Кредиты, обеспеченные криптовалютой: сравнение Nexo и Ledn

May 03•10 min read

Взять кредит под залог криптовалюты вместо её продажи — ключевая стратегия для тех, кто хочет получить ликвидность, не теряя долгосрочной позиции в цифровых активах. Вместо того чтобы создавать налогооблагаемое событие или закрывать позицию, вы закладываете свои активы в качестве обеспечения и получаете средства в обмен — сохраняя потенциал роста.

Оба сервиса — Nexo и Ledn — предлагают этот тип кредитования под обеспечение криптовалютой. Но несмотря на схожую концепцию, их продукты работают по-разному. Один предлагает возобновляемую кредитную линию с широкой поддержкой обеспечения, другой — срочные кредиты в Bitcoin с ограниченным набором функций.

Это сравнение разбирает ключевые различия, чтобы вы могли выбрать продукт, который подходит именно вам.

Для быстрого обзора функций и актуальных ставок посетите нашу страницу сравнения Nexo и Ledn

Обзор Nexo и Ledn

Ставки и условия могут меняться. Актуальные сведения уточняйте на соответствующих платформах.

Обзор Nexo

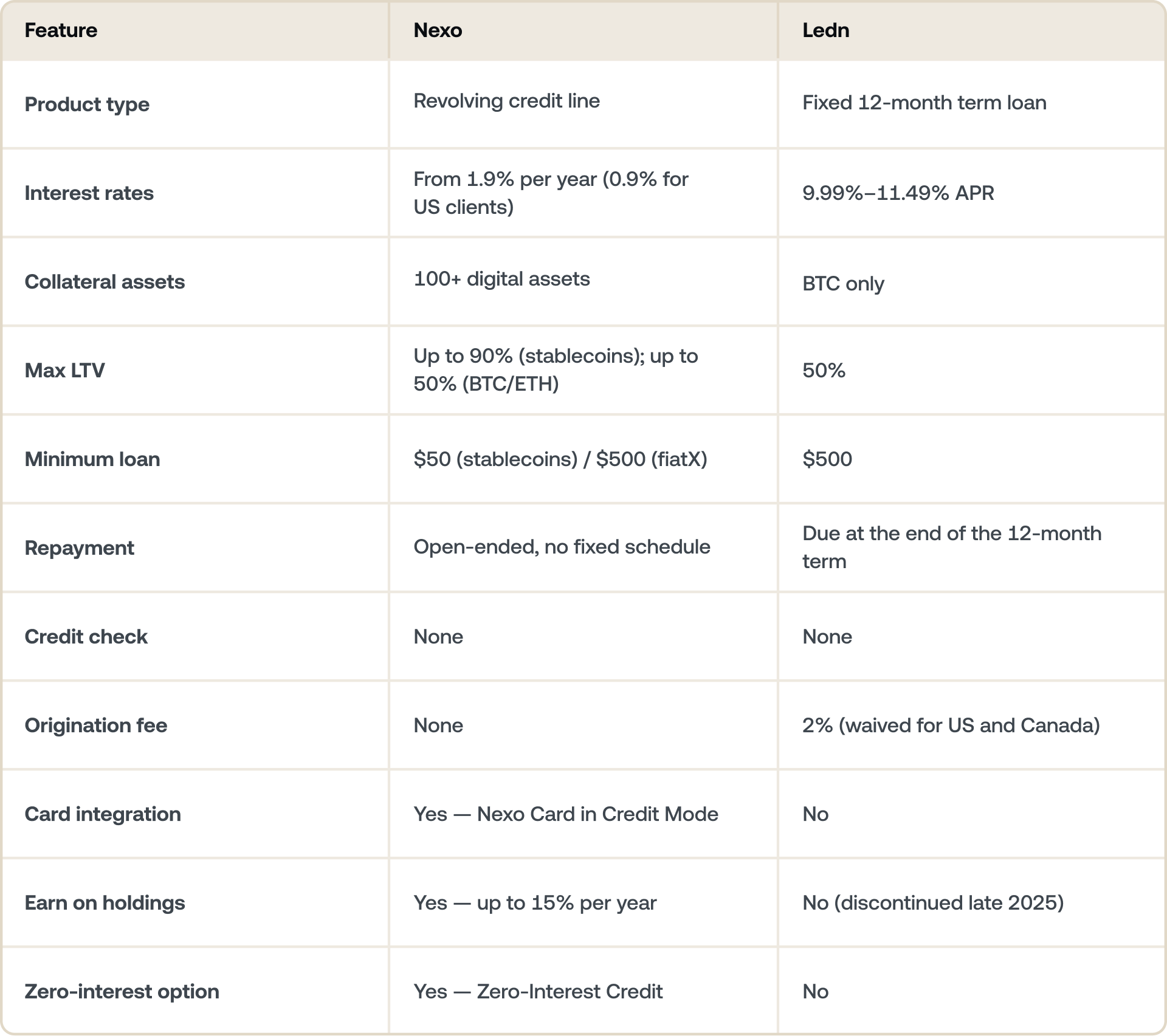

Nexo предлагает возобновляемую криптовалютную кредитную линию. Вы добавляете обеспечение, лимит кредитования устанавливается автоматически, и вы можете снимать средства, погашать долг и брать кредит снова — без повторной подачи заявки. Нет фиксированной даты окончания и обязательного ежемесячного погашения. Проценты начисляются ежедневно только на фактически снятую сумму.

Ставки начинаются от годовых для клиентов уровня Platinum, поддерживающих показатель LTV на уровне 20% или ниже. Ваша ставка определяется вашим Loyalty Tier, который зависит от доли NEXO Tokens в вашем общем портфеле.

Nexo также предлагает Zero-Interest Credit — отдельный продукт, позволяющий взять кредит под залог BTC или ETH под 0% без комиссий, с фиксированным сроком и без риска ликвидации на протяжении этого срока. Каждая позиция включает заранее заданные параметры защиты цены, поэтому потенциальные результаты прозрачны с самого начала.

Помимо кредитования, Nexo работает как универсальная платформа: вы можете зарабатывать проценты на активы через Flexible Savings или Fixed-term Savings, совершать покупки с помощью Nexo Card и управлять всем из единого аккаунта.

