands for Annual Percentage Yield. It takes the same base rate and factors in how often interest is added to your balance — daily, weekly, or monthly — and compounds it forward over a year.

The more frequently interest compounds, the higher the APY relative to the APR.

A simple example:

- Base rate: 12% APR, compounded monthly

- APY: ~12.68%

The difference here is small. But at higher rates, or with daily compounding (which is common in crypto), the gap widens. A 50% APR compounding daily becomes roughly 64.8% APY.

This is why APY is the number platforms use when they want to show you your earning potential. It's the fuller picture.

Why crypto platforms use both — and when each one applies

In traditional finance, you mostly see APY on savings accounts and APR on loans. Crypto follows the same logic, just faster.

When you're earning: Platforms quote APY because your yield compounds. If you deposit 1 BTC and earn 5% APY, your effective return is higher than 5% APR — because the interest paid out gets reinvested (or compounds automatically) through the year. For a deeper look at earning methods, see how to earn interest on crypto.

When you're borrowing: Loan and credit line rates are typically quoted as APR — the simple annualized cost of what you owe. This makes it easier to compare borrowing costs across products without compounding effects distorting the comparison.

The compounding frequency question

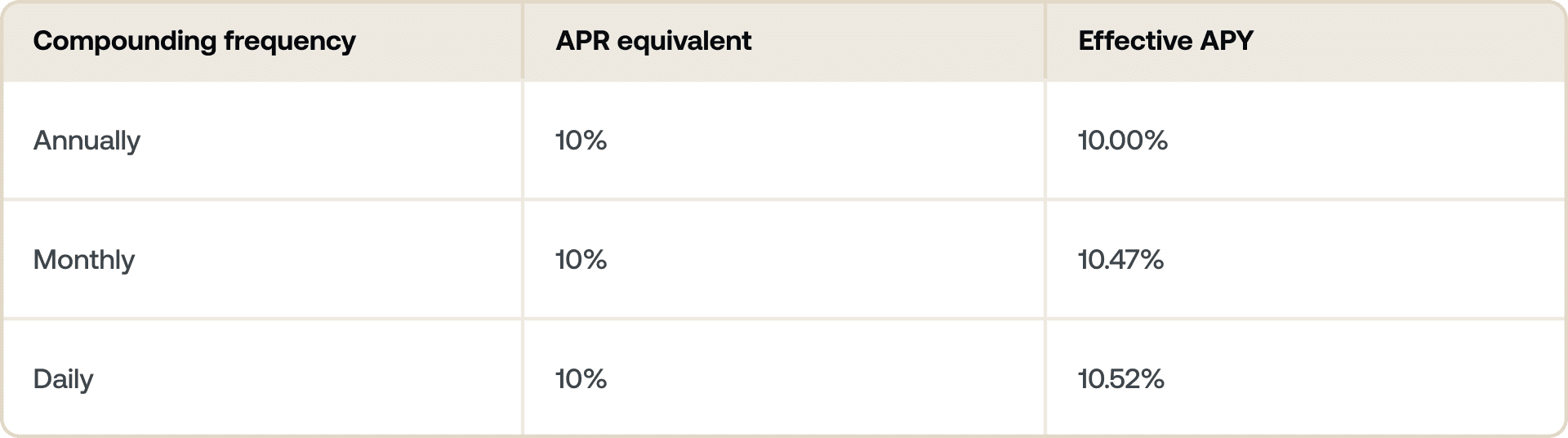

Not all APY figures are created equal. The compounding frequency matters.

Daily compounding means your APY will always be slightly higher than your APR for the same base rate. The difference isn't dramatic at low rates, but it grows as the base rate climbs.

When comparing two platforms quoting different APY figures, it's worth checking whether they compound daily, weekly, or monthly. The higher APY headline isn't always better if one compounds less frequently.

If you're also weighing whether to lock funds for a fixed term or keep them flexible, see our dedicated article Flexible vs. Fixed-term Savings: What's the difference.

Earning vs. borrowing on the same asset

Say you hold ETH and you want to put it to work without selling.

You deposit your ETH into an earning product at 4% APY, compounding daily. Over 12 months, your ETH position grows — the APY reflects the full compounded return you'll receive.

At the same time, you take a crypto-backed loan at 10.9% APR. This is your annual cost of borrowing. You know exactly what you're paying to access liquidity without selling.

The two numbers serve different purposes. APY tells you what you'll earn. APR tells you what you'll pay.

Running both gives you the full picture: the net cost or benefit of a leveraged crypto position.

What to watch for when comparing platforms

A few things worth checking before taking a rate at face value:

- Is the rate fixed or variable? APY figures in crypto often change based on market conditions, demand, or protocol governance. Fixed terms tend to lock the rate.

- How often does it compound? Daily compounding means a higher effective yield than weekly or monthly for the same base rate.

- Is the quoted rate the APY or just the APR? Some platforms quote base rates without compounding.

- Are there conditions? Loyalty Tiers, lock-up periods, or minimum deposit thresholds can affect the actual rate you receive.

How Nexo shows rates

On Nexo's earn products, rates are quoted as APY, reflecting the compounded return on your crypto. You can earn industry-leading rates on assets like BTC, ETH, XRP, USDC, and more — check nexo.com/earn-crypto for current rates.

For the Nexo Credit Line, borrowing costs are quoted as APR, giving you a clear, simple annual rate to work with when you're accessing liquidity against your portfolio. See current borrowing rates at nexo.com/borrow.

These materials are accessible globally, and the availability of this information does not constitute access to the services described, which services may not be available in certain jurisdictions. Rates are subject to change and may vary by region, loyalty tier, and other applicable factors. Always refer to the Nexo app for your applicable rates. These materials are for general information purposes only and not intended as financial, legal, tax, or investment advice, offer, solicitation, recommendation, or endorsement to use any of the Nexo Services and are not personalized, or in any way tailored to reflect particular investment objectives, financial situation or needs. Digital assets are subject to a high degree of risk, including but not limited to volatile market price dynamics, regulatory changes, and technological advancements. The past performance of digital assets is not a reliable indicator of future results. Digital assets are not money or legal tender, are not backed by the government or by a central bank, and most do not have any underlying assets, revenue stream, or other source of value. Independent judgment based on personal circumstances should be exercised, and consultation with a qualified professional is recommended before making any decision.