Markets Today - June 15, 2026

Jun 15•4 min read

-3.png)

Daily analysis of crypto markets and the forces shaping them, from the Nexo research desk.

Peace dividend and Fed discount

Bitcoin climbed above $65,500 at the Monday open as confirmation of a U.S.–Iran interim peace deal and President Trump's announcement that the Strait of Hormuz will reopen Friday drove a broad risk-on rotation. Oil prices fell sharply, supporting global risk assets. Spot Bitcoin ETFs broke a five-session outflow streak on June 12, recording $85.85 million in net inflows, their strongest single-day figure in roughly four weeks. The relief rally is real, but it carries conditions. Markets are not fully pricing a permanent resolution until the June 19 signing in Switzerland holds. Seven G10 central bank meetings this week add a further layer of event risk.

Bitcoin

Bitcoin is back above $65,500 on Monday, up roughly 2% over 24 hours, but markets are pricing in a moderate recovery rather than a breakout. Polymarket assigns 71% odds to Bitcoin touching $67,500 before month-end — a 3% move from current levels — and 34% to $70,000. Options data reinforces that read. Upside implied volatility has fallen back to pre-war levels and the cost of downside protection has compressed sharply, reflecting hedges being unwound rather than fresh bullish bets being placed.

Institutional demand is showing signs of recovery. ETF flows turned positive on June 12, ending the most sustained net withdrawal period since the products launched in January 2024. The FOMC is the key near-term risk. The March precedent is worth noting: seven sessions of inflows totaling $1.17 billion reversed into a $163.52 million single-session outflow on the day the Fed met. Institutional positioning into Wednesday carries that same event-risk pattern.

