USDC কী?

Mar 13•7 min read

সংক্ষিপ্ত উত্তর

USDC হল একটি স্ট্যাবলকয়েন — এক ধরনের ক্রিপ্টোকারেন্সি যার মূল্য সর্বদা $1। এটি Circle দ্বারা ইস্যু করা হয় এবং এটি 1:1 অনুপাতে মার্কিন ডলার নগদ এবং নিয়ন্ত্রিত মার্কিন আর্থিক প্রতিষ্ঠানে রাখা স্বল্পমেয়াদী ইউএস ট্রেজারি সিকিউরিটি দ্বারা সমর্থিত। Bitcoin বা Ethereum-এর মতো, USDC-এর মূল্য বাড়ে বা কমে না। এই স্থিতিশীলতাই এটিকে ক্রিপ্টো অস্থিরতার ঝুঁকি ছাড়াই পেমেন্ট, সঞ্চয় এবং সুদ আয় করার জন্য উপযোগী করে তোলে।

বেশিরভাগ মানুষ যখন দামের ওঠানামা ছাড়াই ক্রিপ্টোতে থাকতে চান তখন USDC সম্পর্কে জানতে পারেন। কিন্তু এটি কেবল ক্রিপ্টোর একটি "নিরাপদ" সংস্করণ হওয়ার চেয়েও বেশি কিছু।

ডিজিটাল অর্থনীতিতে USDC সবচেয়ে বহুল ব্যবহৃত অ্যাসেটগুলোর মধ্যে একটি — এবং যে হোল্ডাররা এটি দিয়ে কী করতে হবে তা জানেন, তারা এটি অলসভাবে বসিয়ে রেখেও উল্লেখযোগ্য পরিমাণে সুদ আয় করতে পারেন। এই আর্টিকেলটি ব্যাখ্যা করে USDC কী, এটি কীভাবে কাজ করে, এটি নিরাপদ কিনা এবং এটিকে কীভাবে কাজে লাগানো যায়।

Nexo, USDC-এর উপর প্রতিযোগিতামূলক সুদের রেট অফার করে — আপনি ফ্লেক্সিবল অ্যাক্সেসের মাধ্যমে আপনার ব্যালেন্সের উপর প্রতিদিন আয় করতে পারেন অথবা Fixed-term Savings-এর মাধ্যমে উচ্চতর রেট লক করতে পারেন। USDC আয় সম্পর্কে জানুন এখানে → https://nexo.com/earn-crypto/usdc

USDC কীভাবে কাজ করে

USDC হল USD Coin-এর সংক্ষিপ্ত রূপ। এটি একটি স্ট্যাবলকয়েন যা মার্কিন-ভিত্তিক আর্থিক প্রযুক্তি কোম্পানি Circle দ্বারা ইস্যু করা হয়। প্রচলনে থাকা প্রতিটি USDC, নিয়ন্ত্রিত মার্কিন আর্থিক প্রতিষ্ঠানে রিজার্ভ হিসেবে রাখা প্রকৃত মার্কিন ডলার বা স্বল্প-মেয়াদী ইউএস ট্রেজারি বিল দ্বারা সমর্থিত।

এর কার্যপদ্ধতি বেশ সহজ। যখন কেউ USDC কেনেন, Circle সমতুল্য ডলার গ্রহণ করে এবং নতুন USDC টোকেন মিন্ট করে। যখন কেউ ডলারের জন্য USDC রিডিম করেন, তখন Circle সেই টোকেনগুলো বার্ন করে এবং মূল নগদ ছেড়ে দেয়। সরবরাহ সর্বদা রিজার্ভের সাথে মিলে যায়, যা দাম $1-এ রাখে।

USDC একাধিক ব্লকচেইনে চলে — যার মধ্যে রয়েছে Ethereum, Solana, Base, Arbitrum, Avalanche এবং আরও অনেক — যার অর্থ হল আপনার প্রয়োজনের উপর নির্ভর করে এটি বিভিন্ন নেটওয়ার্কে চলাচল করতে পারে।

USDC-কে কী সমর্থন করে

Circle একটি প্রধান অ্যাকাউন্টিং ফার্ম দ্বারা নিরীক্ষিত মাসিক প্রত্যয়ন প্রতিবেদন প্রকাশ করে যা রিজার্ভগুলো নিশ্চিত করে। 2026 সালের প্রথম দিক পর্যন্ত, রিজার্ভটি রাখা আছে:

- নিয়ন্ত্রিত মার্কিন ব্যাংকে রাখা নগদ

- Circle রিজার্ভ ফান্ডের মাধ্যমে স্বল্প-মেয়াদী ইউএস ট্রেজারি সিকিউরিটি

এটি USDC-কে মার্কেটের সবচেয়ে স্বচ্ছ স্ট্যাবলকয়েনগুলোর মধ্যে একটি করে তুলেছে। রিজার্ভগুলো ক্রিপ্টো, লেন্ডিং বুক বা অন্যান্য অস্থিতিশীল অ্যাসেটে বিনিয়োগ করা হয় না — যা কিছু অন্যান্য স্ট্যাবলকয়েন থেকে একটি অর্থপূর্ণ পার্থক্য।

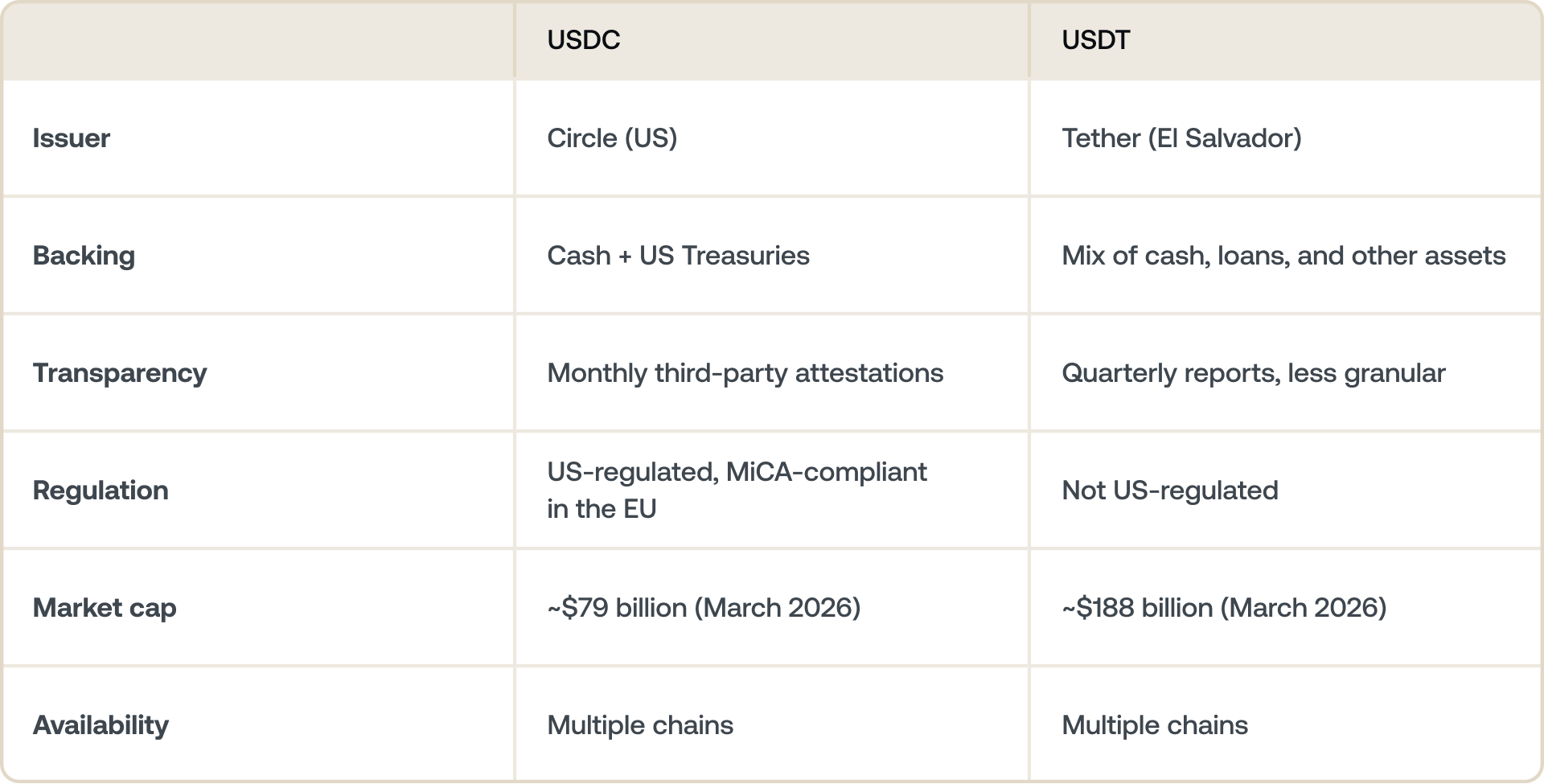

USDC বনাম USDT: পার্থক্য কী?

