How Bitcoin-backed loans work in 2026

Oct 28, 2025•9 min read

Quick answer

Yes, you can borrow against Bitcoin without selling it. You pledge your BTC as collateral with a lending platform and receive cash or stablecoins in return. Your Bitcoin stays in your account — it's just locked while you borrow. You get it back once you repay. The key number to watch is your Loan-to-Value (LTV) ratio, which determines how much you can borrow and what interest rate you pay.

A Bitcoin-backed loan lets you borrow cash or stablecoins without selling your Bitcoin.

You keep exposure to BTC’s future upside while unlocking liquidity for real-world goals — whether that’s buying a house, funding a business, or covering life’s bigger expenses.

It’s the modern equivalent of what wealthy investors have done for decades: borrowing against assets like stocks or real estate, which they believe will keep appreciating.

Why do some investors borrow instead of selling?

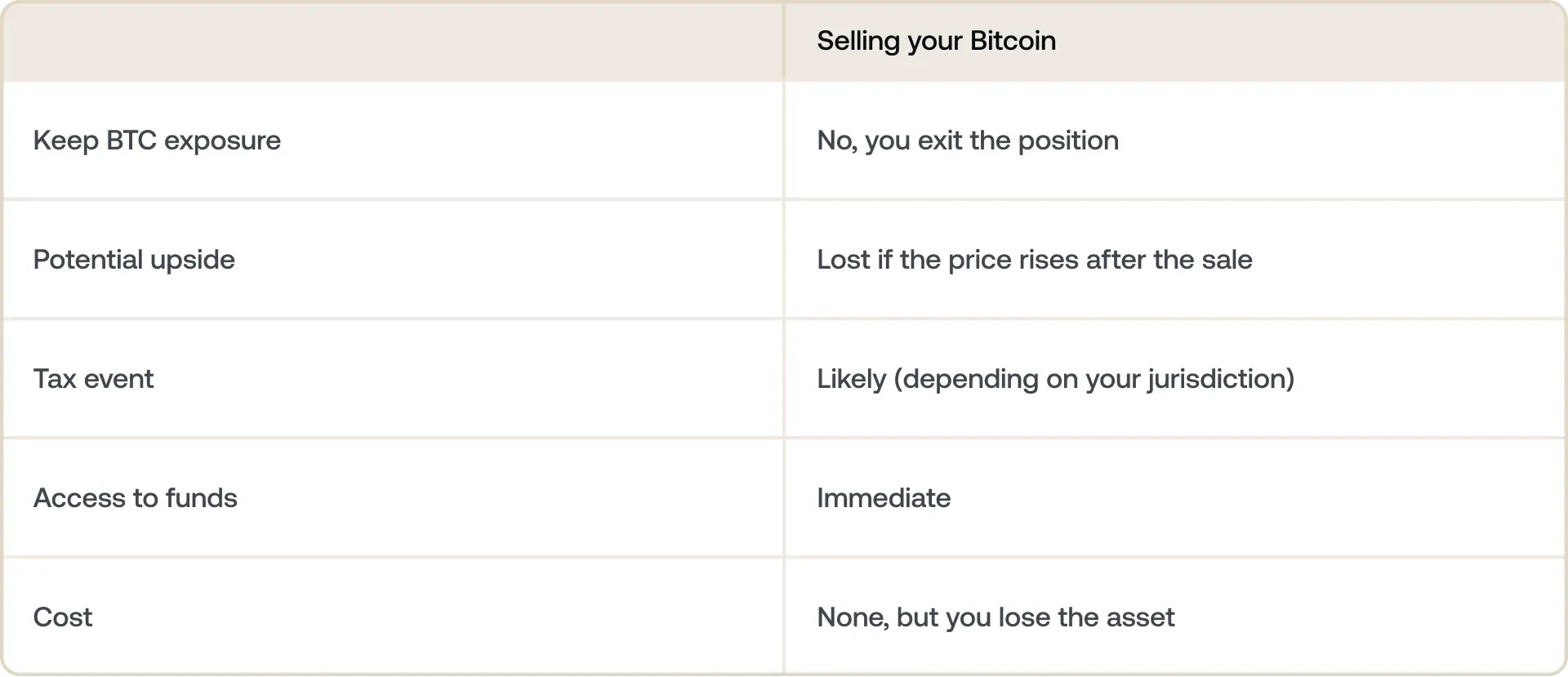

Selling Bitcoin can feel like selling your future. Once it’s gone, you’ve locked in gains and potentially a tax bill while losing out on any further appreciation.

