Markets Today - June 1, 2026

Jun 01•4 min read

Daily analysis of crypto markets and the forces shaping them, from the Nexo research desk.

Crypto flat as traders await ceasefire extension

Crypto markets are holding broadly flat as traders stay on the sidelines ahead of a potential U.S.-Iran ceasefire extension. A 60-day deal and nuclear talks have been teased in press briefings but not formally confirmed. Total market capitalization stands at $2.47 trillion, with the Fear & Greed Index at 33, indicating Fear.

Traditional markets are edging higher on deal optimism and AI momentum. Nvidia's entry into the Windows laptop market and SoftBank surging 11% on its OpenAI and Arm stakes drove Nasdaq 100 futures up 0.6% but crypto has not followed.

Bitcoin

Bitcoin trades near $72,700, down approximately 1.5% over 24 hours, continuing a drift that has unwound the recovery from May lows. Derivatives show no forced deleveraging. Funding is neutral, leverage closures have flatlined, and open interest in BTC terms is rising. The selling is orderly, driven by spot rather than liquidations.

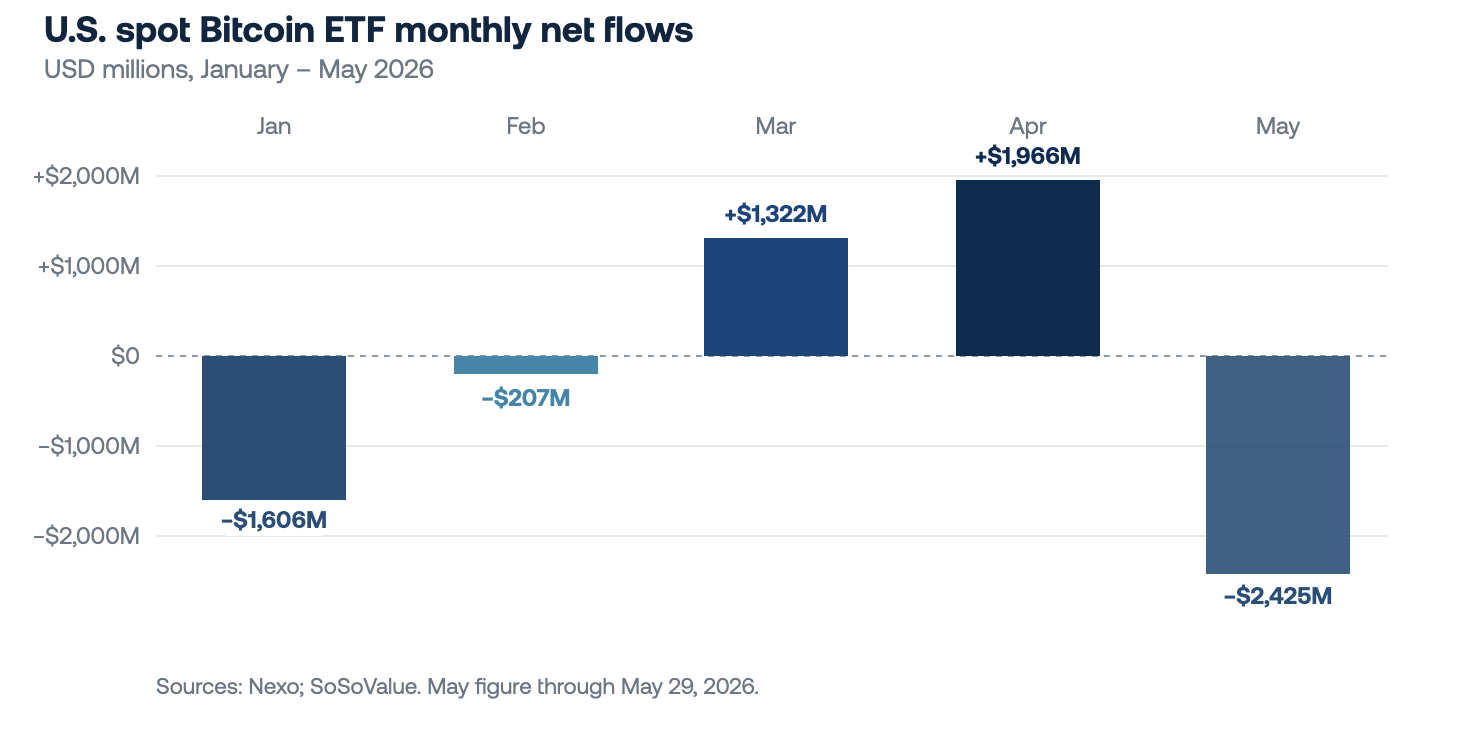

JPMorgan flagged on May 28 that simultaneous outflows from both Bitcoin and gold ETFs reflect investors stepping back from inflation and geopolitical hedges — not a rotation between the two — as Iran deal hopes reduce the urgency of hard-asset positioning. U.S. spot ETFs logged 10 consecutive sessions of outflows between May 15 and May 29, draining $2.97 billion — a new record breaking the previous eight-session streak from early 2025. May is tracking as the third-worst month since launch at approximately $2.4 billion in net outflows, behind only February and November 2025.

The risk is that this unwind has further to run. As per Glassnode data, Q2 spot CVD has been negative in four of the past five years and Q3 weaker still, and with summer liquidity thinning, a U.S.-Iran resolution may prove the more consequential variable than any technical level.

Ethereum & Altcoins

Ethereum trades around $1,980, down 1.6% over 24 hours, with spot ETH ETFs joining BTC in outflows as part of the broader institutional derisking. Standard Chartered maintained its ETH price target, comparing ETH's position to Amazon in 2001 — lower in price while the underlying network keeps growing. The broader market is lower. XRP has dropped 2.8% to $1.30, SOL is down 1.75% to $81. The Altcoin Season Index stands at 31/100, though SOL ETFs continued attracting inflows through May, pointing