Markets Today - May 26, 2026

May 26•4 min read

Daily analysis of crypto markets and the forces shaping them, from the Nexo research desk.

Bitcoin slips below $77,000 as geopolitics weigh on risk appetite

BTC opened Tuesday below $77,000 as geopolitical risk continued to weigh on sentiment. Monday's U.S. strikes in southern Iran lifted Brent toward $98 a barrel. The cross-asset response was uneven. South Korea's KOSPI printed a record on catch-up trade and chip names rallied across Asia. The Nikkei eased from Monday's high and digital assets stayed under pressure. Thursday's April PCE will test Waller's Friday pivot, which backed removing the FOMC's easing bias and signaled that a hike is now as likely as a cut.

Bitcoin

Bitcoin traded near $76,860 in early hours on May 26, with total crypto market cap at $2.56 trillion, down 0.65% over 24 hours. Leveraged positioning is calm. BTC perpetual funding has averaged around 5% annualized over the past week, enough to signal modest long bias, not enough to flag crowding. Per Glassnode, BTC futures open interest sits at $36.23 billion, well below the October 2025 peak of $68.68 billion. One-month implied volatility has eased to 32.9% from a 30-day peak near 39.6% in late April.

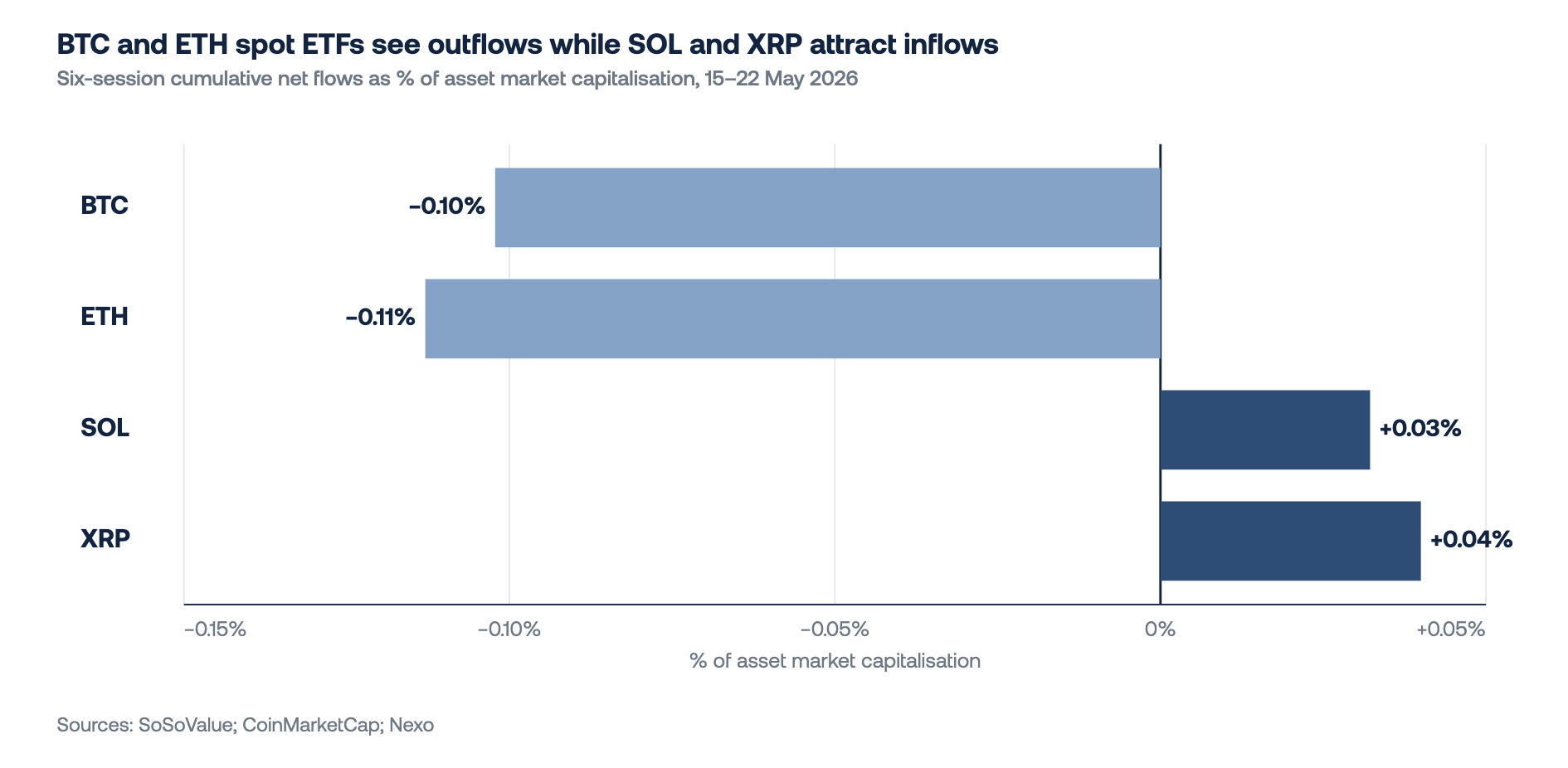

U.S. spot Bitcoin ETFs recorded a net outflow of $105.19 million on 22 May, the sixth consecutive outflow day, with cumulative six-day redemptions of roughly $1.55 billion — about 1.6% of total ETF assets. The combined picture is investors trimming crypto exposure, not panicking. Funding is steady, open interest is well off the highs, and options traders are pricing in less risk of a big move, not more. Thursday's April PCE inflation print is the week's main catalyst for crypto, as it will shape how the Fed responds in coming meetings.

Ethereum & Altcoins

Ether and major altcoins followed Bitcoin lower in modest moves: ETH down 0.4% on the day, SOL down 1.6%, XRP down 0.8%. Leverage across altcoins sits well below 2025 expansion levels. ETH futures open interest is $21.55 billion versus a 2025 average of $25.7 billion and an August peak of $51.7 billion. SOL open interest is $3.74 billion against a 2025 average of $6 billion. XRP open interest is $1.83 billion against a 2025 average of $4 billion. Funding is positive but moderate, pointing to limited directional conviction.

Institutional flows show a split picture. ETH spot ETFs recorded an outflow of$6.67 million on 22 May for the sixth day in a row, for a total of $282 million. SOL and XRP spot ETFs continued to attract inflows over the same window, adding approximately $15.6 million and $32.9 million respectively. In market-cap terms, flows span roughly −0.1% to +0.04%. The complex reads as measured engagement: light leverage, calm funding, ETH out, SOL and XRP in.

