Markets Today - June 8, 2026

Jun 08•4 min read

-1.png)

Daily analysis of crypto markets and the forces shaping them, from the Nexo research desk.

Bitcoin steadies as Strategy steps back in and the macro picture shifts

The crypto market is finding its footing after last week's pressure, with the total crypto market cap recovering modestly as Bitcoin climbs back above $63,000 and altcoins post measured gains. The macro backdrop remains complex: Iran and Israel exchanged strikes over the weekend for the first time since the April ceasefire, sending oil higher and adding a layer of uncertainty to an already active backdrop. Yet markets are absorbing the news with relative composure — S&P 500 futures are up 0.6%, Nasdaq futures are gaining 1.3% as chip stocks stabilize, and Iranian state media has reported an end to military operations against Israel. Brent crude is up 1.1% to around $94, the dollar index is holding near a two-month high at 100.17, and gold has slipped to around $4,326 as higher-for-longer rate expectations continue to weigh on bullion. Wednesday's CPI print and Thursday's ECB rate decision are the week's defining data points.

Bitcoin

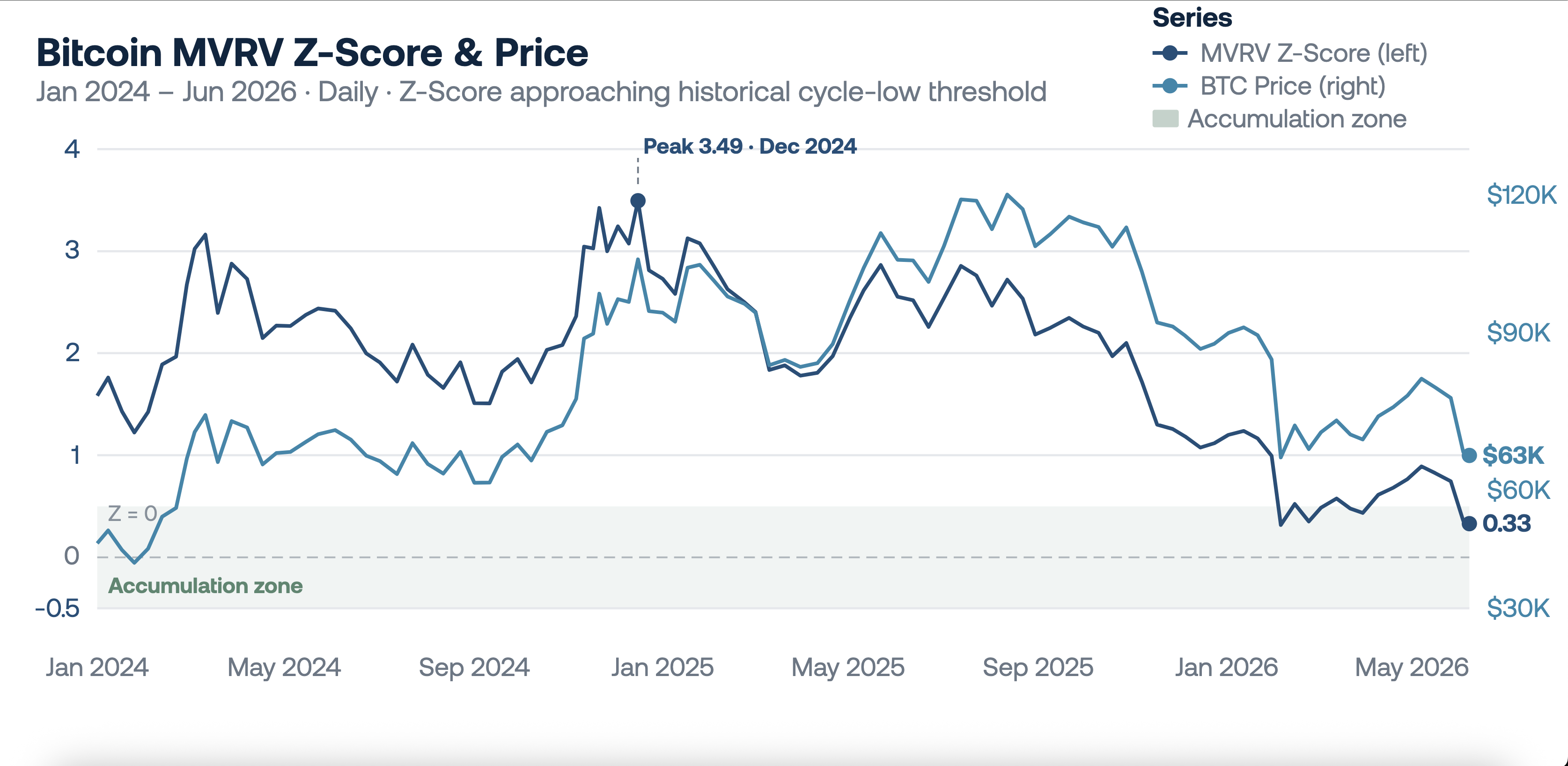

Bitcoin is trades just below $64,000, up almost 3% in 24 hours and recovering from last week's low below $60,000. Two developments are supporting the rebound. First, Strategy has returned to buying — purchasing 1,550 BTC for approximately $101 million at an average price of $65,332, bringing total holdings to 845,256 BTC. The acquisition, the first since last week's symbolic sale, reaffirms the corporate accumulation model that briefly came into question and adds meaningful institutional weight to the current price level. Second, one of Bitcoin's closely watched on-chain metrics — the MVRV Z-Score, is approaching the zone that has historically coincided with major cycle lows, having touched or briefly dipped below zero in 2014, 2018, and 2022 before significant recoveries followed.

Spot Bitcoin ETFs recorded $1.72 billion in net outflows last week, their largest weekly exodus since February 2025, extending a four-week outflow streak totalling $5.4 billion. The primary driver was last week's stronger-than-expected jobs report, which reinforced higher-for-longer rate expectations and made yielding assets more attractive relative to Bitcoin. That said, the institutional ownership base has broadened meaningfully — 61% of circulating Bitcoin supply has remained inactive for more than a year per Glassnode, and corporate treasury accumulation has provided a meaningful offset to ETF outflows. $60,000 remains the key support level — Bitcoin briefly touched it last week before recovering, and holding above it is the near-term priority.

Ethereum & Altcoins