Обзор Ledn

Ledn предлагает срочные 12-месячные криптовалютные кредиты. Вы подаёте заявку на конкретную сумму, получаете средства (как правило, в тот же день) и имеете 12 месяцев на погашение основного долга и накопленных процентов по истечении срока. Ledn позволяет клиентам пролонгировать или обновить кредиты по истечении срока, однако заёмщики обязаны погасить или реструктурировать баланс в зависимости от рыночных ограничений по LTV и актуальных обновлений продуктов.

Ledn принимает в качестве обеспечения только Bitcoin. Платформа прекратила поддержку Ethereum в конце 2025 года и одновременно свернула продукты с начислением процентов, сосредоточившись на кредитовании под залог BTC.

Ставки зависят от размера кредита: 11,49% годовых для кредитов до $250 000, снижаясь до 9,99% для кредитов свыше 1 миллиона долларов. Комиссия за выдачу кредита в размере 2% применяется для заёмщиков за пределами США и Канады в момент выдачи средств.

Почему заемщики выбирают Nexo

Клиенты Nexo ценят кредитную линию, которая остаётся открытой и адаптируется к их потребностям со временем. Вместо разовой заявки с обратным отсчётом до погашения возобновляемая структура Nexo позволяет снимать средства, когда нужна ликвидность, погашать удобным образом и повторно использовать линию без лишних формальностей. Для заёмщиков, управляющих постоянными потребностями в денежном потоке или желающих брать кредиты ситуативно, такая гибкость имеет реальную ценность.

Ставки и комиссии

Ставки и комиссии Nexo

Ставки займа Nexo начинаются от годовых для клиентов уровня Platinum, которые держат не менее 10% стоимости своего портфеля в NEXO Tokens и поддерживают показатель LTV на уровне 20% или ниже. Ставки корректируются в зависимости от вашего Loyalty Tier — Base, Silver, Gold или Platinum — который рассчитывается ежедневно на основе ваших активов в NEXO Token.

Нет ни комиссии за выдачу кредита, ни комиссии за оформление заявки, ни минимального требования к погашению. Вы можете погасить часть или весь баланс в любое время с помощью криптовалюты, FiatX или стейблкойнов.

