Markets Today - May 29, 2026

May 29•3 min read

Daily analysis of crypto markets and the forces shaping them, from the Nexo research desk.

Bitcoin steadies near $74,000 as ceasefire hopes build and labour market week looms

The crypto market has recovered from yesterday's lows, with the total market cap edging back to $2.47 trillion as a tentative 60-day ceasefire extension between the U.S. and Iran — pending President Trump's final approval, sends oil toward its worst monthly decline since March 2020 and pushes global equities to fresh record highs. Bitcoin is steadying near $73,700, Ethereum has reclaimed $2,000, and altcoins are posting modest bounces. Yet the broader divergence remains intact: the S&P 500 closed at a record 7,563, Brent crude has slipped below $93, and gold is recovering toward $4,533 — while crypto has yet to meaningfully participate in the macro relief trade. The near-term focus is shifting from geopolitical developments to regulatory ones.

Bitcoin

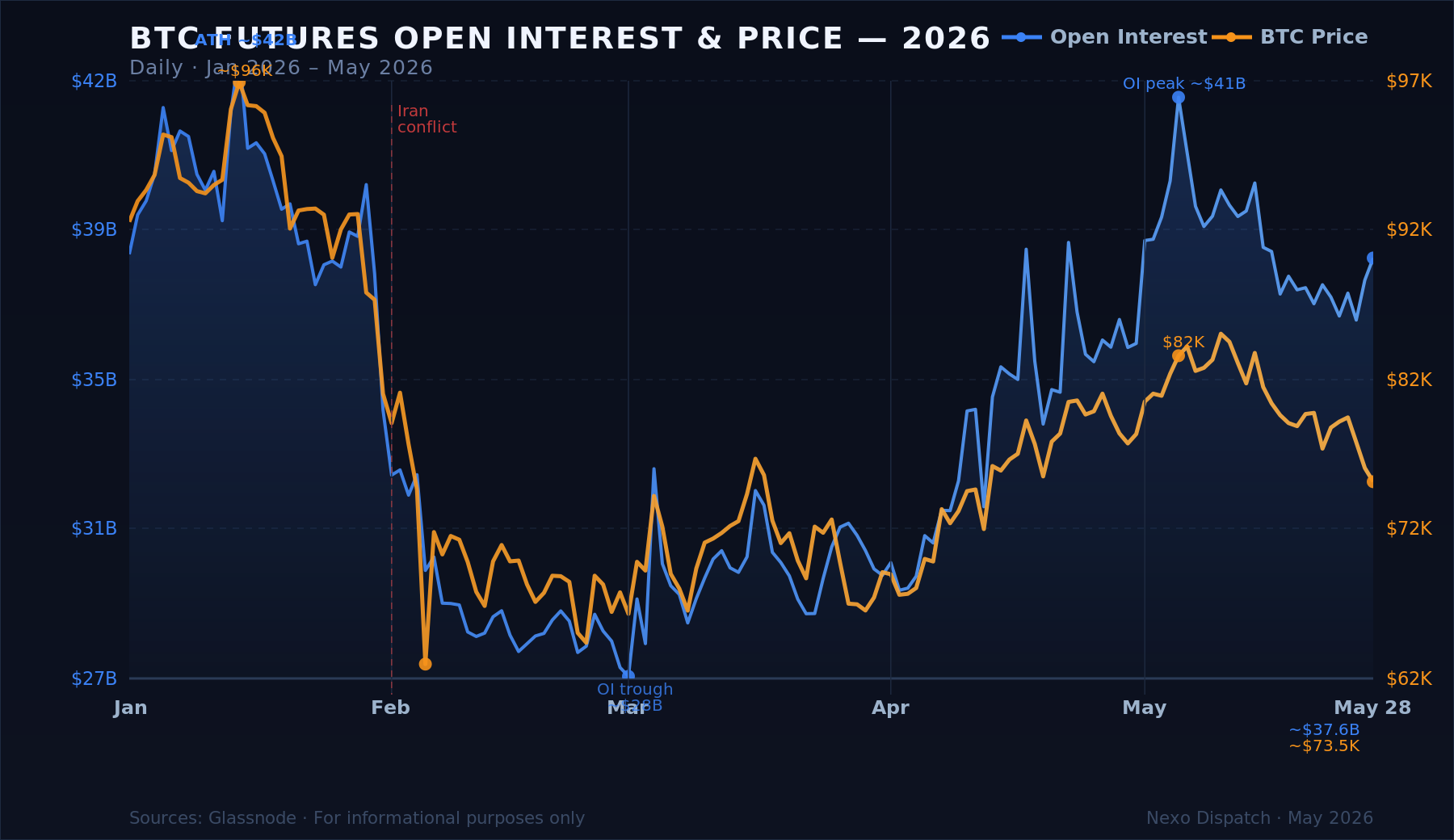

Bitcoin is trading around $73,700, recovering modestly from Thursday's low near $72,500, though the weekly picture remains under pressure. The ceasefire extension provided limited lift for crypto — the market had already moved to price in diplomatic progress, and when Bitcoin held rather than broke higher on the confirmation, the momentum faded. What the chart reflects is a market that has been consolidating since October, with price action increasingly compressed as implied volatility sits at its lowest since September. The options market shows building demand for downside protection, but the broader read is of a market in a holding pattern — waiting for a structural catalyst rather than reacting to macro headlines.

Institutional investors are looking past geopolitical headlines toward U.S. crypto market structure legislation. Bitcoin open interest has held above $35 billion and is trending toward $40 billion per Glassnode — suggesting that while ETF demand has softened, derivatives positioning is quietly rebuilding, a dynamic that could amplify the next directional move in either direction.

Ethereum & Altcoins

Ethereum is just above $2,000, recovering 1.6% on the day after Thursday's dip to $1,965, but down 6.4% on the week. XRP climbed 2.3% to $1.32, Solana and Polygon each rose 1%, and Cardano advanced 2.6% — Friday's modest bounce sitting against a week of meaningful losses across the complex. The standout performer of the week is Stellar's XLM, up 25% in 24 hours after DTCC announced plans to connect its tokenized securities platform to the network — a real-world institutional adoption signal worth noting as the broader market waits for regulatory clarity.

