Nexo vs Salt Lending: сравнение кредитов, обеспеченных криптовалютой

May 04•7 min read

Брать кредит под залог криптовалюты вместо её продажи стало распространённой стратегией среди инвесторов, которые хотят получить ликвидность, не закрывая свою позицию. Две платформы, предлагающие это уже долгие годы, — Nexo и Salt Lending. Несмотря на схожую идею в основе, они работают совершенно по-разному.

Salt — одно из старейших имён в сфере крипто-кредитования: компания основана в 2016 году и специализируется на займах с фиксированным сроком. Nexo предлагает возобновляемую кредитную линию в рамках широкой продуктовой экосистемы. Условия займа, стоимость и последствия рыночных колебаний — всё это определяется структурными различиями между платформами.

Этот сравнительный обзор разбирает ключевые факторы, чтобы вы могли выбрать наиболее подходящий вариант кредитования.

Для краткого обзора функций и актуальных ставок посетите нашу страницу сравнения Nexo и Salt Lending.

Обзор Nexo и Salt Lending

О двух платформах

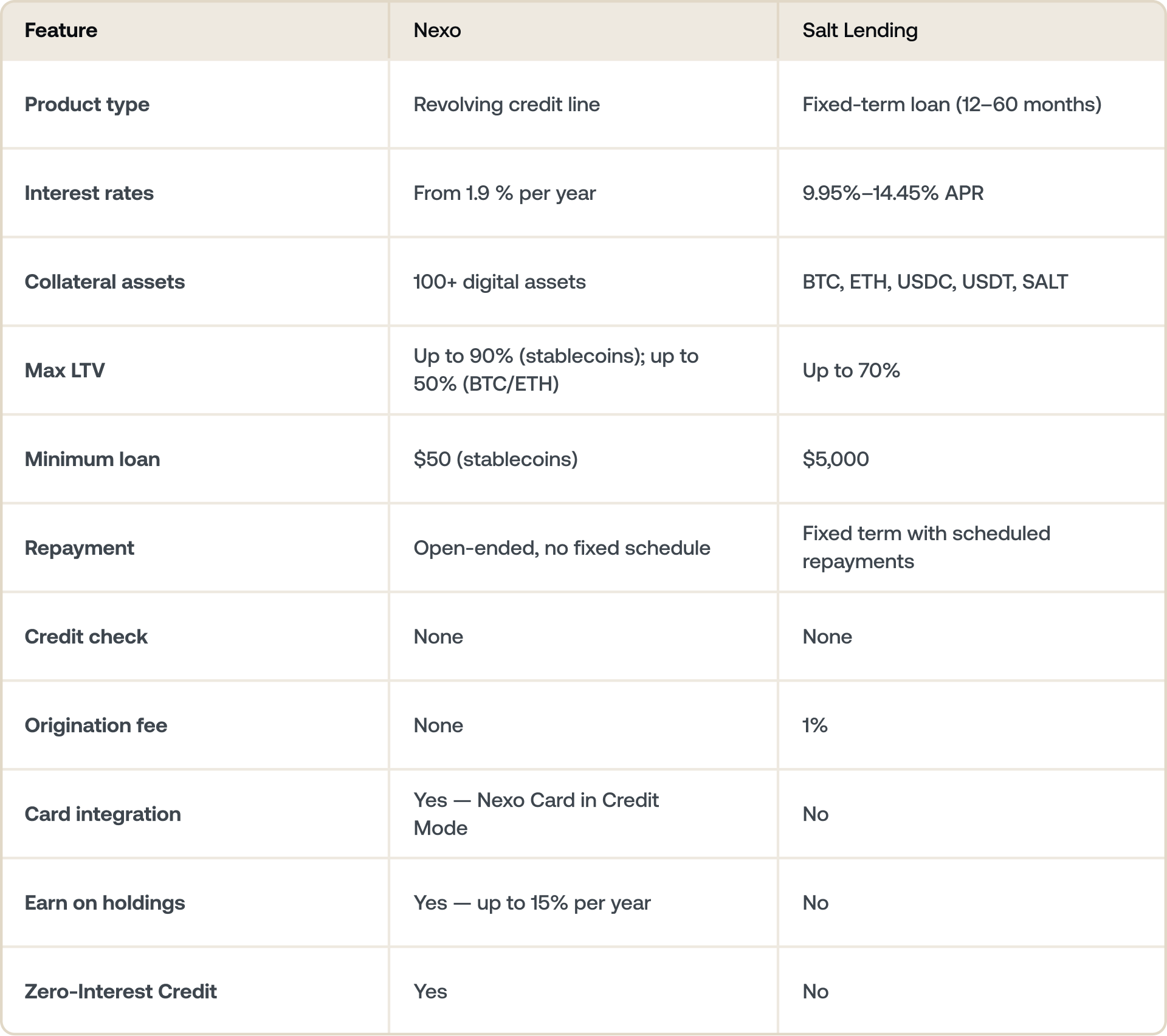

Nexo запустила свою платформу в 2018 году как сервис кредитования и заработка на криптоактивах. Сегодня платформа объединяет кредитование, сбережения, расходы по карте и обмен в одном аккаунте. Кредитный продукт работает как возобновляемая кредитная линия — вы снимаете средства по мере необходимости и погашаете долг в удобном темпе.

Salt Lending была основана в 2016 году. Компания предлагает займы для частных лиц и бизнеса под обеспечение криптовалютой, с фиксированными сроками погашения от 12 до 60 месяцев. Salt работает преимущественно в США и ограниченном числе других рынков.

Как работают займы

Это наиболее важное структурное различие между двумя платформами.

Nexo использует возобновляемую кредитную линию. Здесь нет срока займа и фиксированного графика погашения. Берите кредит на нужную сумму и погашайте его в удобное время.

