अपने Bitcoin के बदले उधार कैसे लें

Mar 16•8 min read

तुरंत जवाब

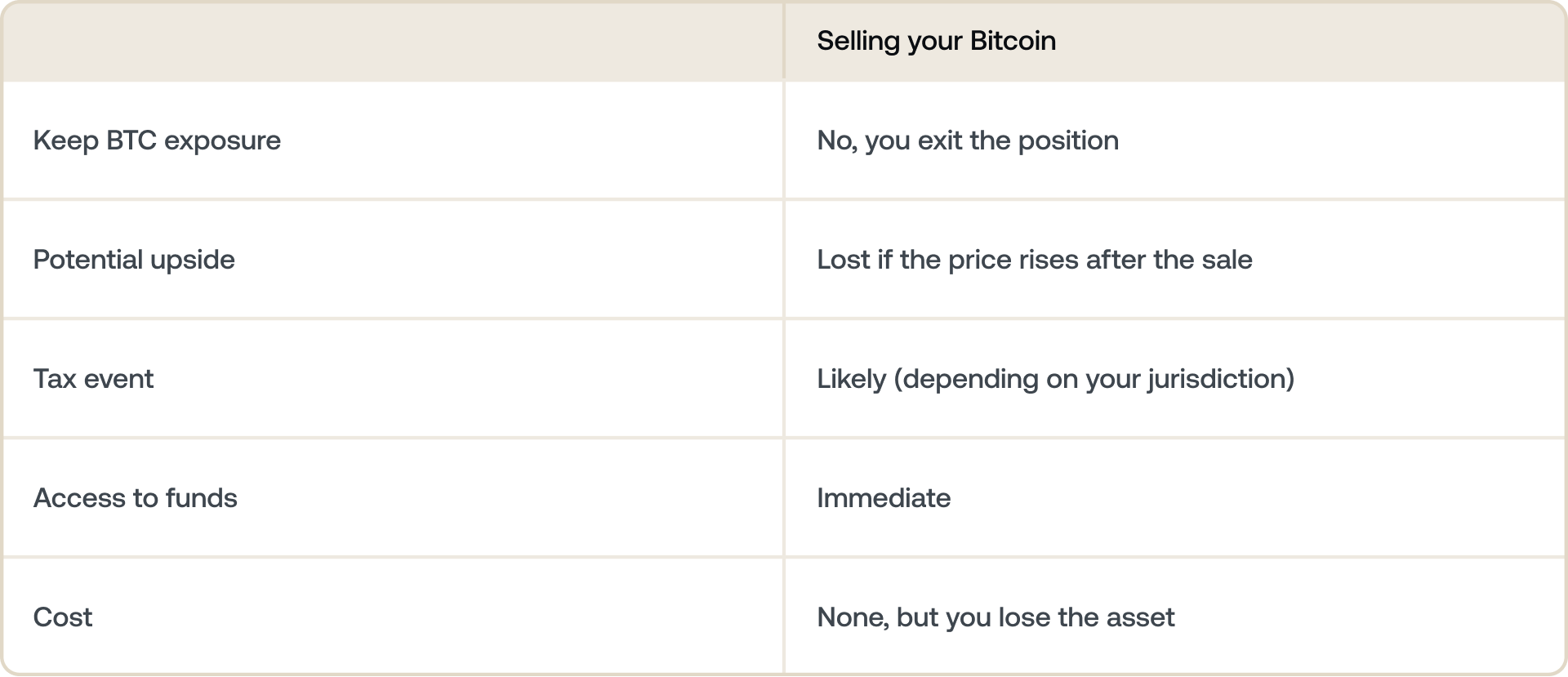

हाँ, आप अपने Bitcoin को बेचे बिना उसके बदले उधार ले सकते हैं। आप एक लेंडिंग प्लेटफ़ॉर्म पर अपने BTC को कोलेटरल के रूप में प्लेज करते हैं और बदले में स्टेबलकॉइन प्राप्त करते हैं। आपका Bitcoin आपके खाते में रहता है - जब तक आप उधार लेते हैं, तब तक यह बस लॉक रहता है। जैसे ही आप इसे चुका देते हैं, यह आपको वापस मिल जाता है। ध्यान रखने वाला प्रमुख नंबर आपका लोन-टू-वैल्यू (LTV) अनुपात है, जो यह निर्धारित करता है कि आप कितना उधार ले सकते हैं और आप कितनी ब्याज दर का भुगतान करते हैं।

किसी खर्च को कवर करने के लिए Bitcoin बेचना एक ऐसे समझौते जैसा लगता है जिसे आप वापस नहीं ले सकते। अगर बेचने के बाद कीमत बढ़ जाती है, तो आप उस बढ़त से चूक गए हैं, और आप कहाँ रहते हैं, इसके आधार पर, आपने कर योग्य घटना को भी शुरू कर दिया हो सकता है।

अपने Bitcoin के बदले उधार लेना दोनों समस्याओं का समाधान करता है। आप आज लिक्विडिटी का एक्सेस पाते हैं और साथ ही अपने BTC को वहीं रखते हैं जहाँ वह है — आपके लिए काम कर रहा है, संभावित रूप से मूल्यवान हो रहा है, और बिक्री को ट्रिगर नहीं कर रहा है।

यह गाइड बताता है कि यह कैसे काम करता है, किन बातों का ध्यान रखना चाहिए, और इसे अपनी सुविधा से ज़्यादा जोखिम लिए बिना कैसे करना है।