Для заёмщиков, которым важна определённость ставки и отсутствие риска ликвидации, Zero-Interest Credit — это отдельный продукт: 0% годовых, нулевые комиссии, фиксированный срок и встроенные параметры защиты цены, чтобы вы знали результат ещё до получения кредита. Он получил награду Consumer Lending Product of the Year на FinTech Breakthrough Awards 2026.

Ставки и комиссии Ledn

Ledn использует многоуровневую структуру ставок в зависимости от размера кредита:

- Standard (до $250 000): 11,49% APR

- Tier 1 ($250 000–$500 000): 10,99% APR

- Tier 2 ($500 000–$1 000 000): 10,49% APR

- Tier 3 ($1 000 000+): 9,99% APR

Комиссия за выдачу кредита в размере 2% взимается при получении средств для заёмщиков за пределами США и Канады. Проценты начисляются ежедневно и погашаются при закрытии кредита — либо по истечении срока, либо при досрочном погашении.

Почему заемщики выбирают Nexo

Структура ставок Nexo выгодна для заемщиков, готовых оптимизировать свой портфель — в частности, держа часть средств в NEXO Tokens. Для заёмщиков, которые это делают, потенциальная экономия по сравнению с платформами с фиксированными ставками существенна, особенно при длительных периодах кредитования.

Zero-Interest Credit от Nexo также открывает заёмщикам путь к финансированию под 0%, недоступному в Ledn. А поскольку на любой продукт Nexo не взимается комиссия за выдачу, стоимость доступа к кредитной линии ниже с первого дня.

Поддерживаемые виды обеспечения

Обеспечение Nexo

Nexo принимает более 100 цифровых активов в качестве обеспечения, включая Bitcoin, Ethereum, XRP, Solana, Polkadot и широкий спектр стейблкойнов. Вы можете объединять несколько активов для обеспечения одной кредитной линии, менять их по мере изменения рыночных условий и корректировать свою позицию без закрытия аккаунта.

Стейблкойны на Nexo имеют более высокий максимальный показатель LTV — до 90% — поскольку их ценовая стабильность снижает риск ликвидации. Для BTC и ETH максимальный LTV составляет 50%.

Обеспечение Ledn

Ledn принимает только Bitcoin. Платформа прекратила поддержку Ethereum в конце 2025 года в рамках решения сосредоточиться исключительно на кредитовании под залог BTC. Максимальный LTV для всех кредитов Ledn составляет 50%.

Для заёмщиков, которые держат только Bitcoin, ограниченный подход Ledn не является недостатком. Однако для тех, кто держит Ethereum, альткойны или стейблкойны, эти активы не могут использоваться в качестве обеспечения в Ledn.

Почему заемщики выбирают Nexo

Гибкость обеспечения Nexo означает, что весь ваш портфель может работать на вас — не только Bitcoin. Если вы держите диверсифицированный набор активов в BTC, ETH и стейблкойнах, Nexo позволяет закладывать их совместно, оптимизировать LTV по типам активов и корректировать состав по мере движения рынка. Это особенно полезно на волатильных рынках, когда вы можете захотеть изменить состав обеспечения, не закрывая кредит.

Погашение и гибкость

Погашение Nexo

Кредитная линия Nexo является бессрочной. Нет ни срока закрытия, ни фиксированного графика, ни минимального взноса. Вы сами решаете, когда и сколько погашать. Проценты начисляются ежедневно только на непогашенный баланс — поэтому если вы погасите часть баланса, ваши ежедневные процентные расходы сразу же снизятся.

Вы можете погашать долг с помощью криптовалюты, FiatX или стейблкойнов прямо с учетной записи Nexo. Кредитная линия остаётся открытой после погашения, поэтому вы можете снова снять средства без новой заявки.

Погашение Ledn

Кредиты Ledn имеют фиксированный срок 12 месяцев. Проценты начисляются ежедневно на протяжении всего срока, ежемесячные платежи не требуются, а полный баланс подлежит оплате по истечении срока.

Кредиты номинированы в USD и могут быть погашены через USDC, банковский перевод в USD или через эквивалентный обмен BTC на USD. Заёмщики также могут подать заявку на рефинансирование кредита на новый срок при соответствии требованиям по LTV или выбрать досрочное погашение без штрафа за предоплату.