Salt Lending использует займы с фиксированным сроком. При оформлении займа в Salt вы выбираете срок от 12 до 60 месяцев, получаете единовременную выплату и погашаете долг по фиксированному графику. Такая структура подходит заемщикам, которым важна предсказуемость — фиксированная сумма погашения и четкая дата окончания. Она менее удобна для тех, кто хочет гибко снимать средства и погашать долг в собственном ритме.

Ни один из форматов не является универсально лучшим. Правильный выбор зависит от цели займа и предпочтительного способа управления погашением.

Почему заемщики выбирают Nexo

В отличие от займов с фиксированным сроком, Credit Line от Nexo работает на возобновляемой основе без фиксированного графика погашения. Заемщики вправе погасить задолженность в любое время, а доступный кредит восстанавливается по мере погашения — при соблюдении применимых требований к соотношению займа к стоимости (LTV).

Nexo также предлагает Zero-Interest Credit — отдельный продукт, позволяющий взять кредит под залог BTC или ETH под 0% без комиссий, с фиксированным сроком и без риска ликвидации на протяжении этого срока. Каждая позиция включает заранее определенные параметры защиты цены, поэтому возможные исходы прозрачны с самого начала. У Salt аналогичного продукта нет.

Процентные ставки

Ставки Nexo определяются уровнем в программе лояльности ( Loyalty Tier) и рассчитываются ежедневно исходя из доли NEXO Tokens, которую вы держите относительно общей стоимости портфеля:

- Base: менее 1% портфеля в NEXO Tokens

- Silver: 1–5% портфеля в NEXO Tokens

- Gold: 5–10% портфеля в NEXO Tokens

- Platinum: не менее 10% портфеля в NEXO Tokens, при LTV ≤ 20% — ставки от 1.9% в год

Ставки Salt определяются соотношением кредита к залогу:

- 30% LTV: 9,95% годовых

- 50% LTV: 10,95% годовых

- 70% LTV: 14,45% годовых

Ставки Salt фиксируются на весь срок кредита с момента его начала. Ставки Nexo могут меняться при изменении уровня в программе лояльности.

Почему заемщики выбирают Nexo

Структура ставок Nexo выгодна для заемщиков, готовых оптимизировать свой портфель — в частности, держа часть средств в NEXO Tokens. Для таких заемщиков потенциальная экономия по сравнению с фиксированными ставками Salt весьма значительна, особенно при длительных периодах заимствования.

