Markets Today - June 25, 2026

Jun 25•4 min read

.png)

Daily analysis of crypto markets and the forces shaping them, from the Nexo research desk.

Bitcoin visits key support as Core PCE lands in line and the AI trade rebounds

Markets are digesting Micron's record quarter alongside today's Core PCE print, which came in at 3.4% year-on-year and 0.3% month-on-month — in line with expectations. Bitcoin dipped to the low $58,000s on the release before recovering and stabilising above $59,000, while equity futures remain higher with Nasdaq 100 futures up 2.2% and S&P 500 futures up 0.8% on the back of Micron's blockbuster results and Qualcomm's AI growth targets. The total crypto market cap remains under pressure but is stabilising. Brent crude has fallen below $73, erasing virtually all of the geopolitical risk premium built up during the Iran conflict. Gold has bounced back above $4,000 to around $4,017 after briefly dipping below the level earlier in the session, and the dollar index has turned lower to 101.18 following the in-line inflation reading.

Bitcoin

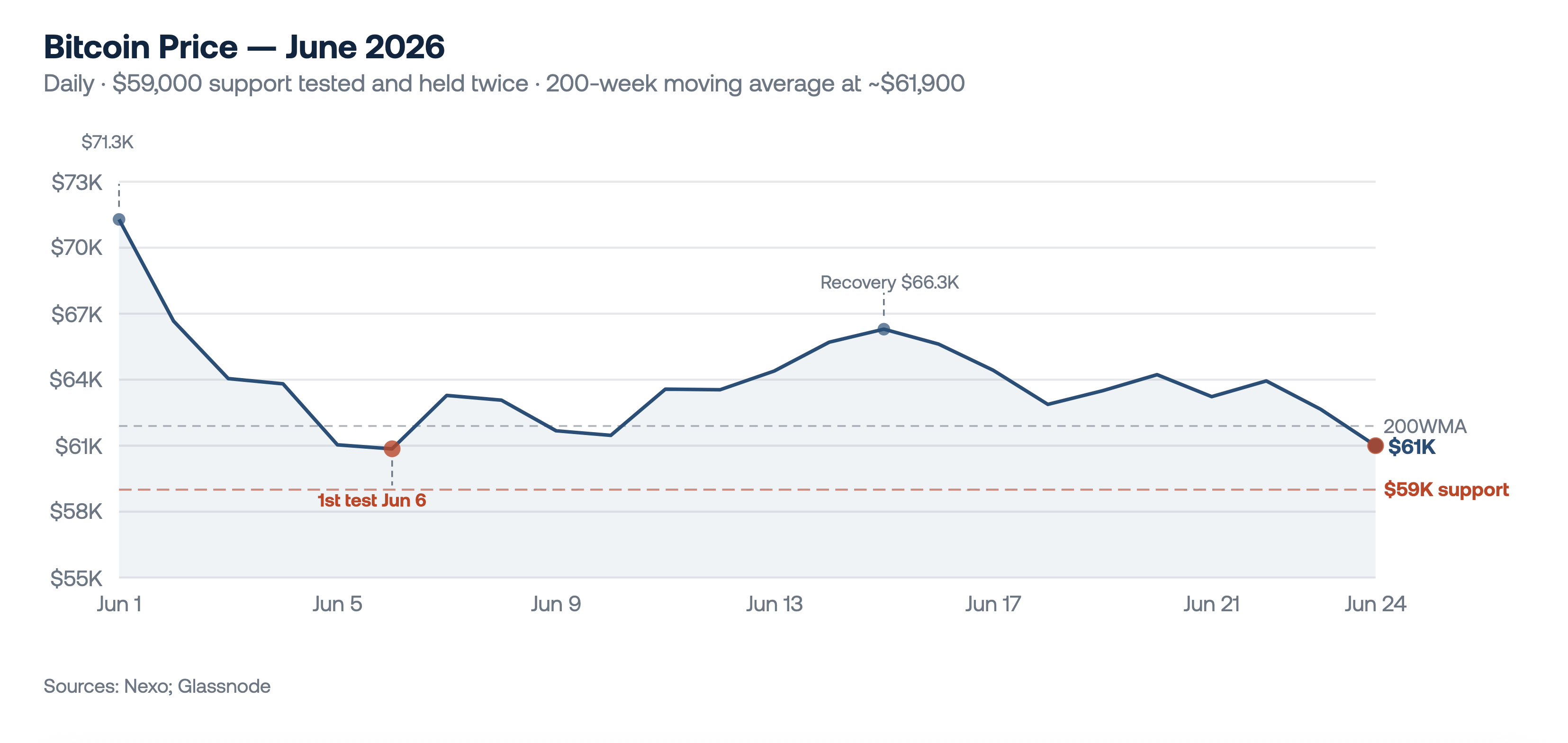

Bitcoin dipped to the low $58,000s immediately following the PCE release before recovering and stabilising above $59,000 — a level that has now confirmed itself as meaningful support, having held on two separate occasions this month. The first was on June 5, when a bounce from $59,000 carried Bitcoin back to $67,000 in the days that followed. The pattern is repeating: $59,000 is the structural line the market will continue to watch heading into the weekend.

On the PCE data itself, the headline reading of 4.1% year-on-year and core at 3.4% — while above the Fed's 2% target — came in line with expectations, removing the most bearish scenario for risk assets. With oil prices having fallen nearly 39% from their May peak and now approaching pre-war levels, the broad market view is that May represents the inflation peak. Core inflation at 3.4% on a 12-month basis will not retreat as quickly as the energy-driven components, but the directional shift is now clearly in play. That framing is broadly constructive for the rate narrative heading into the second half of the year.

Spot Bitcoin ETF outflows deepened on Wednesday to $469 million — their largest single-day figure since June 2 — extending a seventh consecutive week of net redemptions. The pace of outflows remains the key variable to watch for a sustained recovery. On the constructive side, on-chain data shows long-term holders now control approximately 14.8 million BTC, an all-time high, with this cohort continuing to accumulate through the current drawdown as they have at prior cycle lows. In derivatives markets, Bitcoin futures open interest has climbed to 763,000 BTC — the highest since early June — suggesting fresh positioning is entering the market ahead of the weekend.

Ethereum & Altcoins