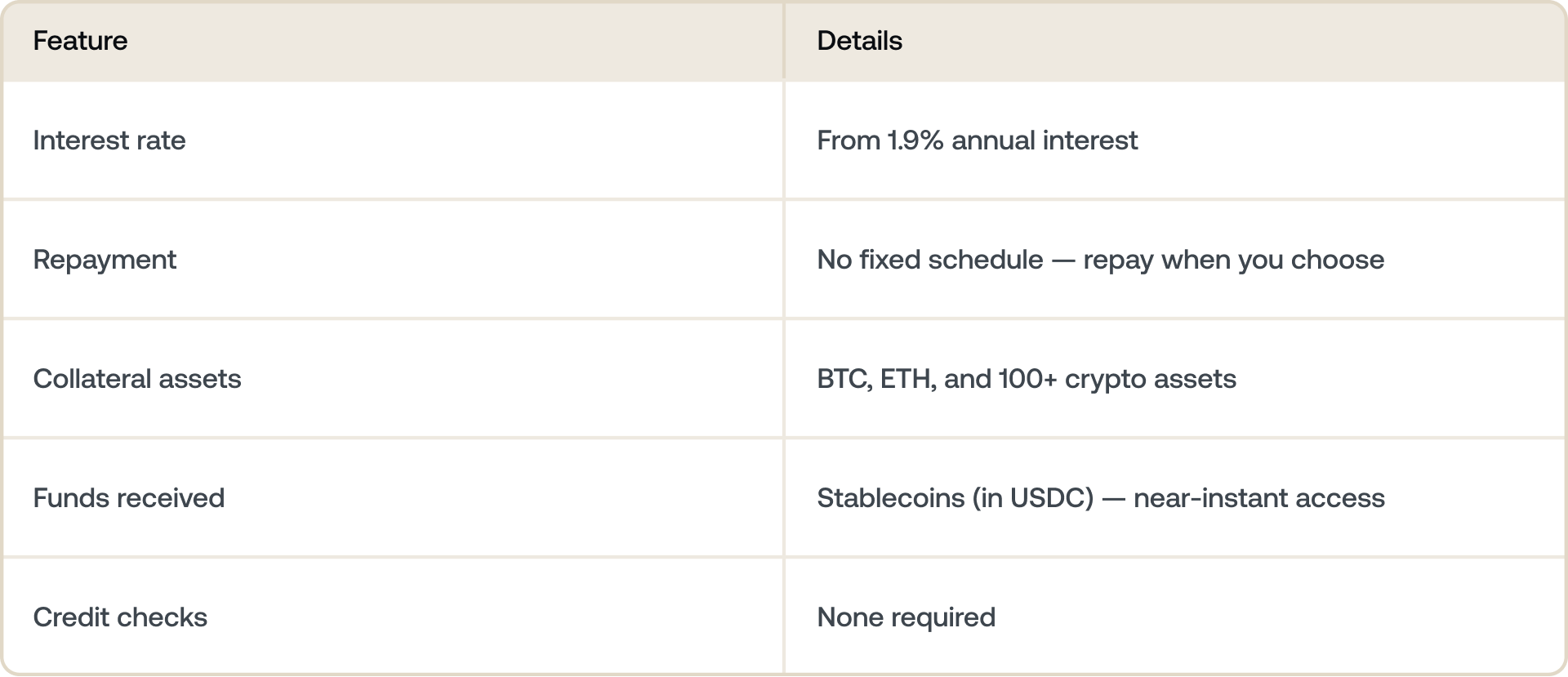

Nexo के क्रिप्टो-समर्थित Credit Line के साथ, आप 1.9% वार्षिक ब्याज से शुरू होने वाली दरों पर Bitcoin और अन्य डिजिटल एसेट के बदले उधार ले सकते हैं — बिना किसी निश्चित रिपेमेंट शेड्यूल और बिना किसी क्रेडिट जाँच के। nexo.com/borrow पर जानें कैसे। दरें आपके LTV और लॉयल्टी टियर पर निर्भर करती हैं।

Bitcoin बेचने के बजाय उसके बदले उधार क्यों लें?

अमीर निवेशक दशकों से रियल एस्टेट, स्टॉक और कला के साथ इस रणनीति का उपयोग कर रहे हैं। किसी ज़रूरत को फ़ंड करने के लिए मूल्यवान एसेट को बेचने के बजाय, वे उसके बदले उधार लेते हैं। एसेट बढ़ता रहता है। लोन समय के साथ चुकाया जाता है।

Bitcoin होल्डर अब वही चीज़ कर सकते हैं।

इसका लेन-देन सीधा है: उधार लेने में पैसे (ब्याज) लगते हैं, लेकिन बेचने से आपको अपने Bitcoin की भविष्य की वृद्धि की कीमत चुकानी