Обеспечение и LTV

Nexo принимает в качестве обеспечения более 100 цифровых активов, включая Bitcoin, Ethereum, стейблкойны и широкий спектр альткойнов. Лимиты LTV зависят от актива:

- Стейблкойны: до 90% LTV

- BTC и ETH: до 50% LTV

- Другие активы: по-разному (актуальные лимиты — на nexo.com/borrow)

Salt принимает Bitcoin, Ethereum, USDC, USDT и собственный токен SALT. Максимальный LTV — 70%, вне зависимости от актива. Ограниченный список обеспечения означает, что Salt не подойдет, если ваши активы преимущественно представлены альткойнами.

Более высокий LTV позволяет взять больше под то же обеспечение — но это также означает, что ваша позиция ближе к маржин-коллу при падении цен. Обе платформы ликвидируют обеспечение, если LTV превышает пороговое значение поддержки.

Почему заемщики выбирают Nexo

Гибкость обеспечения в Nexo означает, что на вас может работать весь ваш портфель, а не только несколько активов. Если вы держите диверсифицированный набор активов — BTC, ETH, стейблкойны и альткойны — Nexo позволяет заложить их вместе, оптимизировать LTV по типам активов и корректировать состав по мере движения рынка. Более узкий список обеспечения Salt и единый максимальный LTV оставляют большинству диверсифицированных портфелей меньше возможностей.

Расходы по кредитной линии

Интеграция Nexo Card

Карта Nexo Card напрямую интегрирована с кредитной линией Nexo через Credit Mode. Каждая покупка по карте автоматически списывается с кредитной линии — это значит, что вы можете занимать под криптовалюту прямо в момент покупки, везде, где принимается Mastercard. Покупки в Credit Mode также приносят до 2% кэшбека в криптовалюте.

Это делает кредитную линию Nexo полноценным инструментом для повседневных трат, а не только механизмом для крупных разовых выводов средств.

Расходы Salt Lending

Salt не предлагает карту и не интегрирован ни с какими торговыми терминалами. Заемные средства выплачиваются наличными или стейблкойнами, которые затем нужно перевести на банковский счет или внешнюю платформу для использования. Платформа сфокусирована исключительно на выдаче и погашении кредитов.

Почему заемщики выбирают Nexo

Для заемщиков, которые хотят использовать кредитную линию как инструмент для повседневных трат, Nexo — единственный вариант из двух. Возможность занимать в момент покупки и получать кэшбек по этим транзакциям добавляет практичное, повседневное измерение, которого у продукта Salt просто нет.

Доход на ваши активы

Доходность Nexo

Активы, хранящиеся на Nexo, могут приносить процентный доход через Flexible Savings или Fixed-term Savings. Flexible Savings обеспечивает ежедневные выплаты с капитализацией без периода блокировки. Fixed-term Savings предлагает более высокие ставки на сроки до 12 месяцев. Ставки достигают до 15% в год — в зависимости от актива, уровня в программе лояльности и предпочтений по выплатам.

Это означает, что заимствование и получение дохода в Nexo могут работать параллельно. Активы, которые вы держите, но не закладываете в качестве обеспечения, могут генерировать доходность, пока другая часть обеспечивает вашу кредитную линию.

Доходность Salt Lending

Salt не предлагает никаких продуктов для начисления процентов. Активы, хранящиеся на платформе, активно используются для обеспечения кредита. Незадействованные активы просто простаивают.

Почему заемщики выбирают Nexo

В Nexo активы за пределами залоговой позиции могут приносить до 15% в год в фоновом режиме — это измерение доходности, которого Salt попросту не предлагает.

Что лучше подходит вам

Выбирайте Nexo, если:

- Вам нужна гибкость — возможность брать и погашать по собственному графику без фиксированного срока

- Вы держите широкий спектр активов и хотите использовать их в качестве обеспечения

- Вы хотите объединить заимствование, сбережения и расходы в одном аккаунте

- Вам нужен доступ к более низким ставкам через уровни программы лояльности

- Вы хотите финансирование под 0% через Zero-Interest Credit

- Вы хотите получать доходность на активы в процессе заимствования

Выбирайте Salt Lending, если:

- Вам нужен фиксированный график погашения с четкой датой окончания

- Вы преимущественно держите Bitcoin или Ethereum и не нуждаетесь в широкой поддержке обеспечения

- Вы хотите простой срочный кредитный продукт без интегрированной экосистемы

Итог

Salt Lending и Nexo оба позволяют занимать под криптовалюту без её продажи — но они ориентированы на разные стили заимствования. Salt построен на фиксированных сроках и предсказуемых выплатах. Nexo создан для постоянного гибкого доступа к ликвидности с более широкой продуктовой экосистемой вокруг.

