What are real-world assets (RWA) in crypto? Tokenization explained.

Mar 06•9 min read

The $25 billion idea that Wall Street finally took seriously

For years, the idea of putting real-world assets on a blockchain sounded like a solution in search of a problem. Why tokenize a Treasury bond? Why put gold on-chain? The existing system worked well enough.

Then BlackRock launched its BUIDL fund on Ethereum — and hit $520 million in 40 days. Franklin Templeton, JPMorgan, Goldman Sachs, and BNY Mellon followed. The tokenized RWA market has now surpassed $25 billion in on-chain value, up from virtually nothing three years ago. McKinsey projects it could reach $2 trillion by 2030.

The question has shifted. It's no longer whether real-world assets belong on the blockchain. It's how fast they're getting there — and what it means for anyone who owns digital assets today.

What are real-world assets (RWA)?

Real-world assets are exactly what they sound like: traditional assets that exist in the physical or financial world — things like gold, government bonds, real estate, stocks, and private credit.

Tokenizing them means converting ownership of those assets into digital tokens on a blockchain. Each token represents a claim on the underlying asset, backed by legal agreements and, increasingly, regulatory compliance.

The simplest example is already everywhere: a stablecoin like USDC is a tokenized dollar. You hold a digital token that represents $1 held in reserve. The same principle extends to any asset. A tokenized US Treasury bond represents $1,000 of actual government debt. A tokenized gold token like PAXG represents one troy ounce of physical gold sitting in a vault.

The asset itself doesn't change. What changes is how ownership is recorded, transferred, and used.

Why does tokenization matter?

Traditional financial markets have real inefficiencies that most people accept because they've always been there.

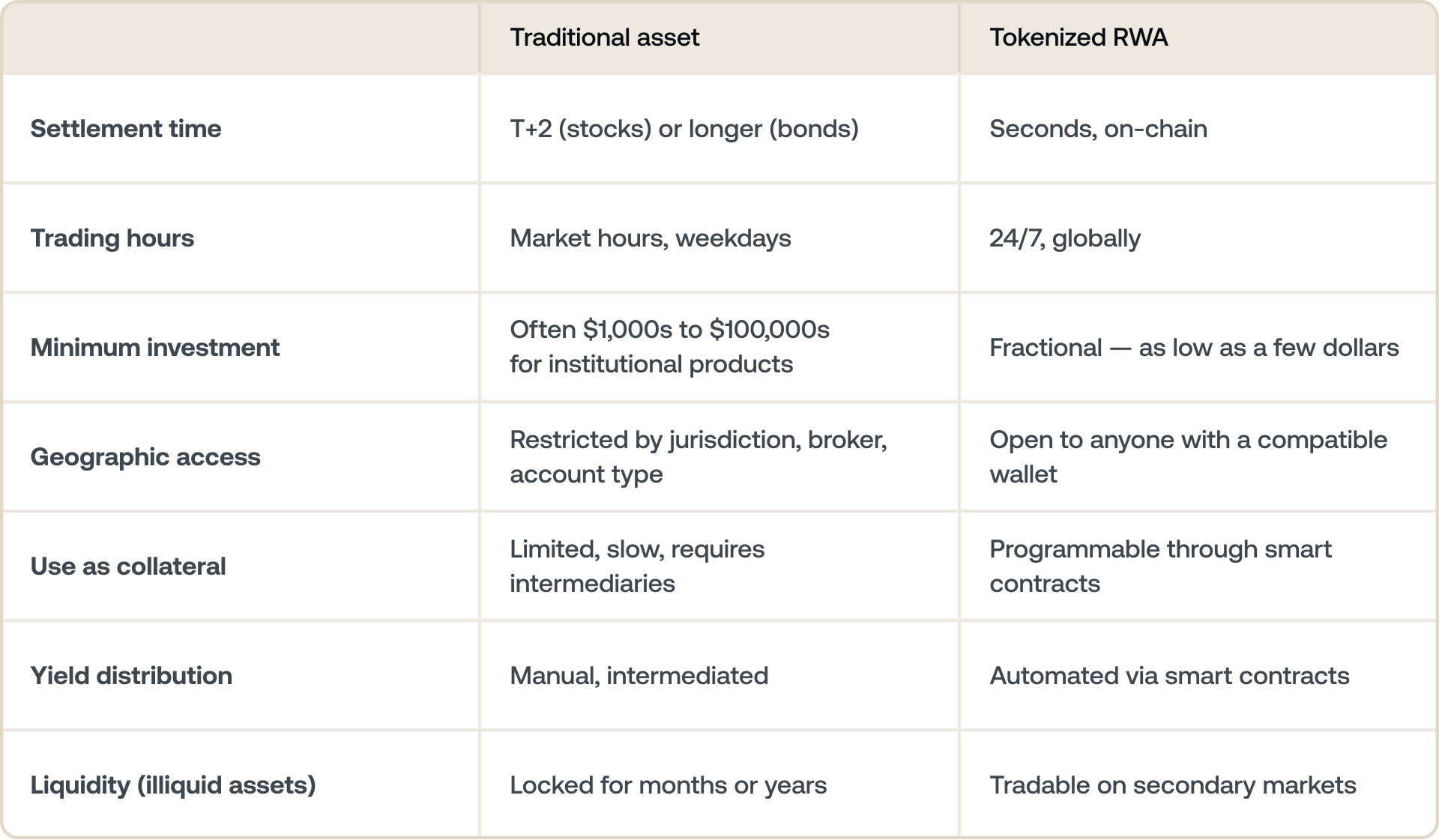

Settlement is slow: When you buy a stock, it takes two business days (T+2) to officially settle. A bond trade can take even longer. Tokenized assets settle in seconds, on-chain, automatically.