पड़ती है। क्या अधिक मायने रखता है यह इस बात पर निर्भर करता है कि BTC किधर जा रहा है और आपको कितनी तत्काल फ़ंड की आवश्यकता है।

Bitcoin के बदले उधार लेना कैसे काम करता है

प्रक्रिया ज़्यादातर लोगों की अपेक्षा से ज़्यादा सरल है। यहाँ बताया गया है कि स्टेप-बाई-स्टेप क्या होता है।

- आप अपने Bitcoin को कोलेटरल के रूप में प्लेज करते हैं। इसका मतलब है Bitcoin खरीदना या उसे प्लेटफ़ॉर्म पर जोड़ना। आपका BTC बेचा नहीं जाता है - इसे लोन के लिए कोलेटरल के रूप में प्लेज किया जाता है।

- आप फ़ंड प्राप्त करते हैं। प्लेटफ़ॉर्म आपको स्टेबलकॉइन देता है — आमतौर पर आपके Bitcoin के वर्तमान मूल्य का 50% तक, जो आपके चुने हुए LTV पर निर्भर करता है।

- आपका BTC आपके नाम पर रहता है। इसे बेचा या कहीं और ट्रांसफ़र नहीं किया जाता है। अगर Bitcoin की कीमत बढ़ती है, तो भी आप उस बढ़ोतरी से लाभ उठाते हैं।

