Dispatch #271: Crypto’s Big Four: What reignites the comeback move?

Nov 18, 2025•7 min read

In this patch of your weekly Dispatch:

- The Fed’s December cut odds

- BTC’s demand side

- Asia’s crypto advance

Market cast

Bitcoin: The support zone test

On the weekly chart, Bitcoin has slipped below the lower Bollinger Band—a volatility gauge that measures how far price has moved from its average—underscoring the current bearish tone. Momentum indicators align with this view: the Stochastic oscillator remains deep in oversold territory, the MACD histogram is negative and still declining, and the RSI is nearing 30, all pointing to stretched downside conditions. On the daily chart, the 50-day simple moving average has moved below the 200-day, a signal that typically reflects waning short-term momentum but often lags behind actual price action.

Daily oscillators tell a similar story, with both RSI and Stochastic deeply oversold and the MACD holding below zero. Immediate support lies around $91,000–$90,000, with stronger footing near $85,000–$84,000, while resistance stands at $96,000 and the psychological $100,000 level.

The big idea

BTC, ETH, SOL and XRP: Recovery beneath the surface

Dispatch puts the crypto majors back in focus. Not for their volatility, but for what they each bring and ultimately – what could see them rise again. The October derivatives correction, the U.S. government shutdown, and a macro unwind left markets bruised but not broken. Beneath the surface, adoption, institutional engagement, and sovereign interest keep advancing. With cleaner positioning and policy turning favorable, Bitcoin, Ethereum, XRP, and Solana are entering a phase where fundamentals matter more than leverage. The comeback story is less about chasing highs and more about watching crypto’s pillars quietly re-anchor the next cycle.

Bitcoin: After weeks that peeled off its year-to-date gains, Bitcoin’s slide to $94,000 looks more like recalibration. The 43-day U.S. shutdown and tariff tensions hurt sentiment, but adoption momentum is intact. In Washington, the most pro-crypto administration on record has backed new ETFs, clearer regulation, and a surge in corporate treasury demand. Research firm Bernstein argues the pullback stems from cycle psychology.

Many investors expected a fourth-quarter weakness, with the typical post-peak pattern, but this time the market looks fundamentally stronger. Around 340,000 BTC, worth $38 billion, has been distributed by long-term holders in the past six months, yet most of it has been absorbed by ETF inflows and corporate treasuries, which together have added roughly $34 billion in demand. Institutional ownership of Bitcoin ETFs has climbed to 28%, up from 20% last year, underscoring what Bernstein calls “higher quality and consistent ownership.” Elsewhere, the Czech National Bank’s $1 million pilot, mainly Bitcoin, with stablecoins and tokenized deposits, marks the first step by a European central bank toward integrating digital assets into reserves. It’s a small but symbolic leap from observation to experimentation. Meanwhile, on-chain data shows whale selling typical of late-cycle profit-taking, not capitulation. With leverage flushed, ETF flows steady, and macro policy softening, Bitcoin’s next rally is likely quieter but more durable.

Ethereum: Ethereum’s consolidation may be setting up the start of its own cycle. Tom Lee of BitMine says ETH is “embarking on the same path” that saw Bitcoin multiply a hundredfold since 2017. Like early Bitcoin, ETH’s progress is uneven – down about 35% from its August high of $4,946, but conviction may be building. Roughly 17 million ETH flowed into long-term wallets this year, raising their total to 27 million from 10 million in January. At around $3,100, ETH trades near the cost basis of these holders, a level that has historically marked strong accumulation zones. The next Fusaka upgrade promises real gains in speed and usability, while Ethereum’s dominance in stablecoins and tokenized assets keeps it central to digital finance. If activity and institutional inflows rebound, the groundwork for a sustained recovery – and perhaps a long supercycle, will already be in place.

Ripple’s XRP: XRP’s long-awaited return to mainstream finance is underway. The first U.S. spot XRP ETF, trading as XRPC, puts it alongside Bitcoin, Ethereum, and Solana as part of the ETF era’s core group. It’s a landmark moment for Ripple, once defined by regulatory conflict but now buoyed by shifting policy winds. Institutional demand is growing fast: new treasury platforms plan to raise over a billion dollars in XRP-backed products, and derivatives positioning remains bullish. Ripple’s expanding payments network adds real utility to the narrative. Yet near-term data show a market caught between conviction and caution: short-term holders are actively buying the dip, but long-term investors have increased selling to keep momentum muted. Technically, XRP needs a decisive move above $2.38 to regain a bullish structure, while losing $2.06 would invalidate it. If ETF inflows hold and cross-border volumes rise, XRP’s next chapter could be defined by adoption, not litigation.

