Markets Today - July 13, 2026

Jul 13•4 min read

-1.png)

Daily analysis of crypto markets and the forces shaping them, from the Nexo research desk.

Bitcoin holds ground as geopolitical tensions resurface

Bitcoin holds above $62,000 despite renewed U.S.-Iran tensions that unwound last week's fragile de-escalation trade. Following developments in the Strait of Hormuz, President Trump signaled that the June ceasefire was over. Oil briefly lifted before markets steadied. U.S. futures pointed lower Monday. Asian markets split: Tokyo and Seoul sold off sharply, Hong Kong held steady. This is the first week of Q2 earnings season, and the macro calendar is unusually dense. U.S. inflation data, Q2 bank earnings, and Kevin Warsh's first semi-annual monetary policy testimony to Congress all fall within the same trading week.

Bitcoin

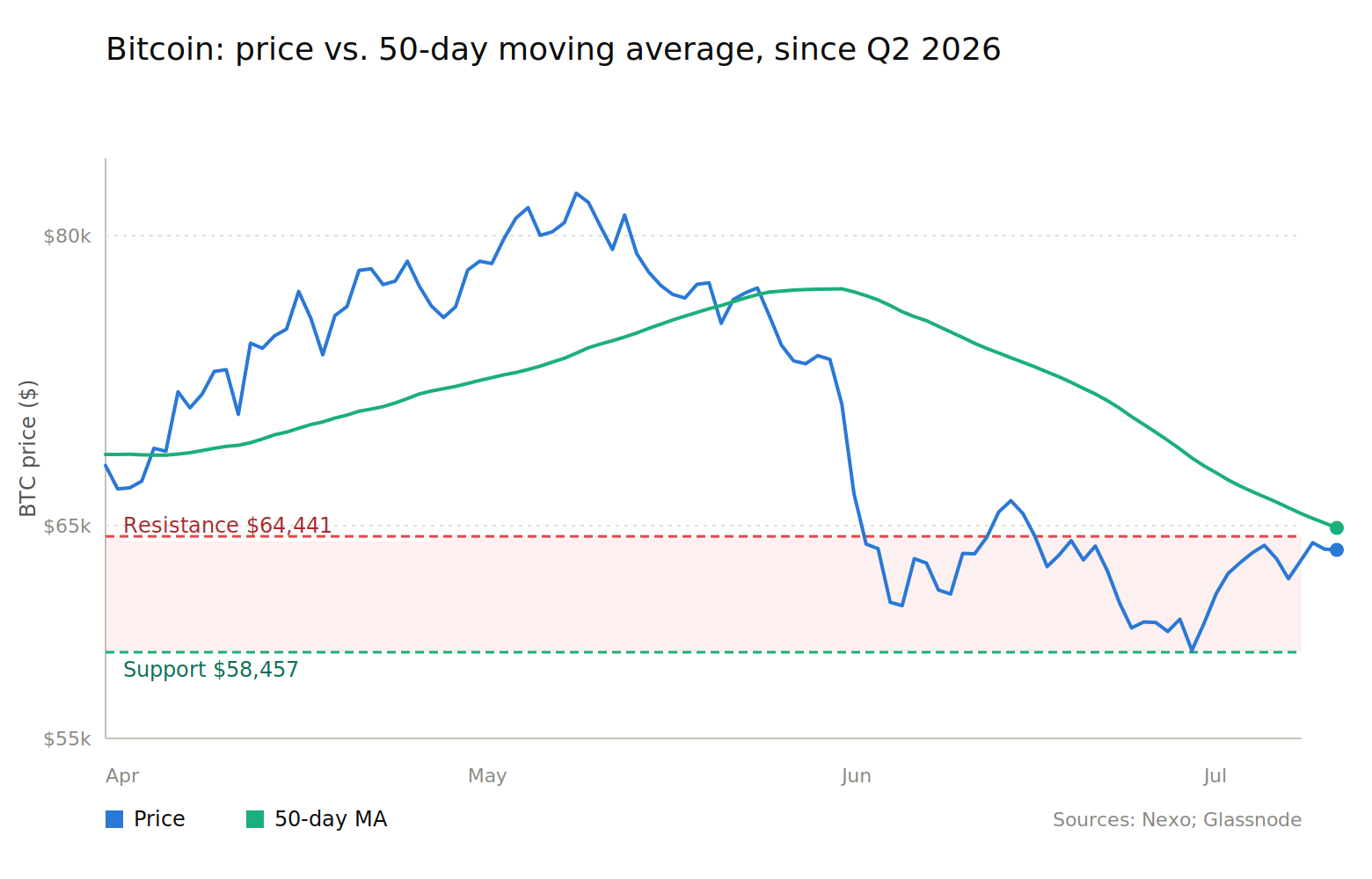

Bitcoin has been boxed in the same range since mid-June, resistance at $64,441 capping every rally, support at $58,457 absorbing the selling, and the renewed Iran tensions haven't broken it either way. It sits just 3.0% below the 50-day moving average but is still 14.8% below the 200-day. Glassnode data shows spot selling pressure has faded. June's net selling averaged nearly 2,000 BTC a day; July's has slowed to just 53 BTC a day, the calmest month of 2026 outside April.

ETF flows confirm it from another angle. The past ten days split between inflow and outflow, netting slightly positive. Spot volume is down by half since the early-July spike, suggesting the decline in ETF net assets tracks price, not redemptions. This stability meets a week that can break it either way. June U.S. CPI lands hours before Fed Chair Warsh's first congressional testimony on July 14. Rates are the early signal to watch, and it'll move through a thin market.

Ethereum & Altcoins

Ethereum's spot ETFs snapped an eight-week outflow streak. They added $84.42 million net for the week of July 6–10, about 0.04% of ETH's market cap. Price decoupled from the broader alt complex starting around July 8. ETH hit a 30-day high on July 12, up 15% over two weeks. Volume stayed thin, though, last week's daily average ran at roughly a third of the past year's typical level.

SOL and XRP rolled over the same week ETH pulled ahead. Their ETF flows were even smaller relative to market cap: SOL added just $930,400, XRP shed $7.18 million. Price followed. Both fell over the week, pulling back from recent highs. Volume told the same story across all three. SOL traded at about 40% of its yearly daily average last week, XRP at under 30%, the thinnest of the group. That leaves the alt complex short on conviction heading into this week's Fed testimony and inflation data.