Access is restricted: Many high-quality investments — institutional money market funds, private credit, certain Treasury products — are only available to large institutions or accredited investors. Tokenization allows fractional ownership, meaning a $1 million bond can be divided into 1,000 tokens of $1,000 each. Anyone can hold a piece.

Markets have hours: Stock exchanges open at 09:30 and close at 16:00. Weekends don't exist for trading. Tokenized assets trade 24 hours a day, seven days a week, on global blockchain networks.

Liquidity is locked: Real estate, private equity, and fine art are notoriously illiquid — hard to sell quickly without a significant discount. Tokenization makes them tradable on secondary markets at any time.

Yield sits idle: A tokenized Treasury bond can automatically distribute interest payments through a smart contract. No intermediary, no delay, no paperwork.

Tokenized RWAs vs. traditional assets at a glance

What gets tokenized?

The RWA market is growing across several asset classes, each at different stages of maturity.

US Treasuries and government bonds: The largest category by far — approximately $8.7 billion on-chain, making up roughly 45% of the total tokenized RWA market. BlackRock's BUIDL fund and Franklin Templeton's BENJI token were among the first institutional-grade products, and both have attracted significant inflows. The appeal is straightforward: Treasury bonds are safe, yield-bearing assets, and tokenizing them makes that yield accessible 24/7 with instant settlement.

Tokenized gold: Gold hit all-time highs above $4,500 per ounce in 2025, driving significant interest in tokenized versions. PAX Gold (PAXG) and Tether Gold (XAUT) are the two dominant tokens — each backed one-to-one by physical gold stored in professional vaults. Tokenized gold combines the stability and store-of-value characteristics of physical gold with the portability and programmability of crypto. You can hold a fraction of an ounce, transfer it globally in minutes, and — on platforms like Nexo — earn interest on it.

Private credit: Lending protocols like Maple Finance are tokenizing private credit — loans to businesses that would traditionally only be available to institutional investors. The tokenized private credit market has grown rapidly as DeFi protocols seek real-world yield to back their products.

Real estate: Still an early stage, but projects are tokenizing income-generating properties and allowing fractional ownership. The appeal for investors is obvious: access to real estate cash flows without the minimum investment, management overhead, or illiquidity of traditional property ownership.

Stocks and equities: Major crypto platforms are starting to introduce tokenized stocks for customers in 2025. These products allow 24/7 trading of equities, including shares in private companies that would otherwise be out of reach for retail investors.

Who is driving adoption?

This is where the RWA narrative differs from most crypto trends: the institutions driving adoption are the largest financial firms in the world, not crypto-native startups.

BlackRock — the world's largest asset manager, with $10 trillion under management — has committed fully to tokenization. CEO Larry Fink has called it "the next generation for markets" and described a future of "one general ledger" where all assets are tokenized. BlackRock's BUIDL fund attracted $500 million in assets and set the template for institutional tokenized products.

JPMorgan processes billions in tokenized repo transactions through its Kinexys platform. The bank has proven that blockchain settlement can reduce capital requirements and operational risk at scale.

Franklin Templeton moved its government money market fund onto public blockchains — including Solana — making it the first major asset manager to offer a Treasury-backed product usable as 24/7 on-chain collateral.

Goldman Sachs and BNY Mellon have both taken tokenized money market funds live. The SEC issued a no-action letter to the Depository Trust Company (DTC) in December 2025, opening a path for moving securities settlement on-chain. The regulatory environment is shifting decisively in tokenization's favor.

Tokenized gold: the most accessible RWA for individuals

For most retail investors, the most accessible entry point into the RWA narrative isn't institutional bond funds — it's tokenized gold.

PAXG (PAX Gold) and XAUT (Tether Gold) are both available on Nexo. Each token is backed one-to-one by physical gold held in professional vaults, independently audited. They combine the price stability and store-of-value properties of gold with three things physical gold may not offer: instant transferability, fractional ownership down to tiny amounts, and the ability to earn yield.

On Nexo, you can:

- earn interest on PAXG and XAUT through Flexible and Fixed-term Savings, paid daily — something a gold bar in a vault can never do.

- Borrow against your tokenized gold via the Nexo Credit Line, accessing liquidity without selling your position.

- Buy and exchange between PAXG, XAUT, Bitcoin, stablecoins, and 100+ other assets 24/7.

