Markets Today - June 29, 2026

Jun 29•4 min read

-1.png)

Daily analysis of crypto markets and the forces shaping them, from the Nexo research desk.

Crypto markets stabilize as investors await key U.S. jobs data

The total crypto market cap sits near $2.07 trillion, flat over 24 hours, as the market steadies after last week's macro-driven selloff. Bitcoin trades near $60,000 and Ethereum near $1,580, both consolidating rather than distributing. Traditional markets are steady too. U.S. equity futures point higher after a soft week driven by AI skepticism, oil holds near $72 on Iran de-escalation, and positioning stays cautious into a holiday-shortened week. The main event is Thursday's June payrolls, which sets the rate path after last week's hot PCE. Until it lands, crypto trades the macro tape, not its own flows.

Bitcoin

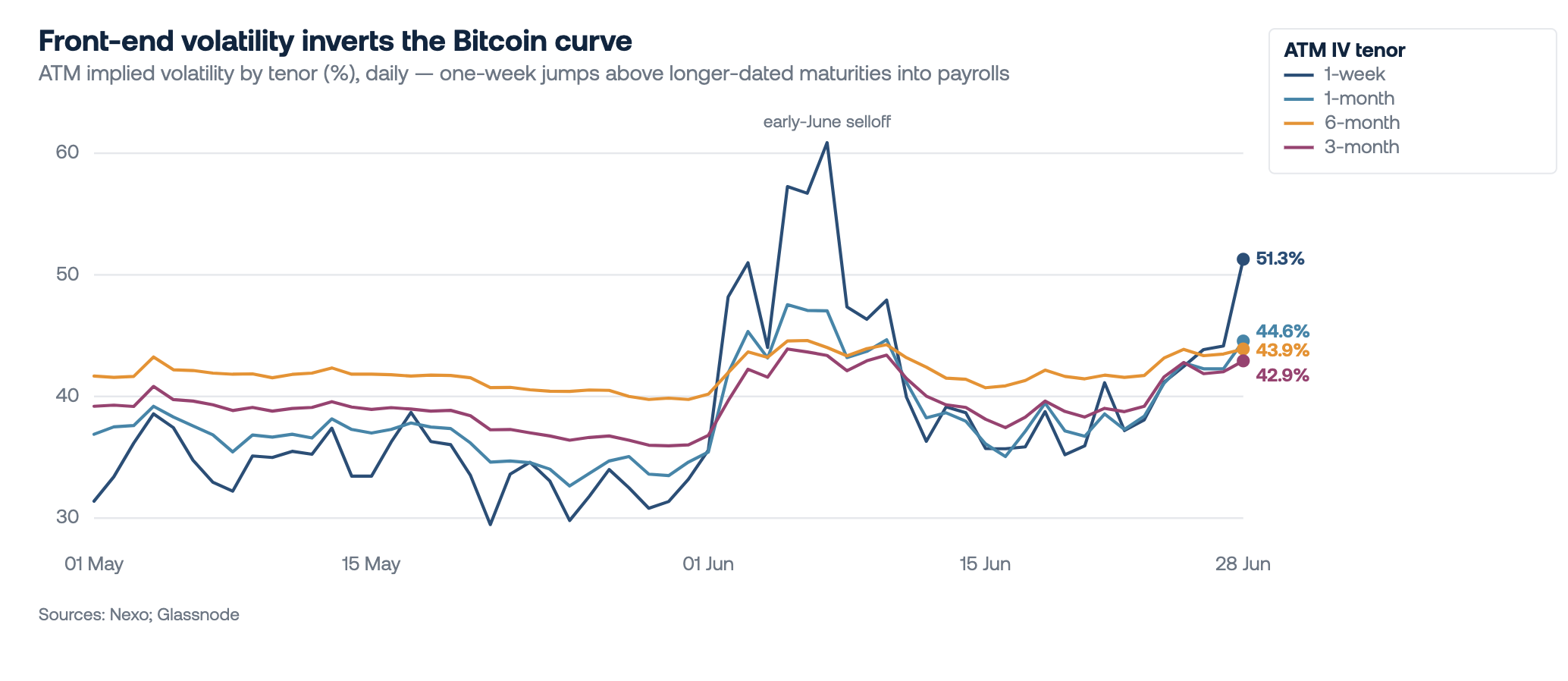

Bitcoin is little changed over 24 hours near $60,000, holding the floor that contained last week's selloff but capped below the mid-June high near $66,300. The breakdown from the $64,000 area leaves $62,000 as first resistance and $59,500, the level that held on June 28, as the line defining the range. The stabilization is real but shallow. Spot volume that spiked above 130,000 BTC through the June 24–26 flush has since fallen to roughly half its 30-day average, so price is steadying on absent participation rather than returning demand.

