Why crypto could be part of the next generation of wealth

May 20•8 min read

Somewhere between $84 trillion and $124 trillion is moving steadily, as the largest intergenerational asset shift in recorded history plays out over the next two decades.

Baby Boomers and the Silent Generation built their wealth through traditional means: real estate, equities, and pension systems. As they begin to pass it down, the generation receiving it thinks about money differently.

That difference is structural. It has significant implications for what wealth looks like going forward.

What is the Great Wealth Transfer?

The Great Wealth Transfer is the name given to the largest intergenerational movement of assets in recorded history. As Baby Boomers (born between 1946 and 1964) age, the wealth they accumulated over decades is moving to their children and grandchildren: primarily Gen X, Millennials, and Gen Z.

It sounds like a financial planning concept. It's actually a civilizational event.

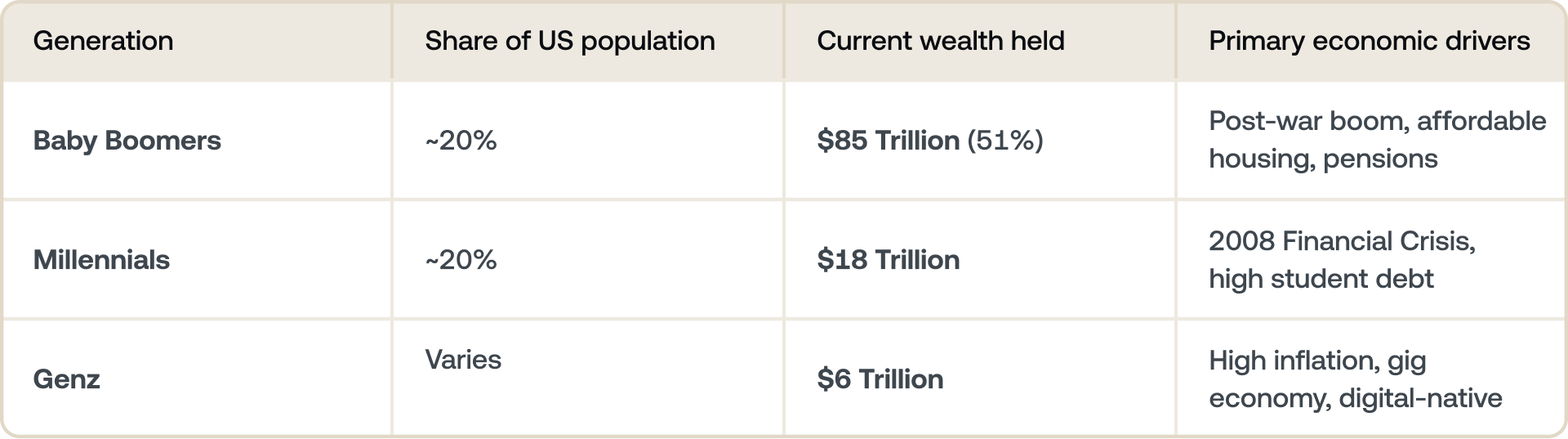

Baby Boomers benefited from a near-perfect set of economic conditions. They entered the workforce during a long post-war boom, bought homes before prices became structurally unaffordable, held jobs with defined-benefit pensions, and invested in equities through one of the longest bull markets in history.

Today, the wealth gap between generations is stark:

But that gap is now beginning to close—not through wage growth or policy change, but through inheritance. The assets Boomers built are beginning to flow downward, and the scale of what's moving is genuinely difficult to comprehend.

Some of it arrives as direct inheritance. Some arrive as gifts, trusts, co-signed mortgages, educational support, and business capital. All of it adds up to a generational reset of who holds what.

Why does it matter beyond family finances? Because wealth shapes markets. When a generation inherits trillions, the assets they choose to hold become the assets that define the next era of investing. Real estate, equities, bonds, and pension funds were the vehicles of the Boomer era. The generation now inheriting their wealth has different instincts—and different infrastructure available to act on them.

The scale of what's happening

The numbers attached to the Great Wealth Transfer are large enough to be difficult to process. To put it in perspective, the entire US GDP sits at approximately $28 trillion. The transfer already underway dwarfs it several times over:

- $124 Trillion: The total assets projected by Cerulli Associates to change hands by 2048.

- $16 Trillion: The amount set to move before 2033 alone.

- $54 Trillion: The amount that will move intragenerationally to spouses first before reaching younger heirs.

The pace is already accelerating. Between late 2019 and late 2024, Millennials' total net worth grew from $3.9 trillion to nearly $16 trillion—a quadrupling in five years driven by asset price growth, career progression, and early inheritance flows. The transfers recorded in 2024 alone included $297.8 billion passed to 91 heirs, a 36% increase year-on-year, according to UBS.

While Gen X leads the near-term picture (with an average inheritance age of 46 for fortunes over $5 million), Gen Z and Millennials follow closely in the decades behind.

Why this generation is different

Every generation inherits the financial framework of the one before it. Baby Boomers inherited post-war institutional trust—banks, pension funds, government bonds—and built their wealth within that system.

Millennials and Gen Z are inheriting something entirely different: a financial system that failed them early, and a digital alternative that didn't.

The 2008 financial crisis hit Millennials at the worst possible time—when they were entering the workforce, taking on student debt, and trying to buy their first homes. The institutions that were supposed to be trustworthy either collapsed or required bailouts. That experience permanently shaped an entire generation's relationship with traditional finance.

A January 2026 OKX survey of 1,000 Americans highlighted this massive behavioral divide:

- 74% of Baby Boomers gave high trust scores to traditional banks.

- Only one in five Millennials and Gen Z echoed that trust.