This is what the RWA thesis looks like at the individual level: real-world value (physical gold) combined with crypto's programmability (yield, borrowing, instant transfer) in a single asset.

Note: PAXG and XAUT are not available in all jurisdictions, including the EEA. Check nexo.com/earn-crypto for current availability in your region.

The risks worth understanding

Tokenization solves real problems, but it introduces new ones.

Legal enforcement: A tokenized asset is only as good as the legal framework backing it. The token itself is a claim — and that claim needs to be enforced by courts, contracts, and regulators. This varies significantly by jurisdiction and asset class.

Counterparty risk: Holding a tokenized Treasury bond means trusting the issuer to actually hold the underlying Treasury. BlackRock and Franklin Templeton have the track record and regulatory oversight to make that credible. Smaller or unaudited issuers carry significantly more risk.

Liquidity fragmentation: Tokenized assets often live on specific blockchains or platforms with limited interoperability. Moving a tokenized bond from one platform to another isn't yet seamless — and that limits the "24/7 liquid" promise in practice.

Regulatory evolution: The rules governing tokenized securities are still being written. Progress has been significant — MiCA in Europe, the US GENIUS Act for stablecoins, the DTC no-action letter — but global regulatory frameworks remain in progress.

Frequently asked questions

1. What is RWA in crypto?

RWA — short for real-world assets — refers to traditional financial and physical assets that have been tokenized on a blockchain. The category includes tokenized government bonds (like BlackRock's BUIDL fund), tokenized gold (PAXG and XAUT), tokenized private credit, real estate, and stocks. Each token represents legal ownership of the underlying asset, combining the characteristics of that asset with the programmability and accessibility of crypto.

2. What's the best RWA crypto?

There's no single "best" RWA crypto — it depends on what you're looking for. For retail investors, tokenized gold (PAXG and XAUT) is the most accessible category, offering exposure to physical gold with the ability to generate yield, transfer instantly, and hold fractional amounts. For yield-focused investors, tokenized US Treasury products like BlackRock's BUIDL or Franklin Templeton's BENJI are the most established institutional options, though typically restricted to accredited investors. The right choice depends on your goals: store of value (gold), yield (Treasuries), or asset diversification (private credit, real estate).

3. Can I buy RWA Coin?

"RWA" isn't a single coin — it's a category of tokens that represent real-world assets. If you want to invest in the RWA narrative, you can buy individual tokenized assets like PAXG (tokenized gold) or XAUT (Tether Gold), both available on Nexo. There are also tokens of platforms that issue or service tokenized assets (such as ONDO, MKR, or Chainlink's LINK), but these are different from holding the tokenized assets themselves.

3. How to purchase RWA crypto?

The simplest way for individual investors to access tokenized real-world assets is through a platform that lists them. On Nexo, for example, you can buy PAXG and XAUT directly, then choose to hold them, earn interest on them, or use them as collateral — all from a single account. Institutional RWA products (like BUIDL or BENJI) typically require accredited-investor status and direct issuer relationships.

4. What is tokenization?

Tokenization is the process of converting ownership of a real-world asset into a digital token on a blockchain. The token is backed by a legal claim on the underlying asset and can be transferred, traded, or used as collateral on-chain. For a full breakdown of how tokenization works — including the legal, blockchain, and custody layers — see our guide to asset tokenization.

5. Why are institutions like BlackRock tokenizing assets?

Tokenization solves real operational problems for institutions: it reduces settlement time from two business days to seconds, removes intermediaries, enables 24/7 trading, and allows assets to be used as programmable collateral in smart contracts. The efficiency gains are significant enough that the world's largest asset managers have committed billions to building tokenization infrastructure.

6. How big is the RWA market?

The tokenized RWA market has surpassed $25 billion in on-chain value as of early 2026. McKinsey projects it could reach $2 trillion by 2030, while some estimates suggest $400 billion or more by the end of 2026 if institutional adoption accelerates.

7. Is tokenization the same as DeFi?

Not exactly. DeFi (decentralized finance) is a broader ecosystem of financial protocols built on blockchain. Tokenization of real-world assets is one input into DeFi — it brings traditional assets on-chain so they can be used within DeFi protocols for lending, borrowing, and yield generation.

These materials are accessible globally, and the availability of this information does not constitute access to the services described, which services may not be available in certain jurisdictions. Rates are subject to change and may vary by region, loyalty tier, and other applicable factors. Always refer to the Nexo app for your applicable rates. These materials are for general information purposes only and not intended as financial, legal, tax, or investment advice, offer, solicitation, recommendation, or endorsement to use any of the Nexo Services and are not personalized, or in any way tailored to reflect particular investment objectives, financial situation or needs. Digital assets are subject to a high degree of risk, including but not limited to volatile market price dynamics, regulatory changes, and technological advancements. The past performance of digital assets is not a reliable indicator of future results. Digital assets are not money or legal tender, are not backed by the government or by a central bank, and most do not have any underlying assets, revenue stream, or other source of value. Independent judgment based on personal circumstances should be exercised, and consultation with a qualified professional is recommended before making any decision.