Ставки Salt начинаются около 10% годовых; ставки Nexo значительно ниже для пользователей, держащих NEXO tokens.

Сравните Nexo и Salt Lending — актуальные ставки и детали продуктов.

Часто задаваемые вопросы

1. Что такое Salt Lending?

Salt Lending — американская платформа крипто-кредитования, основанная в 2016 году. Она предлагает срочные кредиты для физических и юридических лиц под обеспечение криптовалютой без проверки кредитной истории.

2. Как Nexo сравнивается с Salt Lending по процентным ставкам?

Ставки Nexo начинаются от 1.9% в год для пользователей высших уровней программы лояльности. Ставки Salt Lending варьируются от 9,95% до 14,45% годовых в зависимости от соотношения кредита к залогу.

3. Требует ли Salt Lending проверки кредитной истории?

Нет. Как и Nexo, Salt Lending использует вашу криптовалюту в качестве обеспечения для получения кредита, поэтому кредитная история не требуется.

4. Какое обеспечение принимает Salt Lending?

Salt принимает Bitcoin (BTC), Ethereum (ETH), USDC, USDT и собственный токен SALT. Nexo принимает более 100 цифровых активов, которые можно комбинировать.

5. Доступен ли Nexo в США?

Да. Nexo возобновил работу в США в феврале 2026 года через партнерство с Bakkt, публично торгуемой криптовалютной компанией, в рамках соответствующей регуляторной структуры.

6. Могу ли я тратить средства напрямую с кредитной линии Nexo?

Да. Nexo Card в Credit Mode позволяет занимать под вашу криптовалюту прямо в момент покупки — везде, где принимается Mastercard. Salt Lending не предлагает карту и никакой интеграции для прямых трат.

7. Могу ли я получать процентный доход на криптовалюту, занимая в Nexo?

Да. Активы на учетной записи Nexo, не заложенные в качестве обеспечения, могут приносить процентный доход через Flexible или Fixed-term Savings — до 15% в год в зависимости от актива и уровня в программе лояльности. Salt Lending не предлагает продуктов для получения дохода.

8. Что такое Zero-Interest Credit от Nexo?

Zero-Interest Credit — самостоятельный продукт Nexo, позволяющий занимать под BTC, ETH, SOL и XRP под 0% и без комиссий, без риска ликвидации в течение фиксированного срока. Каждая позиция включает заранее определенные параметры защиты цены, поэтому результаты видны с самого начала. У Salt Lending нет аналогичного продукта.

Данные материалы доступны по всему миру. Наличие этой информации не означает доступ к описанным услугам, которые могут быть недоступны в отдельных юрисдикциях. Эти материалы носят исключительно общий информационный характер и не являются финансовой, юридической, налоговой или инвестиционной консультацией, предложением, призывом, рекомендацией или одобрением использовать какие‑либо услуги Nexo, не являются персональными и никоим образом не учитывают конкретные инвестиционные цели, финансовое положение или потребности. Цифровые активы сопряжены с высоким уровнем риска, в том числе связанным с волатильностью рыночных цен, изменениями в регулировании и техническим прогрессом. Прошлые результаты цифровых активов не являются надежным индикатором будущих результатов. Цифровые активы не являются деньгами или законным платежным средством, не обеспечены государством или центральным банком, и у большинства из них нет базовых активов, источника дохода или иных источников стоимости. Следует руководствоваться собственным суждением с учетом личных обстоятельств. Перед принятием любых решений рекомендуется проконсультироваться с квалифицированным специалистом.

Заимствование под цифровые активы сопряжено с риском. При снижении стоимости обеспечения от вас может потребоваться оперативно пополнить обеспечение или погасить кредит. Платформа может выполнить частичное или полное автоматическое погашение либо реализовать обеспечение для управления пороговыми значениями LTV, в том числе в периоды быстро меняющегося рынка, когда уведомления могут не поступить вовремя.