- Conversely, 40% of Gen Z and 41% of Millennials trust crypto platforms at a 7 or higher on a 10-point scale (compared to just 9% of Boomers).

Younger generations are not simply less trusting of banks. They are, for the first time in modern history, more trusting of an alternative.

That alternative is crypto, and the adoption data reflects it:

- The Core Demographic: Millennials currently account for 57% of all crypto owners in the US. Over half of Gen Z globally has owned or currently holds cryptocurrency.

- Rapid Growth: One in four US adults now owns crypto, according to the National Cryptocurrency Association's 2026 State of Crypto Holders Report—an increase of 12 million holders in a single year.

- Portfolio Dominance: Among Millennials, 62% report that crypto accounts for at least one-third of their total wealth.

These aren't speculative positions held by early adopters waiting to cash out. For a large and growing portion of the wealth-receiving generation, crypto is already a core asset class sitting alongside, and sometimes ahead of, traditional equities.

What's changed in the infrastructure

The criticism of crypto as a serious wealth-building tool has historically rested on legitimate concerns: volatility, lack of institutional infrastructure, and regulatory uncertainty. Those objections made sense in 2017. They make far less sense in 2026.

The infrastructure that serious wealth management requires now exists in crypto—and in several dimensions, it rivals what traditional finance offers. For a broader look at how to approach this, learning how to build wealth with crypto is a practical starting point.

1. Generational yield

The contrast in returns between traditional finance and crypto is stark. For example, a platform like Nexo offers competitive annual yields that leave standard bank accounts far behind:

2. Pledging collateral without selling

The liquidity mechanic is equally significant. One of the defining features of traditional wealth management is the ability to borrow against assets without selling them.

Wealthy families have done this for generations, pledging stocks or real estate to access cash while keeping their positions intact.

Crypto-native platforms now offer the exact same approach. On Nexo, you can borrow against your crypto at rates starting from 1.9% APR, using BTC, ETH, SOL, and other assets as collateral.

The asset stays in your portfolio, the position stays open, and the liquidity is available when you need it. There are no credit checks and repayment schedules.

3. Institutional legitimacy

Beyond yield and liquidity, the diversification tools that previously required multiple brokers, advisors, and institutions can now be managed within a single ecosystem.

Institutional legitimacy has arrived faster than most expected. Bitcoin spot ETFs are actively trading in the US, with legacy giants like Goldman Sachs disclosing over $108 million in positions. Corporate treasury holdings of Bitcoin have become a standard boardroom conversation.

Furthermore, regulatory frameworks like MiCA in the EU and the advancing CLARITY Act in the US Senate are shifting the global landscape toward accommodation rather than prohibition. This fundamentally changes the risk profile of holding crypto as a long-term wealth asset.

The wealth transfer meets the wealth infrastructure

Here's where the two trends converge.

The generation inheriting the Great Wealth Transfer is the same generation that already holds crypto, already trusts crypto platforms, and already uses crypto infrastructure to earn yield and access liquidity.

When $124 trillion begins moving in earnest, a significant portion of it will flow into ecosystems and platforms built on blockchain infrastructure. The reason won’t be because of ideology, but because that's where the recipients already live.

This is not a prediction about crypto prices. It's an observation about where financial gravity is moving. Wealth follows the people who hold it, and the people holding the next generation of wealth have already made their preferences clear.

There's also a compounding effect worth considering. Crypto assets, unlike real estate or pension funds, are natively digital—they transfer instantly, globally, without lawyers, probate, or geographic restriction. The generations that grew up with smartphones expect financial infrastructure to work the way software does.

What this means if you're building wealth today

The Great Wealth Transfer is not an event you wait for. It's a context you can act within now—and the infrastructure to do so has never been more developed.

If you already hold crypto, the question is whether your assets are working as hard as they could be. Holding BTC or ETH in a cold wallet that generates no yield is the crypto equivalent of leaving cash in a zero-interest checking account.

The yield infrastructure now exists to change that:

- Flexible Savings: Let you earn on assets while maintaining instant access to them. If you want to dig into how that works in practice, understanding how to earn interest on crypto covers the mechanics.

- Fixed-term Savings: Offer higher rates for capital you're comfortable setting aside for a defined period to compound your long-term position.

Note: Rates apply to eligible clients with a minimum portfolio balance of $5,000, and vary by asset and Nexo Loyalty Tier. Rates are subject to change — always refer to the Nexo app for the rates applicable to your account.

If you're thinking about wealth across a longer horizon—the kind of multi-decade wealth-building that the Great Wealth Transfer is forcing into focus—the borrow mechanic matters just as much as yield.

Building wealth without selling your best-performing assets is how the wealthiest families have always operated. Crypto infrastructure simply makes that approach available at retail scale.

Reviewing the mechanics of borrowing against your Bitcoin explains how to navigate it if you're approaching it for the first time.

The shift toward digital wealth doesn't always show up in a single headline, but the underlying gravity is undeniable.

These materials are accessible globally, and the availability of this information does not constitute access to the services described, which services may not be available in certain jurisdictions. These materials are for general information purposes only and not intended as financial, legal, tax, or investment advice, offer, solicitation, recommendation, or endorsement to use any of the Nexo Services and are not personalized or in any way tailored to reflect particular investment objectives, financial situation, or needs. Digital assets are subject to a high degree of risk, including but not limited to volatile market price dynamics, regulatory changes, and technological advancements. The past performance of digital assets is not a reliable indicator of future results. Digital assets are not money or legal tender, are not backed by the government or by a central bank, and most do not have any underlying assets, revenue stream, or other source of value. Independent judgment based on personal circumstances should be exercised, and consultation with a qualified professional is recommended before making any decision.