Solana: Solana remains the network institutions can’t ignore. Even as SOL fell to about $140 – its lowest since June as the asset has logged 14 straight days of ETF inflows, adding $12 million last week and lifting cumulative totals past $370 million. That consistency, despite wider market redemptions, highlights deepening institutional confidence in Solana’s role as the fastest, user-ready blockchain. Reliability has improved, throughput remains unmatched, and development in payments, gaming, and DePIN keeps expanding. The ETF bid is strengthening liquidity and setting a solid base for recovery. If the network maintains stability through high-traffic periods and continues scaling its real-world ecosystem, this correction could prove a mid-cycle reset before renewed momentum – an opportunity for investors positioning for the next adoption wave.

Together, the Big Four in crypto stand in a consolidation. Leverage has been flushed, infrastructure is advancing, and adoption from central banks to corporates is shifting from resistance to readiness. If that trend holds, this correction may mark not the end of the cycle, but the beginning of its next, more mature phase.

Macroeconomic roundup

Is the December cut still on the map?

Investor confidence in a December Federal Reserve rate cut has eroded sharply, with 46% of traders now expecting a move – down from 67% a week ago, CME data shows. The shift comes as markets digest October’s 25 bps cut, which was fully priced in and failed to lift risk assets, including crypto. Fed Chair Jerome Powell has since stressed that “policy is not on a preset course,” signaling a more cautious, data-driven stance as inflation remains sticky and the labor market strong.

The fading odds reflect a broader recalibration: investors who once expected multiple cuts in 2025 are now bracing for a slower, more measured easing cycle. With liquidity staying tight and risk appetite subdued, both equities and digital assets may remain under pressure until the next reading. Until the Fed signals a clearer path toward sustained rate relief, the risk-on momentum traders have been waiting for will likely stay on hold.

TradFi trends

Asia: Where tokenization and regulation move

Asia’s leading financial centers are accelerating their digital-asset agendas. In Hong Kong, the Monetary Authority has launched the pilot phase of Project Ensemble, moving from sandbox testing to real-value tokenized transactions. Running through 2026, the program will test tokenized money-market funds and real-time liquidity management, with plans to expand toward 24/7 interbank settlement in tokenized central bank money. HKMA chief Eddie Yue called the launch “where innovation meets implementation,” as both Hong Kong and Singapore advance interoperability in tokenized finance.

In Japan, the Financial Services Agency plans to reclassify 105 cryptocurrencies, including Bitcoin and Ether, as financial products under securities law while cutting the top tax rate on crypto income from 55% to 20% to align with stock investments. The reforms, expected to take effect by 2026, mark Japan’s shift toward a Web3-ready financial framework with clearer rules, stronger oversight, and more competitive taxation to attract global capital.