- आप अपनी गति से चुकाते हैं। ज़्यादातर क्रिप्टो लेंडिंग प्लेटफ़ॉर्म एक निश्चित रिपेमेंट शेड्यूल नहीं लगाते हैं। आप जब चाहें, तब चुका सकते हैं — पूरी राशि या आंशिक रूप से।

- आपका Bitcoin अनलॉक हो जाता है। एक बार जब आप लोन और ब्याज चुका देते हैं, तो आपका BTC फिर से पूरी तरह से आपके लिए उपलब्ध हो जाता है।

सबसे महत्वपूर्ण अवधारणा: लोन-टू-वैल्यू (LTV)

LTV क्रिप्टो-समर्थित उधार लेने में एकमात्र सबसे महत्वपूर्ण संख्या है। इसे समझना आपके लिए आवश्यक है।

LTV आपके द्वारा उधार ली गई राशि और आपके कोलेटरल के मूल्य का अनुपात है। अगर आप $10,000 मूल्य के Bitcoin को प्लेज करते हैं और $5,000 उधार लेते हैं, तो आपका LTV 50% है।

जब Bitcoin की कीमत गिरती है तो क्या होता है

यह वह हिस्सा है जो लोगों को चौंका देता है। आपका LTV निश्चित नहीं है — यह मार्केट के साथ बदलता है।

उदाहरण: आप $100,000 मूल्य का 1 BTC प्लेज करते हैं और $50,000 उधार लेते हैं — 50% LTV। अगर Bitcoin $70,000 पर गिर जाता है, तो आपका LTV 71.4% ($50,000 / $70,000) तक बढ़ जाता है। अगर लिक्विडेशन थ्रेसहोल्ड 75% है, तो अब आप अपने कोलेटरल को स्वचालित रूप से बेचे जाने के करीब हैं। हमेशा सावधानी से उधार लें और जब मार्केट अस्थिर हो तो अपने LTV की निगरानी करें।

अगर Bitcoin का मूल्य गिरता है, तो आपके लोन का समर्थन करने वाला कोलेटरल कम हो जाता है। आपका LTV स्वचालित रूप से बढ़ जाता है, भले ही आपने अतिरिक्त फ़ंड उधार न लिया हो। अगर यह किसी प्लेटफ़ॉर्म की लिक्विडेशन थ्रेसहोल्ड को पार कर जाता है, तो प्लेटफ़ॉर्म LTV को वापस नीचे लाने के लिए आपके कुछ Bitcoin बेच सकता है।

सुरक्षित कैसे रहें

- कम LTV से शुरू करें — 30% से नीचे आपको कीमत में उतार-चढ़ाव के खिलाफ एक बड़ा बफर देता है।

- अगर कीमत में काफी गिरावट आती है तो कोलेटरल के रूप में जोड़ने के लिए अतिरिक्त BTC तैयार रखें।

- अपने Bitcoin के लिए मूल्य अलर्ट सेट करें ताकि आप असावधान न रह जाएँ।

- केवल वही उधार लें जिसे आप कीमत में उतार-चढ़ाव से स्वतंत्र होकर आराम से चुका सकें।

Nexo पर Bitcoin के बदले उधार कैसे लें

Nexo का क्रिप्टो-समर्थित Credit Line आपको Bitcoin और 100 से अधिक अन्य एसेट के बदले उधार लेने की सुविधा देता है। यहाँ बताया गया है कि व्यवहार में अनुभव कैसा दिखता है।

आपके द्वारा भुगतान की जाने वाली ब्याज दर आपके लॉयल्टी टियर और आपके LTV पर निर्भर करती है। Nexo के क्लाइंट जो 20% या उससे कम का LTV बनाए रखते हैं, वे 1.9% पर वार्षिक ब्याज का एक्सेस पा सकते हैं। मौजूदा दरें देखें और गणना करें कि आप nexo.com/borrow पर कितना उधार ले सकते हैं