Ethereum is up 3.4% to around $1,666, outperforming Bitcoin on the day and recovering from last week's multi-month lows. XRP and Solana each rose 1.3%, Cardano and BNB each added around 1%. The recovery is measured rather than decisive as the altcoin complex is broadly tracking Bitcoin's rebound without yet establishing independent momentum. The $1,420 level remains the key reference for Ethereum — a sustained hold above it keeps the current recovery thesis intact.

Macro & Institutional

The weekend's Iran-Israel exchange marks the first direct strikes between the two since the April ceasefire, introducing a new layer of geopolitical uncertainty into an already complex macro environment. President Trump maintained that a peace deal remains on the table. Brent crude is up on the session, with markets pricing a widening gap between diplomatic optimism and operational reality.

The week's most consequential institutional development outside of geopolitics is Goldman Sachs pushing its Fed rate cut forecast into 2027, citing the stronger labour market and persistent inflation pressures from energy costs and tariffs. Goldman now expects core PCE to remain above 3% throughout 2026, with cuts resuming only as inflation approaches 2% the following year. European markets are also navigating the ECB's expected rate decision Thursday, with traders pricing as many as three hikes by year-end as eurozone bond yields hit multi-week highs. Asian markets bore the brunt of Friday's risk-off move, with South Korea's Kospi falling 8.3%, Japan's Nikkei dropping 3.85%, and Taiwan's TAIEX declining 3.5%.

Looking Ahead

Wednesday's CPI print is the week's defining moment, where any surprise in either direction would move rate expectations and by extension crypto, equities, and yields simultaneously. Tuesday brings ADP employment as an early read on the labour market. Wednesday also brings the Bank of Canada rate decision and a 10-year Treasury auction in the afternoon. Thursday is the week's busiest day: the ECB rate decision, U.S. PPI, initial jobless claims, and the OPEC monthly report all land together, forming a near-complete picture of where energy, inflation, and growth stand heading into summer. UK GDP rounds out the week on Friday. For Bitcoin, Wednesday's CPI is the most direct near-term catalyst — a contained reading would provide relief, while an upside surprise would keep the pressure on the $60,000 support level that matters most heading into Warsh's first FOMC meeting on June 17.

Author: Iliya Kalchev, Analyst at Nexo’s Dispatch

This material is produced by Nexo for informational purposes only and does not constitute financial, investment, legal, or tax advice, or a recommendation to transact in any digital asset. Views are the author's as of the date of publication and may change without notice. Information is from sources believed reliable, but Nexo makes no warranty as to its accuracy and accepts no liability for any loss arising from reliance on this material.