The week’s most interesting data story

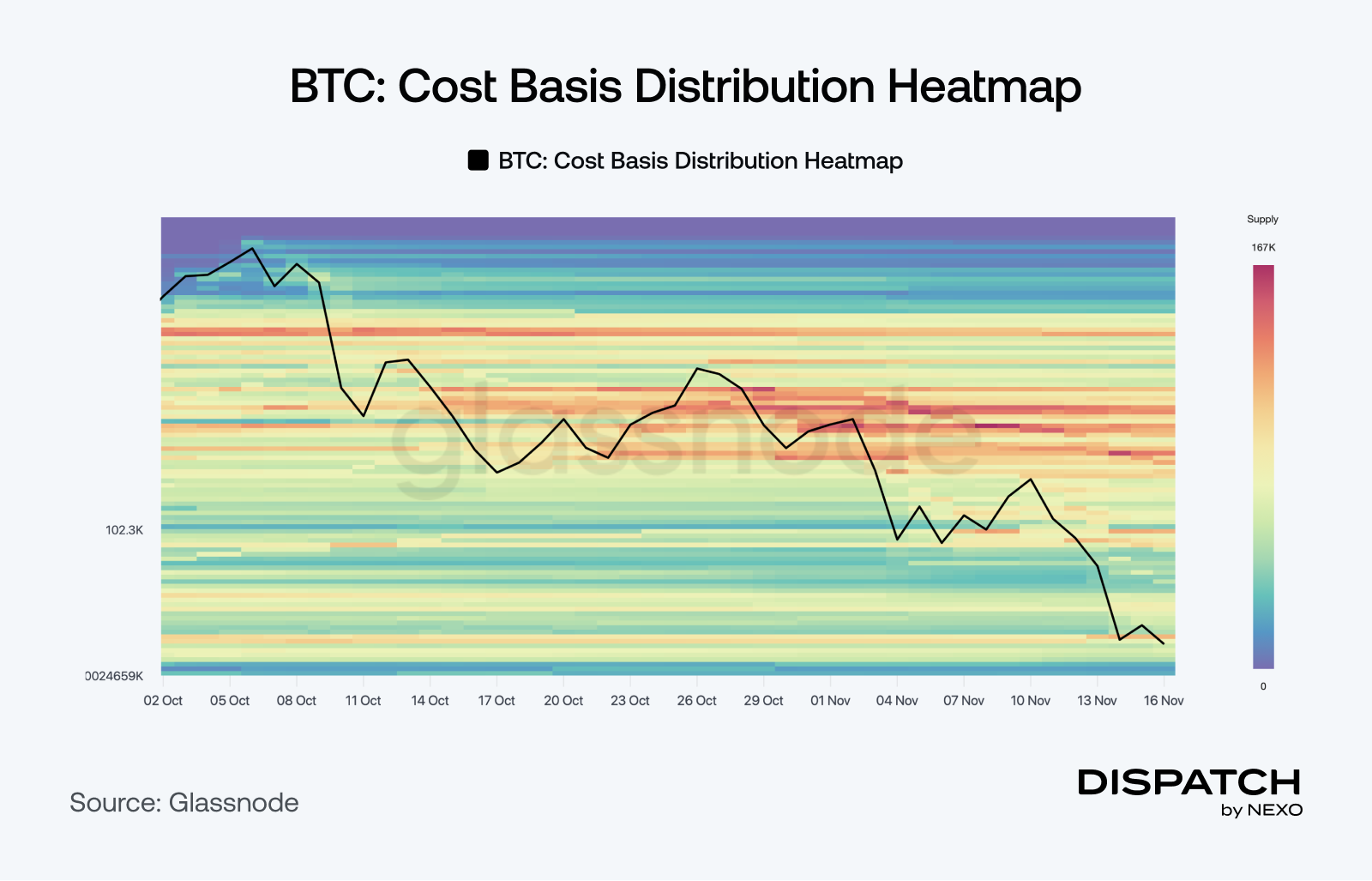

Time for demand-side action

The Cost Basis Distribution Heatmap highlights a notable buildup of realized supply just below $100,000, both ahead of and after the rebound to $106,000. The intensifying activity in this zone points to renewed accumulation, as buyers absorb capitulation flows and establish a firmer base. This balance of seller exhaustion and fresh demand is giving the market room for a measured short-term recovery, even within a broader cautious structure.

Still, a thick supply cluster between $106,000 and $118,000 continues to act as resistance, with many holders using that range to exit near breakeven. Overcoming it will require stronger inflows and sustained conviction to absorb remaining distribution and restore upward momentum.

The numbers

The week’s most interesting numbers

- $25,000 — Peak value of a $10,000 bet on BlackRock’s Bitcoin ETF for a 150% gain in under two years.

- 257% — Harvard’s jump in Bitcoin ETF holdings, making IBIT its top declared investment.

- 89% — XRP’s yearly surge, the only major crypto still in the green.

- $58 million — First-day volume for Canary’s XRP ETF, the biggest ETF debut of 2025.

Hot topic

What the community is discussing

A balanced perspective from Bloomberg.

Is this SOL’s ticket to recovery?

The 4-year cycle makes room for liquidity channels?

Dispatch is a weekly publication by Nexo, designed to help you navigate and take action in the evolving world of digital assets. To share your Dispatch suggestions and comments, email us at [email protected].