Markets Today - May 21, 2026

May 21•4 min read

Daily analysis of crypto markets and the forces shaping them, from the Nexo research desk.

Hawkish Fed minutes cap the de-escalation trade

Bitcoin trades slightly above $77,000 Thursday afternoon as markets digest renewed U.S.-Iran de-escalation headlines. U.S. equities rallied and oil sold off Wednesday on reports that Washington and Tehran are in final-stage talks. Despite an after-hours beat-and-raise and an additional $80 billion buyback authorization, Nvidia slipped around 1% in extended trading. The de-escalation trade remains more measured than the first attempt in early May, capped by a hawkish read of the April FOMC minutes that reinforced the higher-for-longer narrative.

Bitcoin

Bitcoin traded in a $76,700–$78,000 range on May 20, swinging on Iran de-escalation headlines, the hawkish FOMC minutes from the April 28–29 meeting, and NVIDIA's after-hours earnings beat. The largest move followed the NVIDIA print. Bitcoin rallied from $77,657 at the NYSE close to a session high of $78,013 by 11 PM ET, before being rejected at the $78,000 handle and fading to $77,545.

Macro remains the major short-term price driver. U.S. spot Bitcoin ETFs have shed $1.84 billion across the six sessions since the April CPI print on May 13, ending a two-and-a-half-month inflow run that had added $4.4 billion to the complex from February's through early May. Spot order flow tells the same story. Bitcoin saw nine consecutive sessions of net selling from May 12 through May 20, totaling roughly $1.2 billion in sell aggression. The streak broke on May 21 as the NVIDIA earnings bid drew in $98 million from buyers. Immediate resistance sits at $78,000. Above that, the $80,000–$80,300 short-term holder realized price band is the next material level. Initial support is the $76,700 range low; a loss exposes $74,200.

Ethereum & Altcoins

All three majors traded slightly higher overnight but the month-level picture diverges sharply. ETH is at $2,137, up 0.3% on the session and down 5.4% in May. SOL trades at $86.80, up 2.2% overnight and up 4.4% on the month. XRP is at $1.38, up 0.8% intraday and broadly flat in May.