USDT (Tether) এবং USDC দুটি প্রধান স্ট্যাবলকয়েন, কিন্তু তারা কীভাবে কাজ করে এবং কারা সেগুলি ইস্যু করে সে বিষয়ে তারা অর্থপূর্ণভাবে ভিন্ন।

বাস্তবে, উভয়ই $1-এ ট্রেড করে এবং বেশিরভাগ এক্সচেঞ্জ এবং DeFi প্রোটোকল জুড়ে গৃহীত হয়। এর মার্কিন নিয়ন্ত্রক সমর্থন এবং রিজার্ভ স্বচ্ছতার কারণে প্রাতিষ্ঠানিক ব্যবহারকারী এবং নিয়ন্ত্রিত প্ল্যাটফর্মগুলো সাধারণত USDC পছন্দ করে।

ঐতিহাসিকভাবে, আগে থেকে গ্রহণ এবং নির্দিষ্ট কিছু এক্সচেঞ্জে গভীর তারল্যের কারণে USDT-এর মার্কেটের একটি বড় অংশ ছিল।

USDC কি নিরাপদ?

USDC উপলব্ধ কম-ঝুঁকির বিকল্পগুলোর মধ্যে একটি। এখানে একটি সৎ মূল্যায়ন দেওয়া হলো।

কী এটিকে তুলনামূলকভাবে নিরাপদ করে তোলে

- 1:1 ডলার সমর্থন: প্রতিটি USDC প্রকৃত ডলার বা ইউএস ট্রেজারি দ্বারা সমর্থিত — কোনো অ্যালগরিদমিক পদ্ধতি বা অন্যান্য ক্রিপ্টো অ্যাসেট দ্বারা নয়।

- নিয়ন্ত্রিত ইস্যুকারী: Circle মার্কিন অর্থ প্রেরণ আইন অনুযায়ী কাজ করে এবং একাধিক মার্কিন রাজ্যে লাইসেন্স হোল্ড করে। USDC এছাড়াও EU-এর MiCA প্রবিধানের সাথে সঙ্গতিপূর্ণ।

- নিয়মিত প্রত্যয়ন: মাসিক তৃতীয়-পক্ষের রিজার্ভ রিপোর্টগুলোর অর্থ হল সমর্থনটি যাচাইযোগ্য, কেবল দাবি করা নয়।

USDC-তে কীভাবে সুদ আয় করবেন

Flexible Savings বনাম Fixed-term Savings

Flexible Savings

যেকোনো সময় আপনার USDC-তে সম্পূর্ণ অ্যাক্সেস সহ প্রতিদিন সর্বোচ্চ 8% সুদ আয় করুন।

Fixed-term Savings

আপনার USDC একটি নির্দিষ্ট সময়কালের জন্য (1, 3, বা 12 মাস) প্রতিশ্রুতিবদ্ধ করুন এবং সর্বোচ্চ 10% বার্ষিক সুদ আয় করুন। যারা দীর্ঘমেয়াদী দৃষ্টিভঙ্গি নিয়ে রিটার্ন সর্বাধিক করতে চান এমন হোল্ডারদের জন্য সেরা।

Nexo-তে, USDC হোল্ডাররা Flexible Savings-এর মাধ্যমে দৈনিক সুদ আয় করতে পারেন বা Fixed-term Savings-এর মাধ্যমে উচ্চতর রেট লক করতে পারেন। উচ্চতর লয়্যালটি টিয়ারে থাকা ব্যবহারকারীদের জন্য রেট আরও বৃদ্ধি পায় — NEXO Token-এর হোল্ডাররা বেস রেটের উপরে বুস্টেড সুদ থেকে লাভবান হন। বর্তমান রেটগুলো দেখুন nexo.com/earn-crypto-এ

লোকেরা আসলে কীসের জন্য USDC ব্যবহার করে

সুদ আয় করার বাইরেও, USDC-এর বেশ কিছু ব্যবহারিক প্রয়োগ রয়েছে যা মার্চ 2026 পর্যন্ত এর প্রচলন প্রায় $79 বিলিয়নে উন্নীত করেছে।