Credit&Leverage

Galaxy Research's Q1 2026 lending report, published last week, puts total crypto-collateralized lending at $67.4 billion, down $3.6 billion (-5.1%) over the quarter. DeFi borrows fell 14% to $28.2 billion, the second consecutive quarterly contraction on-chain. CeFi contracted just 7% to $25.4 billion in its first quarterly decline since Q4 2023, but still ended above Q3 2025 levels despite BTC, ETH, and SOL trading 34%, 48%, and 59% below pre-October 10 prices, respectively. Only four CeFi lenders grew their books in the quarter, Nexo among them. Nexo and the other two companies in the top three now hold 77.7% of CeFi lending — concentration consistent with Galaxy's read of gradual, orderly deleveraging.

Macro & Institutional

Oil remains the primary cross-asset driver. U.S. forces struck missile launch sites and mine-laying vessels in southern Iran late Monday. U.S. Central Command (CENTCOM) said the action was defensive and the ceasefire holds. Brent had fallen nearly 3% Monday on framework-deal reports. Tuesday's strikes lifted it back toward $98 a barrel. The U.S. dollar and Treasury yields continue to track energy-driven inflation expectations.

Thursday's April PCE release is the week's main data test. In a speech on Friday, Fed Governor Christopher Waller estimated headline inflation at 3.8% year-on-year (from 3.5%) and core at 3.3% (from 3.2%). An upside surprise validates his pivot to backing removal of the FOMC's easing bias and forces more hike risk into the curve. A softer print leaves him isolated and pressures the dollar lower. Oil and the Hormuz track remain the dominant cross-asset catalyst.

Looking Ahead

With U.S. CPI already out, focus turns to Thursday's data session: April PCE (3.5% headline, 3.2% core, both prior), Q1 GDP second estimate (2.0% consensus), durable goods, personal income and spending, and jobless claims. Wednesday brings weekly ADP employment and an ECB press conference. Friday closes with Chicago PMI and Canada Q1 GDP. Fed speakers across the week include Jefferson, Goolsbee, Williams, and Bowman. Inflation data and the Fed reaction function remain the dominant cross-asset catalyst this week.

Author: Dessislava Ianeva, Analyst at Nexo’s Dispatch

This material is produced by Nexo for informational purposes only and does not constitute financial, investment, legal, or tax advice, or a recommendation to transact in any digital asset. Views are the author's as of the date of publication and may change without notice. Information is from sources believed reliable, but Nexo makes no warranty as to its accuracy and accepts no liability for any loss arising from reliance on this material.