लोग असल में क्रिप्टो-समर्थित ऋण का इस्तेमाल किस लिए करते हैं

Bitcoin के बदले उधार लेना सिर्फ एक टैक्स रणनीति नहीं है। लोग इसका उपयोग कई तरह की व्यावहारिक ज़रूरतों के लिए करते हैं।

- बिना बेचे खर्चों को कवर करना: घर का नवीनीकरण, ट्यूशन, स्वास्थ्य सेवा — उच्च लागतें जो अन्यथा असुविधाजनक समय पर बिक्री के लिए मजबूर कर सकती हैं।

- अस्थिरता के दौरान नकदी प्रवाह का प्रबंधन: अगर मार्केट गिरता है और आप नुकसान पर बेचना नहीं चाहते हैं, तो एक अल्पकालिक लोन आपको स्थितियों में सुधार की प्रतीक्षा करते हुए तत्काल जरूरतों को पूरा करने की सुविधा देता है।

- फ़ंडिंग के अवसर: लंबी अवधि के क्रिप्टो पोज़िशन को लिक्विडेट किए बिना एक नए बिज़नेस, संपत्ति या एसेट में निवेश करना।

- BTC एक्सपोजर को बरकरार रखना: कई लंबी अवधि के होल्डर ठीक इसी वजह से बेचने से हिचकिचाते हैं क्योंकि वे निरंतर मूल्यवृद्धि की उम्मीद करते हैं। एक लोन उन्हें उस क्षमता को छोड़े बिना मूल्य का एक्सेस करने देता है।

अक्सर पूछे जाने वाले प्रश्न

1. क्या आप Bitcoin के बदले उधार ले सकते हैं?

हाँ. आप अपने Bitcoin को एक लेंडिंग प्लेटफ़ॉर्म पर कोलेटरल के रूप में प्लेज करते हैं और बदले में नकद या स्टेबलकॉइन प्राप्त करते हैं। आपका BTC बेचा नहीं जाता है — यह आपका बना रहता है और लोन चुकाने के बाद अनलॉक हो जाता है।

2. आप Bitcoin के बदले कितना उधार ले सकते हैं?

यह प्लेटफ़ॉर्म और आपके चुने हुए LTV पर निर्भर करता है। ज़्यादातर प्लेटफ़ॉर्म आपको अपने Bitcoin के वर्तमान मूल्य का 50% तक उधार लेने की अनुमति देते हैं। कम उधार लेना — कम LTV पर — अगर Bitcoin की कीमत गिरती है तो आपको एक बड़ा सुरक्षा बफर देता है, और आमतौर पर आपको क्रिप्टो-समर्थित ऋण पर कम ब्याज दर देता है।

3. Bitcoin लोन में LTV क्या है?

LTV का मतलब है लोन-टू-वैल्यू। यह आपके लोन राशि और आपके कोलेटरल के मूल्य का अनुपात है। अगर आप $10,000 के Bitcoin के बदले $4,000 उधार लेते हैं, तो आपका LTV 40% है। आपका LTV Bitcoin की कीमत के साथ बदलता है — अगर कीमत गिरती है, तो आपका LTV बढ़ जाता है, भले ही आपने लोन में कोई बदलाव न किया हो।

4. अगर मेरे लोन के दौरान Bitcoin गिर जाता है तो क्या होगा?

जैसे-जैसे आपके कोलेटरल का मूल्य कम होता है, आपका LTV स्वचालित रूप से बढ़ जाता है। अगर यह प्लेटफ़ॉर्म की लिक्विडेशन थ्रेसहोल्ड को पार कर जाता है, तो प्लेटफ़ॉर्म LTV को स्वीकार्य सीमा के भीतर वापस लाने के लिए आपके कुछ Bitcoin बेच सकता है। इसका समाधान है कि सावधानी से उधार लें — कम LTV से शुरू करने से आपको लिक्विडेशन को ट्रिगर किए बिना कीमत में गिरावट को झेलने की गुंजाइश मिलती है।

5. क्या आप Bitcoin के बदले उधार लेने पर टैक्स देते हैं?