Если кредит не погашен или не рефинансирован к сроку закрытия, автоматизированная система Ledn ликвидирует необходимое количество обеспечения для покрытия баланса. Льготного периода в этот момент нет.

Почему заемщики выбирают Nexo

Отсутствие крайнего срока погашения устраняет значительный источник давления, характерного для срочных кредитов. С Nexo нет нависающего срока закрытия, который мог бы совпасть с падением рынка, ограничением личного денежного потока или периодом, когда продажа обеспечения была бы невыгодной. Заёмщики, которые хотят сохранять гибкость — снимая и погашая средства на своих условиях — находят возобновляемую структуру Nexo более удобной для управления своими финансами.

Расходы по кредитной линии

Интеграция с картой Nexo

Nexo Card напрямую интегрирована с кредитной линией Nexo через Credit Mode. Каждая покупка по карте автоматически списывается с кредитной линии — это значит, что вы можете занимать под криптовалюту прямо в момент покупки, везде, где принимается Mastercard. Покупки в Credit Mode также приносят до 2% кэшбека в криптовалюте.

Это делает кредитную линию Nexo полноценным инструментом для повседневных трат, а не только механизмом для крупных разовых выводов средств.

Расходы через Ledn

Ledn не предлагает карту и не имеет интеграции с торговыми точками. Заёмные средства выплачиваются в USD, USDC или местной фиатной валюте, которые затем нужно перевести на банковский счёт или внешнюю платформу для использования. Платформа сосредоточена исключительно на выдаче и погашении кредитов без потребительского уровня для расходов.

Почему заемщики выбирают Nexo

Для заёмщиков, которым нужна кредитная линия, выполняющая роль инструмента для покупок, Nexo — единственный вариант из двух. Возможность занимать в момент покупки — зарабатывая кешбэк на этих транзакциях — добавляет практическое повседневное измерение, которого продукт Ledn не предлагает.

Начисление процентов на ваши активы

Доходность Nexo

Активы, хранящиеся на Nexo, могут приносить проценты при условии, что общий баланс портфеля соответствует минимальному порогу в $5 000. Flexible Savings предлагает ежедневное начисление с капитализацией без периода блокировки. Fixed-term Savings предлагает более высокие ставки на сроки до 12 месяцев.

Ставки достигают до 15% годовых в зависимости от актива, вашего Loyalty Tier и того, хотите ли вы получать выплаты в NEXO Tokens. Nexo поддерживает начисление дохода на Bitcoin, Ethereum, стейблкойны и десятки других активов.

Доходность Ledn

Ledn прекратила действие продуктов с начислением процентов в конце 2025 года. Активы, хранящиеся на Ledn, больше не генерируют никакой доходности. Если ваше обеспечение активно не обеспечивает кредит, оно просто лежит без дела.

Почему заемщики выбирают Nexo

На Nexo кредитование и получение дохода могут работать параллельно. Активы, которые вы держите на платформе и которые не заложены в качестве обеспечения, могут приносить до 15% годовых через Flexible или Fixed-term Savings. Это означает, что часть вашего портфеля может продолжать генерировать доходность, пока другая часть обеспечивает вашу кредитную линию.

Для кого лучше подходит каждая платформа

Nexo подходит заёмщикам, которые:

- Хотят возобновляемую кредитную линию, из которой можно снимать, погашать и повторно использовать без новой заявки

- Держат диверсифицированный портфель и хотят использовать несколько активов в качестве обеспечения

- Хотят зарабатывать проценты на активы во время кредитования

- Хотят интегрированных расходов через Nexo Card в Credit Mode

- Нуждаются в быстром и гибком доступе к средствам без фиксированного срока погашения

Ledn подходит заёмщикам, которые:

- Держат исключительно Bitcoin и предпочитают платформу, созданную вокруг BTC

- Хотят простую структуру с фиксированной ставкой

- Предпочитают чётко определённый 12-месячный срок и понятный график погашения

Сравните Nexo и Ledn — актуальные ставки и подробности о продуктах.

Часто задаваемые вопросы

1. В чём разница между Nexo и Ledn для криптовалютного кредитования?

