Bitcoin's reserve and credit layers come into view

May 27•6 min read

In this patch of your weekly Dispatch:

- Nexo grows Q1 loan book

- De-escalation trade capped

- BTC implied vol stays compressed

Market cast

BTC: weekly and daily indicators offer no directional bias

On the weekly chart, price is holding marginally above the 20-period SMA, leaving the longer-term trend intact but unconvincing. RSI is neutral, offering no momentum bias. Stochastic has rolled out of overbought, easing the buy-side pressure built up at recent highs. The MACD histogram remains positive, so bullish momentum is still in place. ADX is declining, indicating that trend strength is weakening regardless of direction.

On the daily chart, we see the same setup in compressed form. RSI and Stochastic are flat and neither gives a directional cue. The MACD histogram sits marginally below zero, a mild bearish tilt rather than an outright sell signal. ADX is at low levels, the standard reading for a range-bound tape.

Key levels to watch. On the downside, immediate support sits around $75,500, with the next zone at $70,000–$71,000. The weekly 20-period SMA may also act as dynamic support. On the upside, immediate resistance is around $78,000–$79,000, with the next zone at $82,000.

The big idea

Bitcoin's reserve and credit layers come into view

May has been a bumpy de-escalation trade. Bitcoin's range has held through it, but on a discretionary bid that remains macro- and sentiment-sensitive. Two events last week point to a structural shift in that base: a reserve layer that takes supply off the float, and a credit market mature enough that long-duration holders don't have to sell into stress.

- Market context. BTC is up 0.5% month-to-date through May 23, with realized volatility at 28% annualized, the third-lowest May reading since 2011. The range held through the worst weekly ETF outflow since January, a hot April CPI print on May 12, and Mark Cuban's public exit. Strategy's $2.01 billion purchase last week largely offset a simultaneous $1 + billion ETF outflow. But on May 5, Saylor signaled Strategy may sell Bitcoin to fund STRC dividend obligations — the first such signal since 2020, and a reminder that even the closest thing to an unconditional buyer is conditional.

- The reserve layer (ARMA). Underneath, however, the structural layer is being built. On May 21, Representatives Begich and Golden introduced the American Reserve Modernization Act (ARMA) with 17 co-sponsors. If passed, it would consolidate existing federal Bitcoin holdings (1.0% to 1.6% of total supply) under Treasury custody, mandate a 20-year hold, and direct a study on budget-neutral acquisition strategies. Notably, by codifying reserve status in law rather than executive order, ARMA lowers the political risk of reversal and raises Bitcoin's credibility as a reserve asset for other sovereigns weighing their own exposure. The marginal sovereign bid that follows would build slowly, on a horizon longer than any allocator cycle.

- The credit layer. The crypto credit market has matured, consolidating around quality operators after October's liquidation event. Nexo cements its place at the center of that consolidation. Per Galaxy Research's Q1 2026 leverage report, Nexo was one of only four CeFi lenders to grow its loanbook, while the broader CeFi market contracted. Nexo is among the three largest lenders globally with a 7.02% market share across tracked CeFi lending. The maturing credit layer means long-duration holders can actively manage exposure through weakness without being forced to sell.

The gold parallel. Central banks hold around 38,666 tonnes of gold — about 18% of all above-ground supply (World Gold Council). Those reserves turn over slowly. ARMA is the first credible legislative path to an equivalent structure for Bitcoin. A mature lending market against those reserves is the second piece of the same architecture. The throughline: Bitcoin's bid is shifting from buyers who can change their minds to holders who won't sell, and a mature credit market that means they don't need to.

TradFi trends

One hedge for all Bitcoin ETFs

The SEC approved a new Bitcoin options product on May 22, listed on Nasdaq under the ticker QBTC — the first U.S. securities-exchange options contract that references the Bitcoin spot price directly. Existing IBIT and FBTC options track a single fund. Cboe's CBTX, listed since December 2024, broadens that to an index of spot Bitcoin ETFs. QBTC goes a step further, referencing an index built from order-book data at eight crypto exchanges — no fund layer in between. It clears in the same brokerage account and uses the same margin rules as S&P 500 index options, so TradFi institutions can hedge Bitcoin the way they already hedge equities. Trading begins once the CFTC signs off and the OCC updates its disclosure document, expected in the second half of 2026.

Macroeconomic roundup

De-escalation meets rates reality

The de-escalation trade returned last week but was capped by hawkish central banks. Brent fell from above $110 to $105.5 on Iran negotiation headlines, and U.S. equities recovered most of the geopolitical risk premium. Bond yields moved the other way. The U.S. 10-year closed near 4.6%, with the 30-year touching its highest level since July 2007. The April 28–29 FOMC minutes ran more hawkish than the statement implied. Many participants would have preferred to drop the bias language outright, citing upside inflation risks from oil, tariffs and Middle East tensions. The majority signaled that further firming would likely become appropriate if inflation persists above 2%, with some discussion that the next move could be a hike rather than a cut.

The yield move was not uniform across regions:

- The 10-year U.S.-Bund spread reached 150 basis points, its widest since August 2025.

- Both the ECB and the U.S. Fed are hawkish but the macro backdrop is diverging. The U.S. is dealing with sticky inflation against resilient growth, Europe with sticky inflation against cracking growth.

- The flash eurozone composite PMI fell to 47.5 in May, a 31-month low, leaving the ECB hiking into a slowdown.