অস্থিরতা ছাড়াই ক্রিপ্টোতে থাকা

যখন ক্রিপ্টো হোল্ডাররা ব্যাংক অ্যাকাউন্টে না গিয়ে লাভ নিতে বা ঝুঁকি কমাতে চান, তখন তারা USDC-তে রূপান্তর করেন। এটি তাদের ক্রিপ্টো ইকোসিস্টেমের মধ্যে রাখে — দ্রুত পুনরায় নিয়োজিত করার জন্য প্রস্তুত — BTC বা ETH-এর মূল্যের গতিবিধির সংস্পর্শে না এসে।

আন্তঃসীমান্ত পেমেন্ট

আন্তর্জাতিকভাবে USDC পাঠানো কয়েক মিনিটের মধ্যে নিষ্পত্তি হয় এবং একটি প্রচলিত ওয়্যার ট্রান্সফারের খরচের একটি ভগ্নাংশ মাত্র। 2025 এবং 2026 সালে, এই ব্যবহারের ক্ষেত্রটি উল্লেখযোগ্যভাবে প্রসারিত হয়েছে — Visa, Solana-তে $3.5 বিলিয়ন মূল্যের USDC নিষ্পত্তি প্রক্রিয়া করেছে, এবং বিশ্বব্যাপী বীমা ব্রোকার Aon, Ethereum-এ স্ট্যাবলকয়েন বীমা প্রিমিয়াম পেমেন্টের জন্য USDC পরীক্ষা করেছে।

DeFi এবং অন-চেইন কার্যকলাপ

USDC হল DeFi প্রোটোকলগুলিতে সর্বাধিক ব্যবহৃত স্ট্যাবলকয়েন — যা ঋণদান, ঋণগ্রহণ, তারল্য সরবরাহ এবং কোল্যাটেরাল হিসাবে ব্যবহৃত হয়। এর নিয়ন্ত্রক অবস্থান এটিকে প্রাতিষ্ঠানিক DeFi কার্যকলাপের জন্য পছন্দের স্ট্যাবলকয়েন করে তুলেছে।

AI এজেন্ট পেমেন্ট

একটি উদীয়মান ব্যবহারের ক্ষেত্র: মেশিন-টু-মেশিন পেমেন্টের জন্য AI এজেন্টদের USDC ব্যবহার। Coinbase-এর CEO 2026 সালের প্রথম দিকে উল্লেখ করেছেন যে AI এজেন্টরা ব্যাংক অ্যাকাউন্ট খুলতে পারে না কিন্তু ক্রিপ্টো ওয়ালেট হোল্ড করতে পারে — এবং USDC, একটি প্রোগ্রামেবল ডলার হিসেবে, সেই অর্থনীতির জন্য স্বাভাবিক পেমেন্ট স্তর। x402 প্রোটোকল, যা স্বয়ংক্রিয় AI পেমেন্টের সুবিধা দেয়, 50 মিলিয়নেরও বেশি লেনদেন প্রক্রিয়া করেছে, যার মধ্যে অনেকগুলিই USDC-তে করা।

2026-এ USDC: বর্তমান গতিকে কী চালিত করছে

মার্চ 2026 পর্যন্ত USDC-এর সম্পৃক্ততা এক বছরের সর্বোচ্চ পর্যায়ে রয়েছে, যা বিভিন্ন সম্মিলিত উন্নয়নের দ্বারা চালিত।

GENIUS Act স্ট্যাবলকয়েন প্রবিধান: জুলাই 2025-এ আইনে স্বাক্ষরিত, GENIUS Act স্ট্যাবলকয়েনের জন্য প্রথম মার্কিন ফেডারেল কাঠামো প্রতিষ্ঠা করেছে। এই কাঠামোর অধীনে পরিচালিত USDC ইস্যুকারীরা নিয়ন্ত্রক স্পষ্টতা লাভ করে যা অনেক প্রতিযোগীর নেই — যা প্রাতিষ্ঠানিক গ্রহণ ত্বরান্বিত হওয়ার সাথে সাথে একটি উল্লেখযোগ্য প্রতিযোগিতামূলক সুবিধা।

AI এজেন্ট অর্থনীতি: USDC স্বায়ত্তশাসিত AI লেনদেনের জন্য নিষ্পত্তি মুদ্রা হিসাবে আবির্ভূত হচ্ছে — এটি একটি প্রকৃত নতুন চাহিদার উৎস যা দুই বছর আগে বিদ্যমান ছিল না।