Nexo предлагает возобновляемую кредитную линию со ставками от годовых, поддержкой более 100 активов в качестве обеспечения, интегрированными расходами через карту и без фиксированного графика погашения. Ledn предлагает фиксированные 12-месячные кредиты под залог Bitcoin по ставке 9,99%–11,49% APR без интеграции с картой и с обеспечением только в BTC.

2. У какой платформы ниже ставки займа?

Ставки Nexo начинаются ниже — от годовых для клиентов уровня Platinum — по сравнению с диапазоном Ledn 9,99%–11,49% APR. Минимальные ставки Nexo требуют хранения NEXO Tokens для получения уровня Platinum; ставки Ledn дифференцированы только по размеру кредита.

3. Могу ли я взять кредит под Ethereum в Ledn?

Нет. Ledn прекратила поддержку ETH в конце 2025 года и теперь принимает в качестве обеспечения только Bitcoin. Nexo поддерживает Ethereum, Bitcoin и более 100 других цифровых активов.

4. Нужно ли мне держать NEXO Tokens, чтобы брать кредиты на Nexo?

Нет. Любой может брать кредиты на Nexo без NEXO Tokens. Их хранение улучшает ваш Loyalty Tier, что снижает ставку займа и открывает дополнительные преимущества — но это не является обязательным условием для доступа к кредитной линии.

5. Проводится ли проверка кредитной истории на какой-либо из платформ?

Ни Nexo, ни Ledn не требуют проверки кредитной истории. Обе платформы используют ваши цифровые активы в качестве обеспечения для одобрения и обеспечения кредитования.

6. Что происходит, если стоимость моего обеспечения падает?

На обеих платформах падение стоимости обеспечения повышает ваш показатель LTV. Nexo обеспечивает мониторинг LTV в реальном времени и уведомления, а также автоматически использует обеспечение для погашения части баланса, если ваш LTV приближается к порогу ликвидации в 83,33%. Обратите внимание: если ваше обеспечение включает стейблкойны, порог ликвидации может изменяться. Ledn отправляет уведомления по эл. почте при LTV 70% и 75% и запускает автоматическую ликвидацию при превышении LTV уровня 80%.

7. Могу ли я тратить средства напрямую с кредитной линии Nexo?

Да. Nexo Card в Credit Mode позволяет занимать под вашу криптовалюту прямо в момент покупки — везде, где принимается Mastercard. Ledn не предлагает карту и не имеет прямой интеграции для расходов.

8. Могу ли я зарабатывать проценты на свою криптовалюту во время кредитования на Nexo?

Да. Активы, хранящиеся в учетной записи Nexo и не заложенные в качестве обеспечения, могут приносить проценты через Flexible или Fixed-term Savings. Ledn прекратила действие продуктов с начислением процентов в конце 2025 года.

9. Что такое Zero-Interest Credit от Nexo?

Zero-Interest Credit — это отдельный продукт Nexo, позволяющий брать кредит под BTC или ETH под 0% годовых и без комиссий, без риска ликвидации в течение фиксированного срока. Каждая позиция включает заранее определенные параметры защиты цены, поэтому результаты видны с самого начала. Это отдельный продукт от стандартной кредитной линии Nexo's.

Данные материалы доступны по всему миру. Наличие этой информации не означает доступ к описанным услугам, которые могут быть недоступны в отдельных юрисдикциях. Эти материалы носят исключительно общий информационный характер и не являются финансовой, юридической, налоговой или инвестиционной консультацией, предложением, призывом, рекомендацией или одобрением использовать какие‑либо услуги Nexo, не являются персональными и никоим образом не учитывают конкретные инвестиционные цели, финансовое положение или потребности. Цифровые активы сопряжены с высоким уровнем риска, в том числе связанным с волатильностью рыночных цен, изменениями в регулировании и техническим прогрессом. Прошлые результаты цифровых активов не являются надежным индикатором будущих результатов. Цифровые активы не являются деньгами или законным платежным средством, не обеспечены государством или центральным банком, и у большинства из них нет базовых активов, источника дохода или иных источников стоимости. Следует руководствоваться собственным суждением с учетом личных обстоятельств. Перед принятием любых решений рекомендуется проконсультироваться с квалифицированным специалистом.