अधिकांश अधिकार क्षेत्रों में, Bitcoin के बदले उधार लेना एक कर योग्य घटना नहीं है क्योंकि आप अपना BTC बेच या उसका निपटान नहीं कर रहे हैं। लोन अपने आप में आय नहीं है। कहा जा रहा है कि, कर उपचार देश और व्यक्तिगत परिस्थितियों के अनुसार अलग-अलग होता है — अपनी स्थिति के लिए विशिष्ट सलाह के लिए एक योग्य कर पेशेवर से परामर्श करें।

6. क्या Bitcoin के बदले उधार लेना सुरक्षित है?

यह हो सकता है, अगर आप सावधानी से उधार लें और संस्थागत-ग्रेड कस्टडी वाले प्लेटफ़ॉर्म का उपयोग करें। अगर Bitcoin की कीमत काफी नीचे और काफी तेजी से गिरती है, तो आपका कोलेटरल बिना किसी चेतावनी के बेचा जा सकता है। कम LTV रखने और अस्थिर अवधि के दौरान अपने पोज़िशन की निगरानी करने से वह जोखिम काफी कम हो जाता है।

7. Bitcoin लोन और क्रिप्टो credit line के बीच क्या अंतर है?

'credit line' शब्द का अर्थ आमतौर पर एक सतत सुविधा है जहाँ आप ज़रूरत के अनुसार फ़ंड निकालते हैं और लचीले ढंग से चुकाते हैं, बजाय इसके कि आप एकमुश्त राशि लें। अधिकांश क्रिप्टो-नेटिव प्लेटफ़ॉर्म एक निश्चित-अवधि के लोन के बजाय एक credit line मॉडल प्रदान करते हैं।

यह सामग्री दुनिया भर में उपलब्ध है, और इस जानकारी की उपलब्धता वर्णित सेवाओं तक पहुँच का गठन नहीं करती है, जो सेवाएँ कुछ अधिकार क्षेत्रों में उपलब्ध नहीं हो सकती हैं। ये सामग्रियां केवल सामान्य सूचना उद्देश्यों के लिए हैं और इन्हें वित्तीय, कानूनी, कर, या निवेश सलाह, किसी भी Nexo सेवा का उपयोग करने के लिए प्रस्ताव, आग्रह, सिफारिश, या समर्थन के रूप में नहीं माना जाना चाहिए और ये पर्सनलाइज़्ड नहीं हैं, या किसी भी तरह से विशेष निवेश उद्देश्यों, वित्तीय स्थिति या जरूरतों को दर्शाने के लिए तैयार नहीं की गई हैं। डिजिटल एसेट उच्च स्तर के जोखिम के अधीन हैं, जिसमें अस्थिर मार्केट मूल्य गतिशीलता, नियामक परिवर्तन और तकनीकी प्रगति शामिल है, लेकिन यह इन्हीं तक सीमित नहीं है। डिजिटल एसेट का पिछला प्रदर्शन भविष्य के परिणामों का एक विश्वसनीय संकेतक नहीं है। डिजिटल एसेट पैसा या कानूनी निविदा नहीं हैं, सरकार या किसी केंद्रीय बैंक द्वारा समर्थित नहीं हैं, और अधिकांश के पास कोई अंतर्निहित एसेट, राजस्व स्ट्रीम या मूल्य का अन्य स्रोत नहीं है। पर्सनल परिस्थितियों के आधार पर स्वतंत्र निर्णय का उपयोग किया जाना चाहिए, और कोई भी निर्णय लेने से पहले एक योग्य पेशेवर से परामर्श की सिफ़ारिश की जाती है।