ইকোসিস্টেম সম্প্রসারণ: 2026 সালের গোড়ার দিকে USDC নতুন ব্লকচেইনগুলির জন্য সমর্থন যোগ করেছে, যার মধ্যে রয়েছে Base, Cardano এবং Morph, যা DeFi এবং লেয়ার 2 ইকোসিস্টেমে এর নাগাল আরও বাড়িয়েছে।

প্রায়শই জিজ্ঞাসিত প্রশ্নাবলী

১. USDC কী?

USDC একটি স্ট্যাবলকয়েন — একটি ক্রিপ্টোকারেন্সি যা মার্কিন ডলারের সাথে 1:1 অনুপাতে পেগ করা। এটি Circle দ্বারা ইস্যু করা হয় এবং নিয়ন্ত্রিত মার্কিন আর্থিক প্রতিষ্ঠানে রাখা নগদ এবং মার্কিন ট্রেজারি দ্বারা সমর্থিত। Bitcoin বা Ethereum-এর মতো এর মান ওঠানামা করে না।

২. USDC কি নিরাপদ?

USDC উপলব্ধ সবচেয়ে স্বচ্ছ এবং নিয়ন্ত্রিত স্ট্যাবলকয়েনগুলোর মধ্যে একটি। এটি মাসিক তৃতীয়-পক্ষের প্রত্যয়নসহ নগদ এবং মার্কিন ট্রেজারি দ্বারা সমর্থিত। কোনো বিনিয়োগই সম্পূর্ণ ঝুঁকিমুক্ত নয়, তবে স্ট্যাবলকয়েনগুলোর মধ্যে USDC-এর অন্যতম শক্তিশালী সুরক্ষা প্রোফাইল রয়েছে।

৩. USDC এবং USDT-এর মধ্যে পার্থক্য কী?

উভয়ই ডলার-পেগড স্ট্যাবলকয়েন, কিন্তু তারা ইস্যুকারী, স্বচ্ছতা এবং নিয়ন্ত্রক স্থিতিতে ভিন্ন। USDC মার্কিন যুক্তরাষ্ট্রে Circle দ্বারা মাসিক রিজার্ভ প্রত্যয়ন এবং MiCA কমপ্লায়েন্স সহ ইস্যু করা হয়। USDT ব্রিটিশ ভার্জিন দ্বীপপুঞ্জে Tether দ্বারা কম বিস্তারিত রিপোর্টিং সহ ইস্যু করা হয়। USDC সাধারণত নিয়ন্ত্রিত প্ল্যাটফর্ম এবং প্রাতিষ্ঠানিক ব্যবহারকারীদের দ্বারা পছন্দ করা হয়; USDT-এর সামগ্রিকভাবে একটি বড় মার্কেট শেয়ার রয়েছে।

৪. আমি কীভাবে USDC-তে সুদ আয় করব?

Nexo-এর মতো প্ল্যাটফর্মগুলো Flexible Savings অ্যাকাউন্টের মাধ্যমে USDC হোল্ডিংয়ের উপর দৈনিক সুদ অফার করে, কোনো লক-আপের প্রয়োজন নেই। Fixed-term Savings একটি নির্দিষ্ট সময়কালের জন্য আপনার USDC প্রতিশ্রুতিবদ্ধ করার বিনিময়ে উচ্চতর রেট অফার করে। সুদ প্রতিদিন প্রদান করা হয় এবং আপনার ব্যালেন্সে স্বয়ংক্রিয়ভাবে চক্রবৃদ্ধি হারে যোগ হয়।

৫. USDC-এর সুদের রেট কত?

প্ল্যাটফর্ম অনুযায়ী রেট ভিন্ন হয় এবং মার্কেটের অবস্থার সাথে পরিবর্তিত হয়। Nexo-তে, USDC রেট আপনার লয়্যালটি টিয়ার এবং আপনি ফ্লেক্সিবল বা Fixed-term Savings বেছে নিচ্ছেন কিনা তার উপর নির্ভর করে — উচ্চতর টিয়ার এবং দীর্ঘমেয়াদী মেয়াদে বেশি আয় হয়। nexo.com/earn-crypto-এ বর্তমান রেটগুলো দেখুন।