Borrowing against it, on the other hand, means you can:

- Access cash without triggering a sale or taxable event.

- Keep your BTC working toward potential long-term growth.

- Manage liquidity during volatile markets.

The trade-off is straightforward: borrowing costs money (interest), but selling costs you the future growth of your Bitcoin. Which matters more depends on your view of where BTC is heading and how urgently you need the funds.

That’s the logic driving a growing group of investors in 2026 — people who see their Bitcoin not as something to spend, but as something to leverage.

How does a Bitcoin-backed loan actually work?

You pledge Bitcoin as collateral. Your BTC is locked (not sold) and used to back the loan.

You receive funds. Depending on the platform, that can be in fiat or stablecoins, often within minutes.

You keep the upside. While locked, you still benefit if the Bitcoin price rises.

You repay flexibly. Once you’ve paid back the loan and interest, your BTC is available once again.

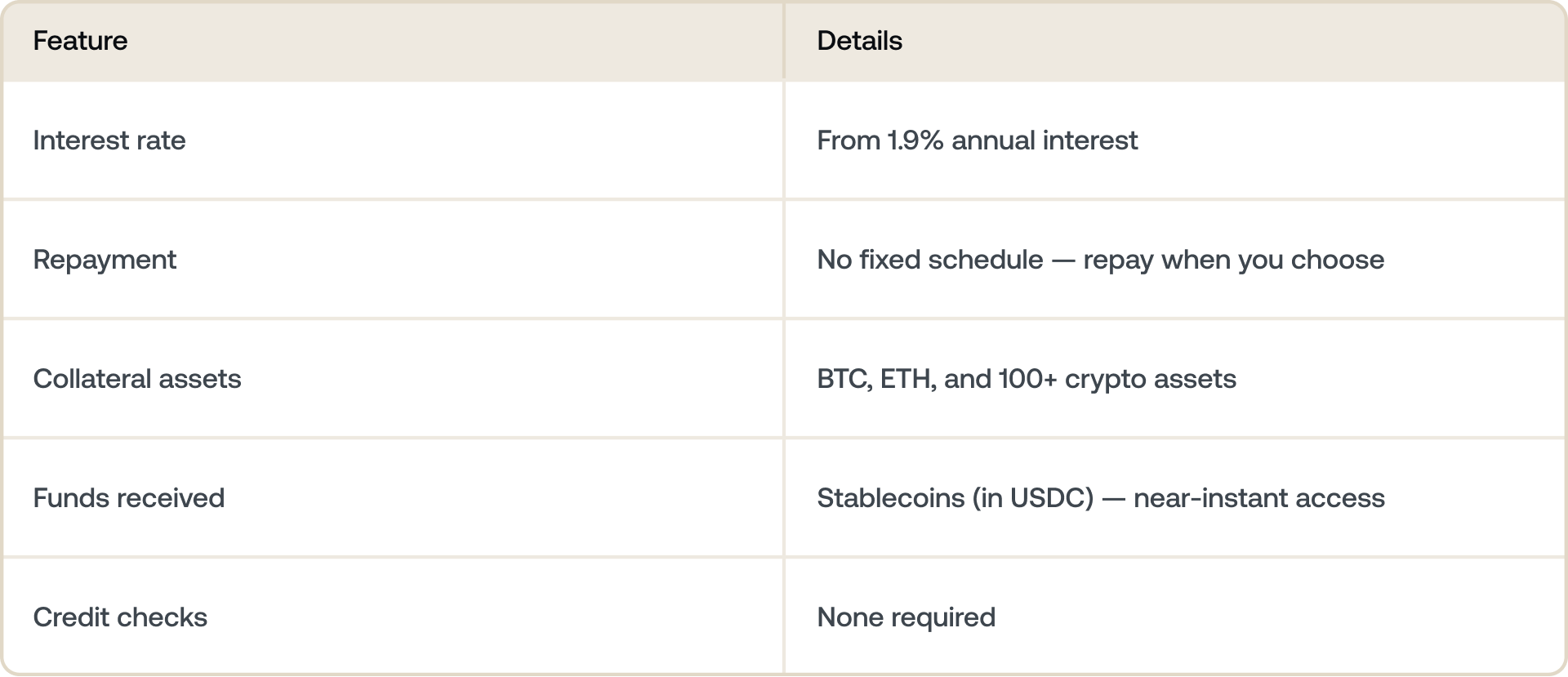

Platforms like Nexo position this around key parameters:

- Loan-to-Value (LTV): The ratio of what you borrow vs. what your BTC is worth. Lower LTV means lower risk.