Ethereum & Altcoins

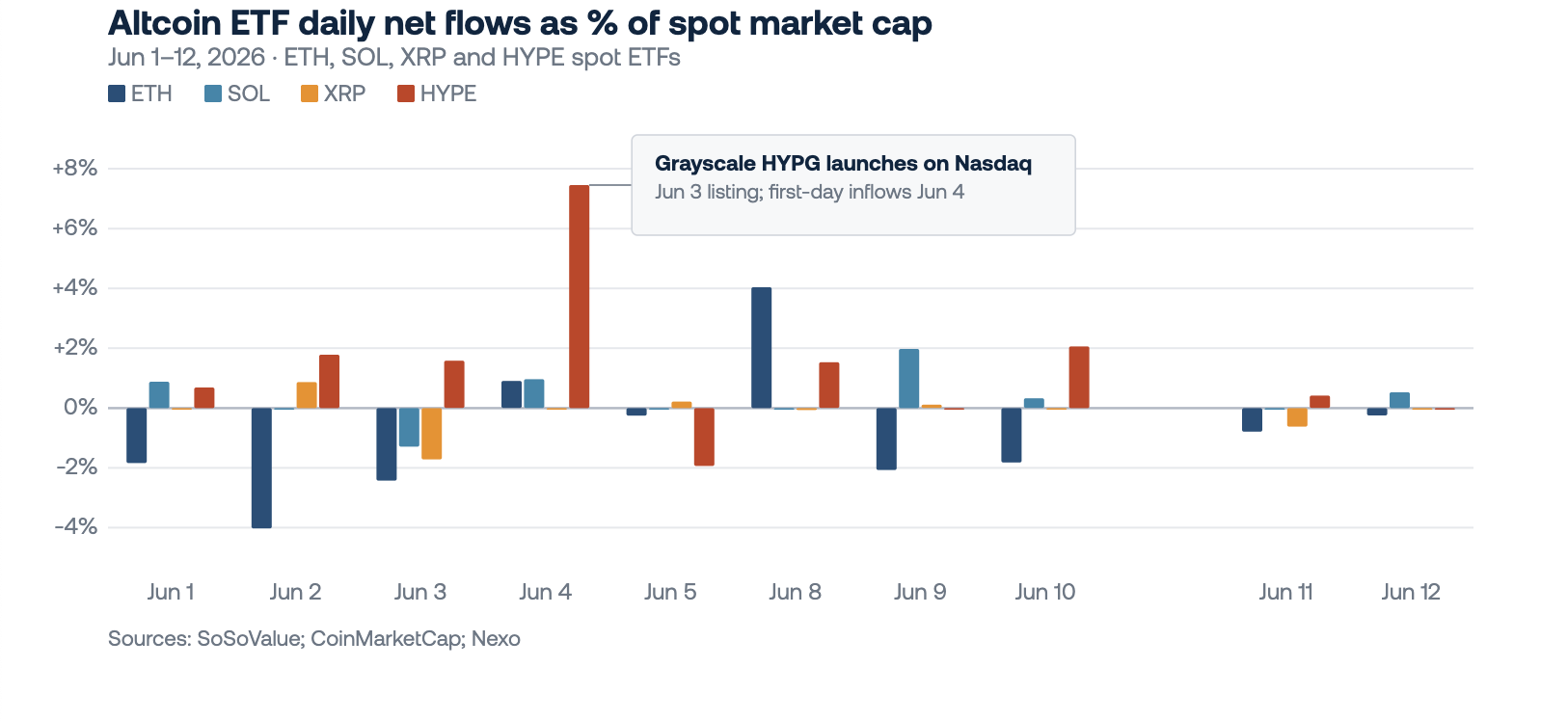

Altcoins followed Bitcoin up, with Solana and HYPE leading the top ten recovery. ETF flows tell a more nuanced story. Ethereum spot ETFs recorded $4.95 million in net outflows on Friday, diverging from Bitcoin ETFs which turned positive for the first time in five sessions. The gap is wider in aggregate. ETH spot ETFs shed $712.56 million from May 11 through May 29 and a further $356.76 million in June, pushing net assets from a $13.45 billion peak to $9.16 billion — a 32% decline in under four weeks.

Demand has not left the altcoin space, it has become selective. Solana and XRP ETFs added a combined $348.47 million in May and stayed broadly flat in June, with both tokens gaining 6.6% and 5.3% between June 12 and June 14 on the ceasefire rally. HYPE is the clearest expression of that selectivity, accumulating $154.61 million in ETF inflows in under a month. On June 4, HYPE ETFs recorded their largest single-day inflow relative to market cap across all alt ETFs, driven by Grayscale's HYPG listing on Nasdaq — the third U.S. HYPE ETF to list in three weeks.

Investor interest in HYPE is underpinned by a fee buyback model that converts platform trading volume directly into token demand, giving the asset a structural bid that most altcoins lack.

Macro & Institutional

Two events bookend the week. The FOMC decision Wednesday and the formal U.S.–Iran peace signing in Switzerland on Friday pull in opposite directions. Cheaper oil eases the inflation pressure that pushed central banks toward tighter policy, but whether that feeds through to markets depends on what Warsh signals.

The main risk is the dot plot and the forward guidance. Current pricing assigns approximately 40% odds of a December rate hike, a significant shift from earlier expectations of multiple cuts, and an upward revision to the funds path would validate that repricing.

The BoJ concludes Tuesday and is near-certain to raise rates to 1% for the first time since 1995. Governor Ueda will not attend or vote, having been hospitalized, which makes the forward guidance harder to read than usual. A hawkish tone on further normalization would pressure USD/JPY and risk unwinding carry positions across risk assets.

Looking Ahead

Tuesday's BoJ decision is the immediate focus. China's May activity data — industrial production, retail sales, and fixed asset investment — prints the same day and will set the tone for emerging market risk appetite. Wednesday is the week's focal point. U.S. May retail sales offer the first clean read on consumer resilience after the April–May energy spike, and the FOMC decision, economic projections, and Warsh's inaugural press conference follow in the evening. Thursday brings U.K. labor data and the BoE decision, where the MPC vote split will matter as much as the hold. Friday's tape is thin as U.S. markets are closed for Juneteenth but the formal U.S.–Iran peace signing in Switzerland adds a geopolitical event-risk overlay to close the week.

Author: Dessislava Ianeva, Analyst at Nexo’s Dispatch

This material is produced by Nexo for informational purposes only and does not constitute financial, investment, legal, or tax advice, or a recommendation to transact in any digital asset. Views are the author's as of the date of publication and may change without notice. Information is from sources believed reliable, but Nexo makes no warranty as to its accuracy and accepts no liability for any loss arising from reliance on this material.