Derivatives also point to muted risk appetite. Perpetual funding holds only mildly positive near 2.5% annualized, and the three-month basis has compressed to roughly 2.3%, leaving little premium to carry leveraged longs. Options show traders buying protection ahead of Thursday's U.S. payrolls. The implied volatility term structure has inverted for the first sustained stretch since early June's selloff, with one-week IV spiking to 51% against the low 40s further out.

This pattern typically emerges ahead of anticipated market-moving events and signals near-term uncertainty. Hedging demand has tilted toward the downside, with puts trading at a slight premium to calls across tenors and the put-call ratio above one.

Ethereum & Altcoins

Ethereum has lagged the majors, trading near $1,580, up less than 1% on the day but down more than 8% on the week after sliding to $1,565 on June 25, with spot ETFs shedding about $471 million in June and $273 million last week alone. The altcoin funds diverged sharply: Solana held roughly flat on price and flows, XRP drew about $47 million even as the token fell some 7%, and the newly listed HYPE product took in roughly $162 million, almost all from a single $108 million creation on June 25. The split is less a rotation into altcoins on conviction than a function of what institutions sell when they de-risk. Bitcoin and Ethereum are the most liquid instruments and the first sold, while the newer, smaller funds remain in an accumulation phase where creations continue regardless of price.

Macro & Institutional

Markets are priced for falling inflation and a hawkish Fed at once. That rarely holds, and Thursday's U.S. jobs report is what breaks the tie. Core PCE climbed further above its 3% target last week, the sharpest acceleration in two decades outside the post-pandemic surge. At the same time, oil fell about 30% on the month on Iran de-escalation, pulling one-year inflation swaps to post-pandemic lows. With inflation still hot, the Fed needs proof of a cooling labor market before it can cut. A soft payrolls number frees the cut path; a hot one stacks on PCE and keeps policy on hold. That release moves crypto more than anything on-chain right now.

Underneath the price weakness, institutional adoption keeps building. SBI, one of Japan's largest financial groups, launched the country's first trust-backed yen stablecoin, putting a regulated bank behind on-chain settlement. Hong Kong's spot crypto ETFs are up 90% since launch. Toss Bank, a leading South Korean digital bank, signed a Solana remittance pilot, testing blockchain rails for cross-border payments. And the CLARITY Act heads to a July 17 hearing.

Looking Ahead

The week is built around the U.S. labor market and the rate path it dictates. Tuesday's JOLTS openings, forecast to ease to 7.28 million, and Wednesday's ADP and ISM manufacturing prints all speak to the same question of whether hiring is slowing, while eurozone CPI, expected at 3.0% from 3.2%, and a series of central bank speakers fill out the macro backdrop. Thursday is the decisive print. June payrolls are released early ahead of Friday's Independence Day close, with consensus at 114,000 against 172,000 prior, a notable expected deceleration. A soft number would revive the case for cuts and lend support to risk, while an upside surprise would reinforce the PCE read and keep policy on hold. For crypto, the timing compounds the risk. Order book bid depth remains thin, leaving price more sensitive to any deviation from consensus, and the holiday weekend points to lighter liquidity into the close. Through Thursday, Bitcoin continues to trade as a function of the macro tape rather than its own flows.

Author: Dessislava Ianeva, Analyst at Nexo’s Dispatch

This material is produced by Nexo for informational purposes only and does not constitute financial, investment, legal, or tax advice, or a recommendation to transact in any digital asset. Views are the author's as of the date of publication and may change without notice. Information is from sources believed reliable, but Nexo makes no warranty as to its accuracy and accepts no liability for any loss arising from reliance on this material.