- Interest rates from 0.9%, depending on your Wealth Tier and collateral ratio.

- No fixed repayment schedule, meaning you repay at your own pace, in crypto or stablecoins.

- Multi-asset collateral flexibility, letting you combine Bitcoin with other supported assets such as Ethereum or stablecoins to back your loan.

Many platforms, including Nexo, give you a choice: you can withdraw your Bitcoin-backed loan in either fiat or stablecoins — digital assets that are pegged 1:1 to major fiat currencies like USD, EUR, or GBP.

If you choose fiat, the process is seamless and fast. You can withdraw the funds straight to your bank account, with automatic, real-time conversions handled directly on the platform.

If you choose stablecoins, you have two clear paths depending on what you need:

1. You want to use the funds in the real world

If your goal is to pay for something tangible — a property deposit, a renovation, or business funding — you can:

- Swap stablecoins for fiat directly on the platform or via an exchange.

- Then withdraw to your linked bank account.

Because stablecoins like USDC are pegged to the dollar, the conversion is straightforward — one USDC is designed to equal roughly one U.S. dollar. It’s a digital bridge between your Bitcoin holdings and your bank account.

2. You want to keep the funds in the crypto ecosystem

If your plan isn’t to spend right away, you can use your stablecoins within the platform to grow or diversify your portfolio:

- Swap into other cryptocurrencies you believe in (for example, converting USDC into ETH, BTC, or SOL).

- Reinvest strategically, as many users use their borrowed stablecoins to take new positions or to dollar-cost average into other assets.

This is what makes borrowing in stablecoins flexible: they move seamlessly between digital and traditional finance.

Already holding stablecoins instead of BTC? You can also run this in reverse — see our guide to how USDC loans work.

The real-world use case: buying a home with Bitcoin.

Imagine this: You own 5 BTC, each worth $100,000.

Instead of selling them to fund a property deposit, you use them as collateral for a Bitcoin-backed loan. The property becomes yours, while your Bitcoin remains in play, ready to benefit if prices rise.

That’s not theoretical. In 2026, a growing number of people are doing exactly this. Some even finance entire home purchases using Bitcoin collateral — a concept once seen as outlandish and now becoming increasingly common.

It’s a sentiment many long-term holders share.

How much can you actually borrow?

When you borrow against Bitcoin, the loan amount you can unlock depends on something called your Loan-to-Value ratio, or LTV.

LTV measures the size of your loan compared to the value of your Bitcoin collateral. It’s shown as a percentage.

For example, if you use $200,000 worth of BTC to borrow $100,000, your LTV is 50%. That means your loan is worth half the value of your Bitcoin holdings.

For Bitcoin, most platforms, including Nexo, set the highest LTV at around 50%. This buffer exists because Bitcoin’s price can move fast. By lending you only up to half of your asset’s value, the platform helps protect both sides:

- You’re less likely to face a margin call if BTC dips.

- The lender can manage risk without selling your collateral too soon.

Lowering your LTV (say, to 20–30%) gives you even more protection against volatility and often qualifies you for better interest rates.

What happens if your LTV rises?

If the price of Bitcoin drops, your LTV rises automatically because your collateral is worth less.

Example: You pledge 1 BTC worth $100,000 and borrow $50,000 — a 50% LTV. If Bitcoin drops to $70,000, your LTV jumps to 71.4% ($50,000 / $70,000). If the liquidation threshold is 75%, you're now close to having your collateral automatically sold. Always borrow conservatively and monitor your LTV when the market is volatile.

If it crosses a certain threshold (often around 70–83% depending on the platform), you’ll receive a margin call, which is a reminder to:

- Add more collateral (more BTC or other assets), or

- Repay part of the loan to restore balance.

If no action is taken, part of your Bitcoin may be automatically sold to bring your LTV back to a safer zone.

How to stay safe

- Start with a low LTV — below 30% gives you a large buffer against price swings.

- Keep extra BTC ready to add as collateral if the price drops significantly.

- Set price alerts for your Bitcoin so you're not caught off guard.

- Only borrow what you can repay comfortably, independent of price movements.

When it works and when it doesn’t.

Bitcoin loans work best when:

- You have a strong long-term conviction in BTC.