৬. USDC কি তার পেগ হারাতে পারে?

তাত্ত্বিকভাবে, হ্যাঁ — এবং এটি 2023 সালের মার্চ মাসে SVB ব্যাংকিং সংকটের সময় সংক্ষিপ্তভাবে ঘটেছিল, 48 ঘন্টার মধ্যে পুনরুদ্ধার করার আগে প্রায় $0.87-এ নেমে গিয়েছিল। স্বাভাবিক মার্কেট পরিস্থিতিতে, USDC সরাসরি রিডেম্পশনের মাধ্যমে তার $1 পেগ বজায় রাখে: যেকোনো হোল্ডার Circle-এর সাথে $1-এর জন্য USDC এক্সচেঞ্জ করতে পারেন, যা মূল্যকে স্থিতিশীল রাখে।

৭. USDC কী দ্বারা সমর্থিত?

প্রতিটি USDC, মার্কিন ব্যাংকগুলোতে রাখা নগদ এবং Circle রিজার্ভ ফান্ডের মাধ্যমে রাখা স্বল্প-মেয়াদী মার্কিন ট্রেজারি সিকিউরিটি দ্বারা 1:1 অনুপাতে সমর্থিত। একটি তৃতীয়-পক্ষ অ্যাকাউন্টিং ফার্মের মাসিক প্রত্যয়ন প্রতিবেদনগুলো নিশ্চিত করে যে রিজার্ভগুলো প্রচলিত সরবরাহের সাথে মিলে যায়।

৮. USDC কীসের জন্য ব্যবহৃত হয়?

USDC ক্রিপ্টো অস্থিরতা ছাড়া মূল্য সঞ্চয়, আন্তঃসীমান্ত পেমেন্ট, DeFi ঋণদান এবং ঋণগ্রহণ, ক্রিপ্টো-সমর্থিত ঋণের জন্য কোল্যাটেরাল এবং ক্রমবর্ধমানভাবে AI এজেন্ট লেনদেনের জন্য পেমেন্ট স্তর হিসাবে ব্যবহৃত হয়। এটি ট্রেডারদের দ্বারাও ব্যাপকভাবে ব্যবহৃত হয় যারা পজিশনগুলোর মধ্যে ক্রিপ্টো ইকোসিস্টেমের মধ্যে থাকতে চান।

এই সামগ্রীগুলো বিশ্বব্যাপী অ্যাক্সেসযোগ্য, এবং এই তথ্যের প্রাপ্যতা বর্ণিত পরিষেবাগুলোতে অ্যাক্সেস গঠন করে না, যা নির্দিষ্ট আইনব্যবস্থায় উপলব্ধ নাও হতে পারে। এই উপকরণগুলি শুধুমাত্র সাধারণ তথ্যের উদ্দেশ্যে এবং কোনো Nexo পরিষেবা ব্যবহারের জন্য আর্থিক, আইনি, ট্যাক্স বা বিনিয়োগের পরামর্শ, অফার, আবেদন, সুপারিশ বা অনুমোদন হিসাবে অভিপ্রেত নয় এবং এগুলি ব্যক্তিগত বিনিয়োগের উদ্দেশ্য, আর্থিক পরিস্থিতি বা প্রয়োজন প্রতিফলিত করার জন্য পার্সোনালাইজড বা কোনোভাবেই তৈরি করা হয়নি। ডিজিটাল অ্যাসেটগুলো উচ্চ মাত্রার ঝুঁকির অধীন, যার মধ্যে অস্থির মার্কেট মূল্যের গতিবিধি, নিয়ন্ত্রক পরিবর্তন এবং প্রযুক্তিগত অগ্রগতি অন্তর্ভুক্ত কিন্তু সীমাবদ্ধ নয়। ডিজিটাল অ্যাসেটগুলোর অতীত পারফরম্যান্স ভবিষ্যতের ফলাফলের একটি নির্ভরযোগ্য সূচক নয়। ডিজিটাল অ্যাসেটগুলো টাকা বা আইনি দরপত্র নয়, সরকার বা কোনো কেন্দ্রীয় ব্যাংক দ্বারা সমর্থিত নয়, এবং বেশিরভাগের কোনো অন্তর্নিহিত অ্যাসেট, আয়ের উৎস বা মূল্যের অন্য কোনো উৎস নেই। ব্যক্তিগত পরিস্থিতির উপর ভিত্তি করে স্বাধীন বিচার কার্যকর করা উচিত, এবং কোনো সিদ্ধান্ত নেওয়ার আগে একজন যোগ্য পেশাদারের সাথে পরামর্শ করার সুপারিশ করা হয়।