Macro & Institutional

July is historically strong for markets, and Q2 earnings support that seasonality on the surface.FactSet expects 23.6% y/y S&P 500 earnings growth. But that strength is concentrated in Energy and Tech estimate revisions, not broad-based, which is why bank earnings this week carry more weight than usual. They're the cleanest read on credit quality and consumer resilience beneath a tech-driven index. The bigger swing factor for risk assets, though, is interest rates. Markets now price a 52% chance of a September Fed hike, double last month's odds, and that repricing needs data to hold up. AI capex is the other pressure point on the equity side. Spending estimates have trended higher for quarters, but with some AI-spender shares already under pressure, any sign of hesitation this earnings season would challenge the narrative. Layered on top, the Iran-U.S. escalation pushed Brent up nearly 5% intraday Monday, from $76 to a $79.8 high. If this hardens into a sustained supply shock rather than settling down, it feeds straight back into the rate story.

Looking Ahead

June CPI and PPI (Tuesday, Wednesday) will test whether the Fed's newly hawkish tilt has data to justify it, coming right after minutes showed half the FOMC now penciling in a hike this year. Bank earnings from JPMorgan, Citigroup, BlackRock, and Morgan Stanley matter less for the headline growth numbers than for what they reveal underneath: credit quality, loan demand, and consumer resilience, a read on the real economy that tech-driven index gains have been masking. China's GDP print and a likely Bank of Canada hold round out a week where growth and inflation signals arrive almost simultaneously, while the reignited U.S.-Iran conflict keeps oil, and by extension inflation expectations, as the wildcard that could reshape how markets read everything else.

Author: Dessislava Ianeva, Analyst at Nexo’s Dispatch

This material is produced by Nexo for informational purposes only and does not constitute financial, investment, legal, or tax advice, or a recommendation to transact in any digital asset. Views are the author's as of the date of publication and may change without notice. Information is from sources believed reliable, but Nexo makes no warranty as to its accuracy and accepts no liability for any loss arising from reliance on this material.