The week's most interesting data story

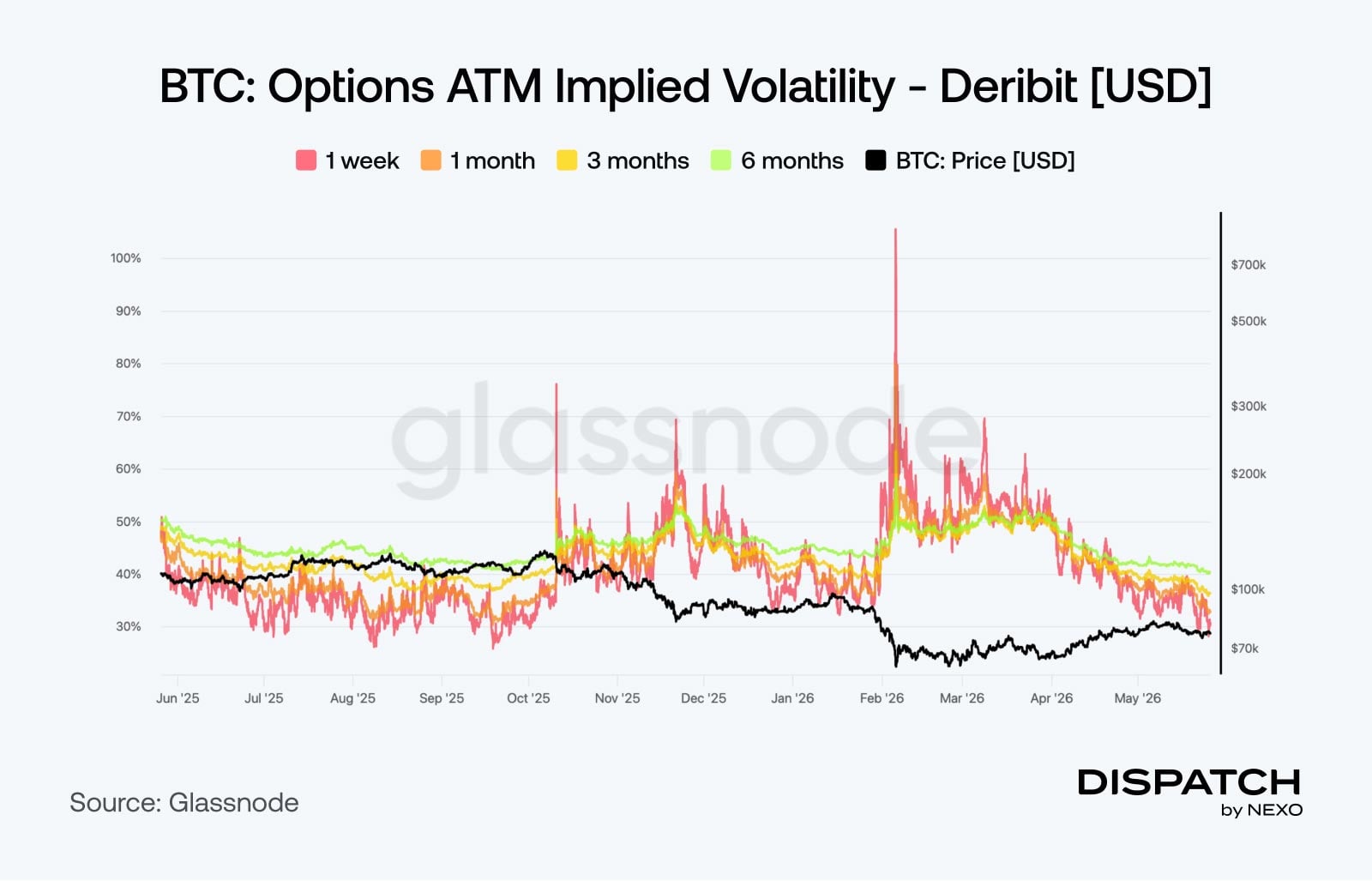

BTC implied volatility remains at historically low levels

Bitcoin implied volatility continues to compress as BTC stabilizes in the upper $70,000s after recovering from its early-February low near $63,000. The term structure, inverted through February and March, has normalized. As of May 21, 1-week ATM IV sits at 29.3%, 1-month at 34.4%, 3-month at 37.3%, and 6-month at 40.7% — all within a few points of their respective 15-month lows. Traders are pricing in relative calm despite persistent macro uncertainty and a still-fragile market structure. Historically, prolonged periods of suppressed Bitcoin volatility rarely last; compression regimes tend to precede significant directional moves, particularly when spot stabilizes after large drawdowns.

The numbers

The week’s most interesting numbers

5.2% — U.S. 30-year treasury yields hit a 19-year peak last week, marking a major bond market selloff, driven by escalating inflation fears.

32.7% — Bitcoin's 1-month implied volatility compressed in May, hitting its lowest level since September 2025.

$230 million — combined net inflows into spot SOL and XRP ETFs over the first 16 trading days of May 2026, with neither product registering a single outflow day.

65.2%— the share of all EUR stablecoins hosted on Ethereum.

Hot topic

What the community is discussing

https://x.com/_10delta_/status/2058551705051058277

AI and utility driven infra will lead the next leg higher, they say.

https://x.com/eliant_capital/status/2058546044334432607

Goldman's sentiment gauge suggests positioning is not yet stretched or euphoric.

https://x.com/MarylandHODL21/status/2058981918108991893

Yield curve control plus money printing will drive capital out of dollars into alternative stores of value.

Dispatch is a weekly publication by Nexo, designed to help you navigate and take action in the evolving world of digital assets. To share your Dispatch suggestions and comments, email us at [email protected].