The PCE-driven pullback was felt across the wider altcoin market, with Ethereum mirroring Bitcoin's move before recovering to around $1,564. XRP, Solana, BNB, and Cardano each saw similar intraday swings before stabilising. The altcoin complex is broadly recovering alongside Bitcoin as equity sentiment improves on the back of Micron's results.

Macro & Institutional

Micron's fiscal third-quarter results delivered a decisive answer to the week's central question — revenue came in at $41.46 billion, more than four times the year-ago level, with data center revenue jumping more than sevenfold to $11.5 billion and gross margins expanding to 84.9%. Qualcomm added to the momentum, forecasting $15 billion in annual data center sales by 2029. Together the two prints confirm that AI infrastructure demand remains robust — the two-day chip selloff was a valuation reset, not a fundamental shift.

Today's PCE data — headline at 4.1% and core at 3.4% year-on-year, came in line with expectations, representing what the market is broadly treating as the inflation peak. With oil now approaching pre-war levels, the energy-driven component of inflation is expected to reverse sharply in June data. Core inflation will be stickier, but the direction of travel has shifted. Markets are now pricing a roughly one-third probability of a July rate hike and 66% probability by September. The in-line reading was enough to reverse earlier moves in gold and the dollar — gold bounced back above $4,000 to around $4,017, while the dollar index turned lower to 101.18 after its recent run to 13-month highs. Brent below $73 and normalising Hormuz traffic remain the most direct structural improvements in the macro backdrop since February. All 32 major U.S. banks passed the Fed's annual stress test, absorbing $708 billion in projected losses with capital falling only 1.6 percentage points — a clean outcome that removes one source of uncertainty heading into a tighter rate environment.

Looking Ahead

With Core PCE now in the rearview mirror and landing broadly in line, the near-term rate narrative is slightly more constructive than it was 24 hours ago. Friday's University of Michigan Consumer Sentiment and Inflation Expectations survey closes the week — a read on whether lower energy prices and the Iran deal are beginning to shift the public's inflation outlook, and a data point that could reinforce the peak inflation narrative if expectations move lower. For Bitcoin, $59,000 remains the line that matters heading into the weekend — a hold above it keeps the recovery thesis intact.

Author: Iliya Kalchev, Analyst at Nexo’s Dispatch weekly bulletin.

This material is produced by Nexo for informational purposes only and does not constitute financial, investment, legal, or tax advice, or a recommendation to transact in any digital asset. Views are the author's as of the date of publication and may change without notice. Information is from sources believed reliable, but Nexo makes no warranty as to its accuracy and accepts no liability for any loss arising from reliance on this material.