to selective rather than wholesale risk-off. HYPE is up nearly 7% over 24 hours to nearly $73 and 71% over the past month on the news of its partnership with Intercontinental Exchange (ICE), the parent company of the NYSE. Stellar has added 7% over 24 hours and 73% over the past seven days. VanEck's first U.S. spot BNB ETF launched on Nasdaq on May 29 under VBNB, though early volumes remain negligible.

Macro & Institutional

The Iran war entered its fourth consecutive month, with the U.S. striking Iranian radar and drone sites over the weekend. Brent crude rose approximately 3% on Monday to near $94 per barrel, reversing a roughly 10% weekly decline driven by ceasefire optimism. The pattern is becoming familiar: diplomatic signals compress risk premiums, military escalation rebuilds them, and neither side has delivered a resolution, leaving energy markets, and by extension inflation expectations, structurally elevated.

European stocks opened subdued, with Eurozone bond yields rising as markets priced ECB rate hikes in response to the energy shock. The dollar remains supported by hawkish Fed signals, with markets pricing approximately 17 basis points of tightening for the year. China's official manufacturing PMI slipped to 50.0 in May while the non-manufacturing PMI rebounded to 50.1. The Caixin manufacturing PMI moderated to 51.8, outperforming forecasts. Tokyo CPI eased to 1.4% year-on-year in May, yet the Bank of Japan is widely expected to hike in June given negative real interest rates and continued wage growth.

Looking Ahead

Attention turns to a heavy U.S. data week. U.S. ISM manufacturing releases today (consensus at 52.7), followed by ISM services and the Fed Beige Book on Wednesday, and May non-farm payrolls on Friday (consensus at +90,000). Flash May CPI prints for Germany, France, Spain, and Italy are also due today. If labor data hold firm and inflation moderates, pressure on Bitcoin's current level could ease. An upside surprise in price data would likely extend consolidation.

Author: Dessislava Ianeva, Analyst at Nexo’s Dispatch

This material is produced by Nexo for informational purposes only and does not constitute financial, investment, legal, or tax advice, or a recommendation to transact in any digital asset. Views are the author's as of the date of publication and may change without notice. Information is from sources believed reliable, but Nexo makes no warranty as to its accuracy and accepts no liability for any loss arising from reliance on this material.