Macro & Institutional

The tentative 60-day ceasefire extension, which would include unrestricted Hormuz shipping, the lifting of the U.S. naval blockade, and an Iranian commitment not to pursue a nuclear weapon, still requires President Trump's approval and Iranian confirmation. Even if confirmed, the deal would not immediately normalise oil flows: Hormuz traffic remains well below pre-conflict levels and the market is more inventory-depleted than before the conflict began.

Thursday's PCE data provided a moderately constructive backdrop. Headline PCE came in at 3.8% year-on-year — the fastest pace since May 2023, but core PCE rose just 0.2% month-on-month, a deceleration that slightly pushes back against the most hawkish rate expectations.

Anthropic raised $65 billion in Series H funding at a post-money valuation of $965 billion, with run-rate revenue crossing $47 billion. SpaceX is targeting a $1.8 trillion IPO valuation with roadshows potentially beginning as soon as June 4. Both signal that the AI infrastructure buildout is accelerating regardless of the macro environment — a dynamic that continues to underpin markets.

Looking Ahead

Next week's calendar is front-loaded with labour market and activity data that will shape the Fed's June calculus. Monday brings Fed Chair Powell speaking alongside Eurozone unemployment and the first May manufacturing readings — S&P Global PMI and ISM Manufacturing, both expected to show continued expansion. Tuesday delivers JOLTS job openings, Wednesday ADP employment. Friday's nonfarm payrolls are the week's centrepiece. For Bitcoin, the question heading into June is whether progress on the CLARITY Act can provide the structural catalyst that macro relief has so far failed to deliver.

Author: Iliya Kalchev, Analyst at Nexo’s Dispatch

This material is produced by Nexo for informational purposes only and does not constitute financial, investment, legal, or tax advice, or a recommendation to transact in any digital asset. Views are the author's as of the date of publication and may change without notice. Information is from sources believed reliable, but Nexo makes no warranty as to its accuracy and accepts no liability for any loss arising from reliance on this material.