Markets Today - May 11, 2026

May 11•4 min read

Daily analysis of crypto markets and the forces shaping them, from the Nexo research desk.

BTC keeps steady above $80,000 ahead of US CPI

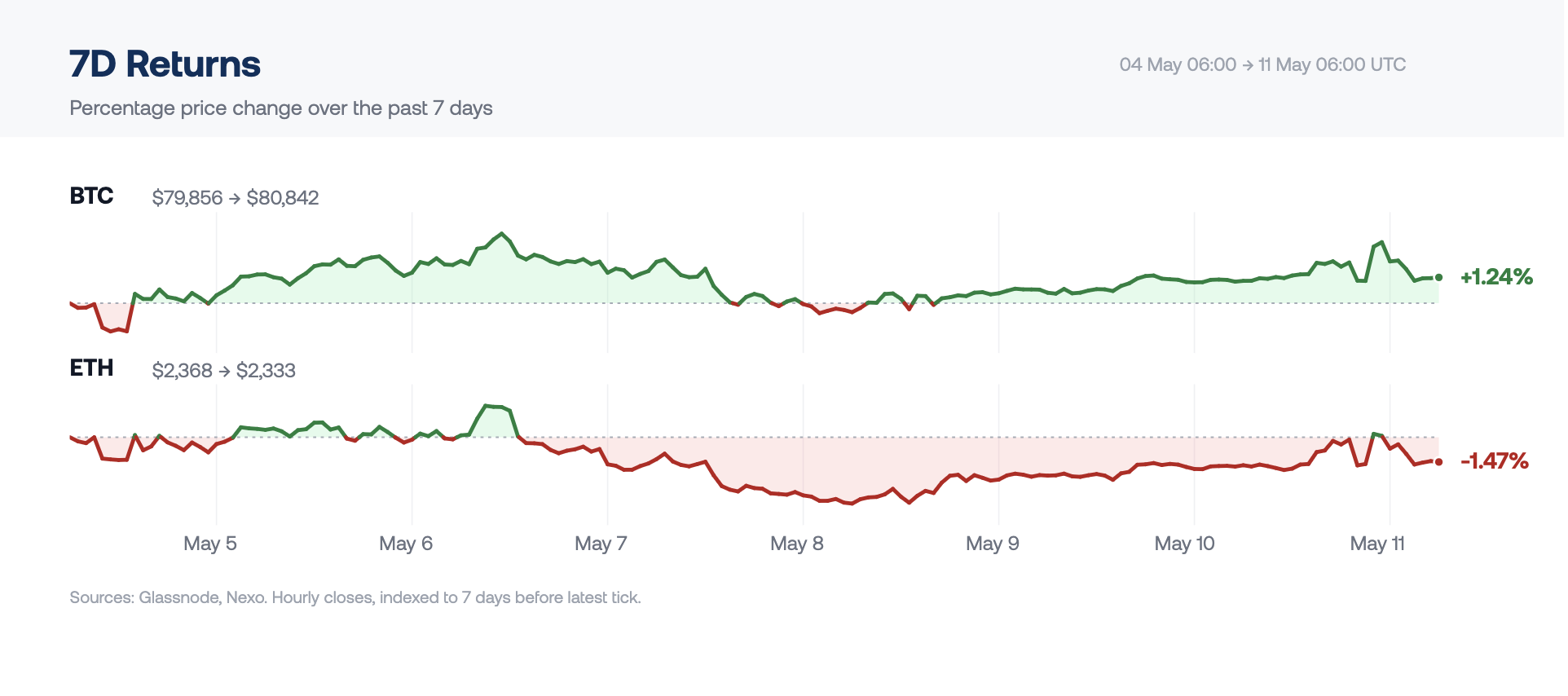

Digital assets open the week steady, though moves beneath the surface . Bitcoin trades above $80,000 with a total crypto market cap around $2.65 trillion but the two majors pull apart into Tuesday's US CPI print: BTC spot accumulation has continued and last week's run of daily ETF outflows broke, while net spot selling in Ether has intensified into early May. In traditional markets, the S&P 500 and Nasdaq closed Friday at fresh records, a sixth consecutive weekly gain for both. WTI finished near $95 and Brent near $101, both down on the week as a fragile U.S.-Iran ceasefire absorbed renewed Persian Gulf exchanges. The 10-year Treasury closed at 4.38%. This week’s focus is the April CPI print Tuesday and the expected full Senate vote on Kevin Warsh's confirmation as Federal Reserve Chair.