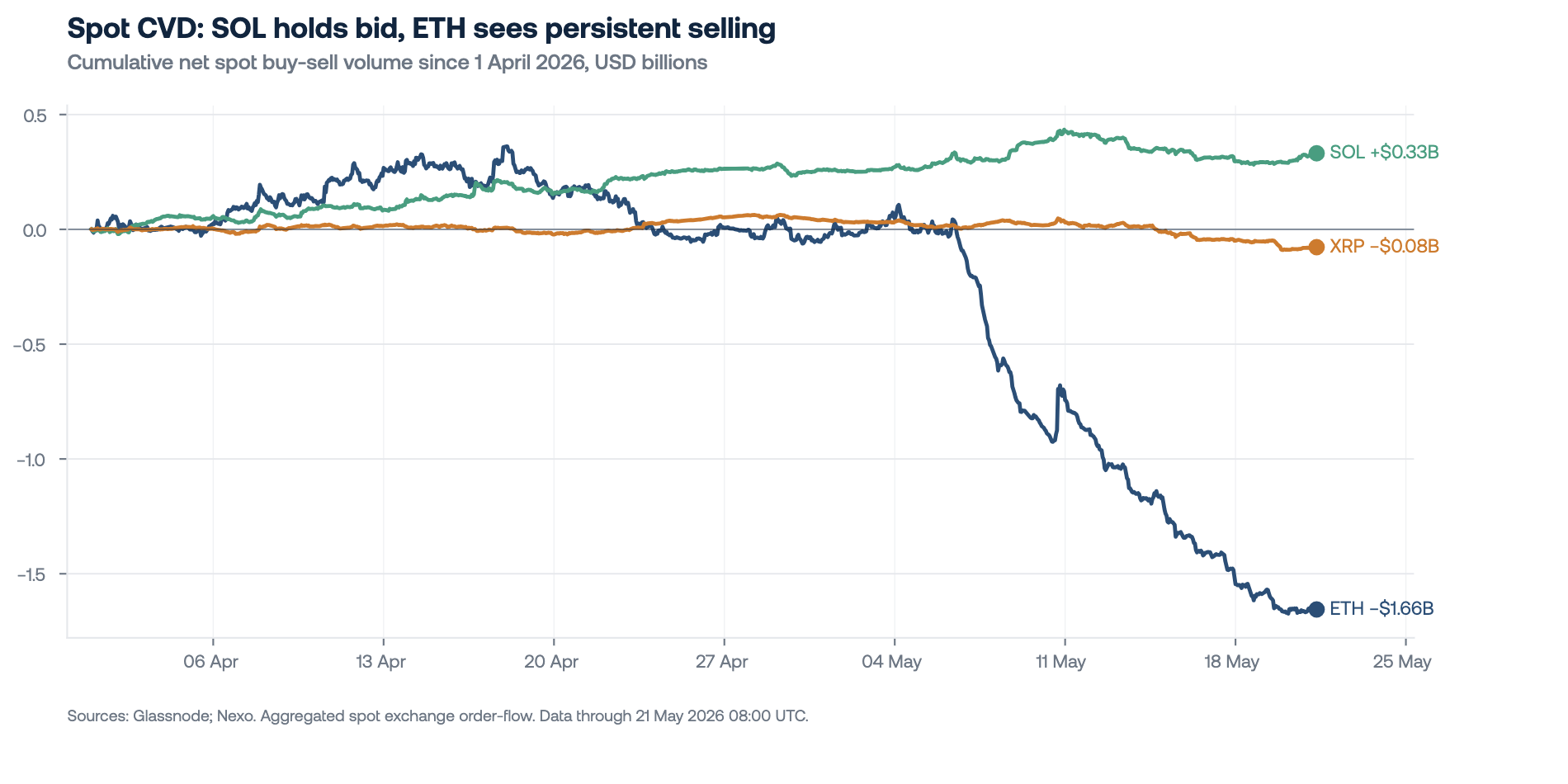

The institutional signal tracks the price action. Spot ETH ETFs recorded their eighth consecutive session of net outflows on May 20, taking the May running total to $260 million in outflows. Over the same period, SOL and XRP ETFs absorbed $103 million and +$98 million in inflows, respectively. Spot order flow tells the same story: aggregated spot CVD for ETH has fallen by $1.66 billion since April 1, with the breakdown accelerating in early May. SOL CVD added $0.33 billion and XRP held broadly flat.

The configuration is consistent with rotation rather than broad altcoin de-risking. Capital that left ETH did not exit the complex.

Macro & Institutional

Macro remains the dominant driver. Brent crude fell 5.2% to $105.5 on May 20 as Iran de-escalation hopes built, well below April's $117 average, yet 10-year Treasury yields stayed at a one-year high. The curve is pricing inflation persistence even as the geopolitical risk premium starts to fade. The April 28–29 FOMC minutes, released Wednesday at 2 PM ET, ran more hawkish than the statement implied. Many participants would have preferred to drop the bias language outright, citing upside inflation risks from oil, tariffs and Middle East tensions. The majority signaled that further firming would likely become appropriate if inflation persists above 2%, with some discussion that the next move could be a hike rather than a cut.

While the inflation channel dominates headline sentiment, the growth side is starting to crack. The flash Eurozone composite PMI fell to 47.5 in May from 48.8 in April, a 31-month low and second consecutive contraction. Services drove the drop to 46.4, the weakest since February 2021, as the cost-of-living squeeze from war-related energy prices weighs on consumer demand. The Middle East shock is no longer only an inflation story, it is becoming a demand story.

Looking Ahead

Today's calendar centers on global flash PMIs for May from the Eurozone, UK and U.S., providing a growth check against the Fed's higher-for-longer signal. U.S. data also includes initial jobless claims, the Philly Fed manufacturing index, April housing starts and building permits, plus the Atlanta Fed GDPNow update (Q2 tracking at 4.0%). Fed's Barkin speaks this evening, with Waller following Friday, the first scheduled Fed commentary after the minutes. Friday brings Japan's national CPI, the next test of BoJ hike timing after Tuesday's stronger-than-expected Q1 GDP. The University of Michigan consumer sentiment and inflation expectations released later that day will be read for signs that household inflation expectations remain anchored, a concern flagged directly in the FOMC minutes.

Author: Dessislava Ianeva, Analyst at Nexo’s Dispatch

This material is produced by Nexo for informational purposes only and does not constitute financial, investment, legal, or tax advice, or a recommendation to transact in any digital asset. Views are the author's as of the date of publication and may change without notice. Information is from sources believed reliable, but Nexo makes no warranty as to its accuracy and accepts no liability for any loss arising from reliance on this material.