- You only borrow what you can comfortably repay.

- You monitor your LTV during volatility.

It can go wrong if:

- The Bitcoin price drops sharply, and your collateral is automatically used to repay the loan.

- You don’t act on margin call notifications.

- You treat a crypto loan like “free money.”

Still weighing the decision? Read our take on whether borrowing against Bitcoin is a good idea.

Why are people turning to crypto loans?

People use Bitcoin-backed loans for different reasons:

- Real estate purchases to unlock deposits or refinance traditional mortgages.

- Business growth to fund ventures without selling long-term holdings.

- Tax management to access liquidity without triggering taxable events.

- Diversification to use BTC value while staying invested.

In essence, it’s about turning digital wealth into usable liquidity.

What makes it different from a traditional loan?

A Bitcoin-backed loan isn’t the same as a bank loan. You’re borrowing against your digital assets, not your credit history or income.

Traditional loans:

- Based on income, credit score

- Takes weeks to process

- Monthly repayment schedule

Bitcoin-backed loan

- Based on the value of your BTC

- Same-day approval

- Flexible repayment at your pace

- Bitcoin as collateral

Important: If the BTC price drops too far, the lender may sell part of your Bitcoin to restore balance, but your property or other assets remain untouched.

Frequently asked questions

1. Can you borrow against Bitcoin?

Yes. You pledge your Bitcoin as collateral with a lending platform and receive cash or stablecoins in return. Your BTC isn't sold — it remains yours and is unlocked once you repay the loan.

2. Do you actually borrow Bitcoin, or something else?

You don't borrow Bitcoin itself. Your BTC serves as collateral, and what you receive is cash or stablecoins. Your Bitcoin stays locked in your account until the loan is repaid, then becomes fully available again.

3. How much can you borrow against Bitcoin?

It depends on the platform and your chosen LTV. Most platforms allow you to borrow up to 50% of your Bitcoin's current value. Borrowing less — at a lower LTV — gives you a larger safety buffer if Bitcoin's price drops, and typically gives you a lower interest rate on the crypto-backed loan.

4. What is LTV in a Bitcoin loan?

LTV stands for Loan-to-Value. It's the ratio of your loan amount to the value of your collateral. If you borrow $4,000 against $10,000 of Bitcoin, your LTV is 40%. Your LTV moves with Bitcoin's price — if the price drops, your LTV rises, even if you haven't changed the loan.

5. What happens if Bitcoin drops while I have a loan?

Your LTV increases automatically as your collateral loses value. If it crosses the platform's liquidation threshold, the platform may sell some of your Bitcoin to bring LTV back within acceptable limits. The solution is to borrow conservatively — starting at a low LTV gives you room to absorb price drops without triggering liquidation.

6. Do you pay tax when borrowing against Bitcoin?

In most jurisdictions, borrowing against Bitcoin is not a taxable event because you're not selling or disposing of your BTC. The loan itself isn't income. That said, tax treatment varies by country and individual circumstances — consult a qualified tax professional for advice specific to your situation.

7. Is borrowing against Bitcoin safe?

It can be, if you borrow conservatively and use a platform with institutional-grade custody. If Bitcoin's price drops far enough and fast enough, your collateral can be sold without warning. Keeping a low LTV and monitoring your position during volatile periods significantly reduces that risk.

8. What's the difference between a Bitcoin loan and a crypto credit line?

The term "credit line" typically implies an ongoing facility where you draw down funds as needed and repay flexibly, rather than taking a single lump sum. Most crypto-native platforms offer a credit line model rather than a fixed-term loan.

These materials are accessible globally, and the availability of this information does not constitute access to the services described, which services may not be available in certain jurisdictions. Rates are subject to change and may vary by region, loyalty tier, and other applicable factors. Always refer to the Nexo app for your applicable rates. These materials are for general information purposes only and not intended as financial, legal, tax, or investment advice, offer, solicitation, recommendation, or endorsement to use any of the Nexo Services and are not personalized, or in any way tailored to reflect particular investment objectives, financial situation, or needs. Digital assets are subject to a high degree of risk, including but not limited to volatile market price dynamics, regulatory changes, and technological advancements. The past performance of digital assets is not a reliable indicator of future results. Digital assets are not money or legal tender, are not backed by the government or by a central bank, and most do not have any underlying assets, revenue stream, or other source of value. Independent judgment based on personal circumstances should be exercised, and consultation with a qualified professional is recommended before making any decision.