Bitcoin

Bitcoin opens Monday above $80,000, flat over 24 hours. Spot Bitcoin ETFs took in +$623 million last week, the sixth straight positive week and +$3.40 billion across the streak, even with daily flows turning negative on May 7 (−$277.5 million) and May 8 (−$145.7 million).

The spot story extends on-chain. Glassnode data shows BTC leaving exchanges every day for the past 30 days, averaging −48,700 BTC per reading, with net spot buying outpacing selling by +7,400 BTC over the month. Derivatives are pulling the other way: perpetual open interest at $36.1 billion sits 45% below the October peak, leverage is thin, and funding averaged −2.95% annualized over the past month before turning slightly positive on May 10–11. The setup has the signature of post-capitulation accumulation: steady spot buying, coins leaving exchanges, derivatives still positioned short. With leverage thin and funding only just turning, the most likely break is higher if spot demand holds and shorts cover.

Ethereum & Altcoins

Ether trades around $2,300 on Monday morning, also flat over the past 24 hours. ETH ETF flows, though, have decoupled from Bitcoin: 2026 YTD flows sit at −$240 million against +$2.73 billion for spot Bitcoin ETFs, and cumulative net inflows have drawn down roughly 18% from the October peak versus 5.5% for Bitcoin. The trend suggests capital has been flowing selectively into Bitcoin, bypassing Ether.

Glassnode data shows ETH cumulative spot volume delta around −450,000 ETH over 30 days –sustained net selling – the inverse of Bitcoin. Derivatives, however, are starting to shift. The cross-venue 8-hour mean funding rate has flipped cleanly positive over the last four days, and open interest has fallen 6% over the same window, from $23.2 billion to $21.8 billion – the signature of shorts unwinding rather than new longs entering. The combination potentially explains ETH's price resilience despite the spot selling and suggests that derivatives short cover has been the marginal bid.

Macro & Institutional

Both S&P 500 and Nasdaq closed Friday at records, registering a sixth consecutive weekly gain, the longest win streak since 2024. April nonfarm payrolls printed +115,000 against consensus near 60,000–65,000, with average hourly earnings +0.2% month-over-month, robust enough to keep the hawkish Fed case alive and raise the stakes for Tuesday's CPI.

Yields remain elevated but stable. The 10-year closed at 4.38% and the 2-year at 3.90%, not yet at levels that pressure equities. WTI finished near $95 and Brent near $101, down roughly 7% and 6% on the week. Both eased as the U.S.-Iran ceasefire absorbed fresh Strait of Hormuz exchanges, though prices remain historically high. The IEA estimates the conflict is still removing around 14 million barrels per day from global supply. Stable yields, easing oil, and equities at records make for a constructive setup for risk. Tuesday's CPI is the test.

Looking Ahead

Two pivot points land on the same week. Powell's eight-year term as Federal Reserve Chair ends May 15 as the Senate is expected to vote on Warsh's confirmation. Warsh’s pledged intent to retire forward guidance and the dot plot is a shift in how the Fed communicates, not just how it sets rates.It arrives alongside the most important inflation print of the cycle. The April CPI release Tuesday is the key test of whether the oil shock has bled into broader prices. An in-line core reading keeps the energy-only story intact and Fed expectations roughly where they are. An upside surprise in core inflation — particularly driven by services and shelter rather than energy — would push bond yields higher and weigh on risk assets. Either way, Warsh inherits the chair the same week the answer arrives.

Author: Dessislava Ianeva, Analyst at Nexo’s Dispatch

This material is produced by Nexo for informational purposes only and does not constitute financial, investment, legal, or tax advice, or a recommendation to transact in any digital asset. Views are the author's as of the date of publication and may change without notice. Information is from sources believed reliable, but Nexo makes no warranty as to its accuracy and accepts no liability for any loss arising from reliance on this material.